Written by Lance Roberts, Clarity Financial

“Exactly one week after last week’s sell off, the market dumped again. This time it was the news of the complete dismemberment of President Trump’s ‘economic council’ of CEO’s along with the rumor that Gary Cohn would be exiting his position at the White House as well. While the latter turned out to be #FakeNews, the damage had already been done as market participants began to question the ability of the Administration to get its promised legislative action advanced.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Given the run up in the markets since the election, which was based on tax cuts/reform, infrastructure spending, repatriation and repeal of the Affordable Care Act, the lack of progress on that agenda has left the markets pushing higher on ‘hope’ and ‘promises.’ The disbanding of the economic council has led to some disruption of that confidence.”

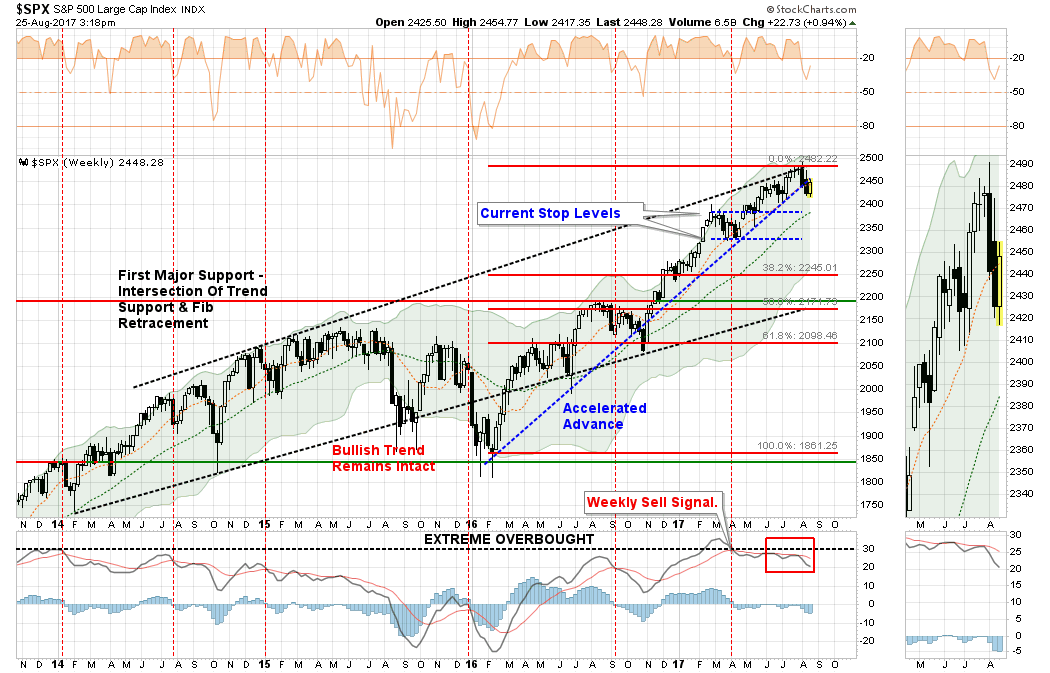

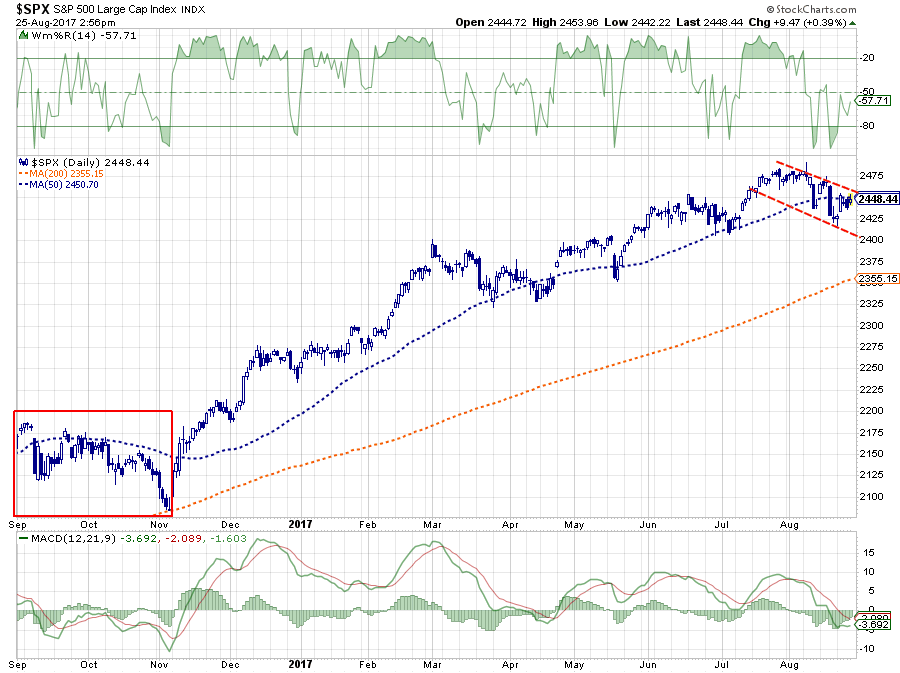

For the second week in a row, the market staged a strong comeback rally which again failed at resistance, keeping further additions to equities on hold once again this week. With the market remaining on a short-term “sell signal,” we will remain patient to allow the market to regain a firmer footing within the confines of the current bullish trend.

On a weekly basis, the “bullish trend” remains at risk as well. With the markets on a weekly “sell signal” at fairly high levels, it does suggest that “stock slop” could be with us for a while particularly as we head into the month of September. This potentially set investors up for a bigger correction in the weeks ahead.

In case you missed last week’s missive, I laid out two scenarios we were watching while we “wait for confirmation the current sell-off has abated before adding additional risk exposure to portfolios.”

Scenario 1:

The market regains its footing next week and rallies strongly enough to break above the downward trending levels of previous rally attempts. Such action would confirm the bullish trend remains intact and would provide the opportunity to rebalance equity exposure to model weights accordingly.

Scenario 2:

The market rallies to the upwardly sloping “bullish trend line” that began with the election of President Trump. The rally fails at resistance and turns lower. Such a failure would confirm the current short-term bullish trend has likely concluded leading to a reduction of equity exposure, increases in cash positions and fixed income, and a reduction in overall portfolio equity risk.

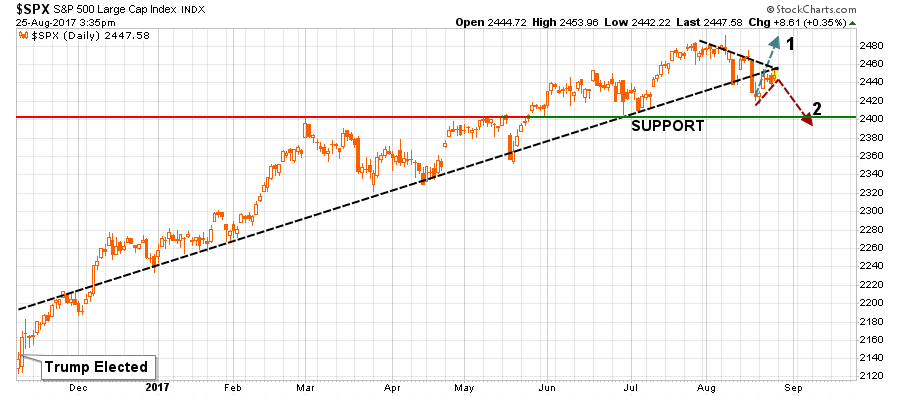

Currently, it is “Scenario 2” which continues to play itself out currently.

The Case For “Scenario 2”

From an analytical viewpoint, there are several factors that continue to support “scenario 2,” as detailed above, playing out.

As noted the internal deterioration of the market has continued unabated over the last several weeks the number of stocks trading above their respective 50- and 200-day moving averages dropping to levels that have more normally equated to a deeper market correction.

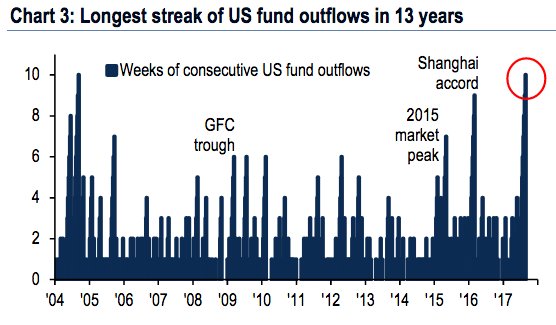

The internal deterioration in the market shouldn’t be surprising given the large outflows from equities over the last few weeks as noted recently by Joe Ciolli:

“Traders are dumping US stocks to a degree not seen in 13 years. They’ve pulled money out of US equity funds for 10 straight weeks, the longest such streak since 2004, according to data compiled by Bank of America Merrill Lynch.”

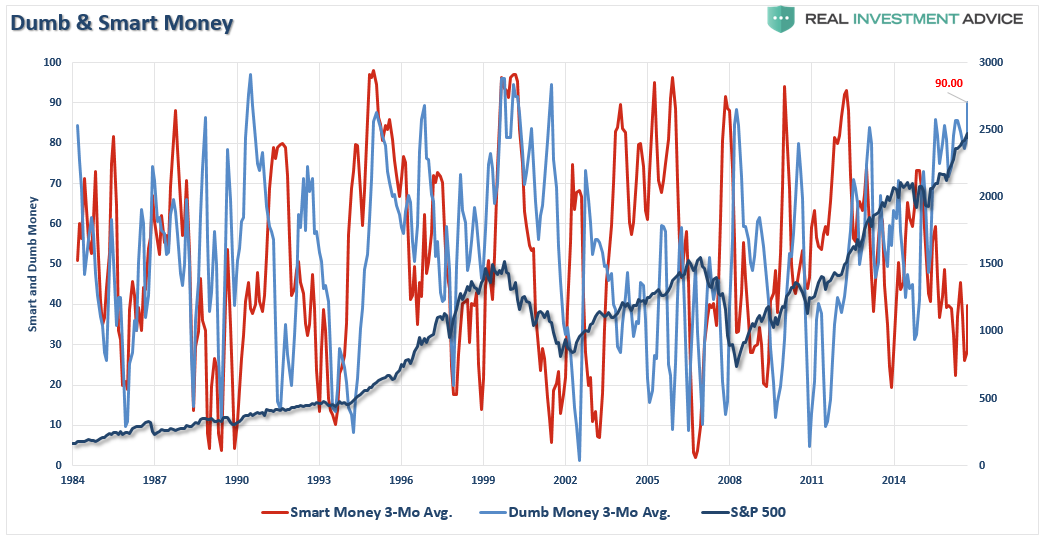

This doesn’t mean that stocks are imminently due for a crash, but the institutional (smart money) outflows from equities certainly put downward pressure on the “bull case” for the time being. However, with investors (dumb money) extremely long equities, as I noted two weeks ago, the case for substantially higher highs is quite limited.

Sentiment Trader also made an important observation in this regard as well with respect to the Dow indices being “out of gear.” To wit:

“When it comes to market clichés, theories, and indicators, people tend to have an almost religious adherence to minutia and forget the underlying principles behind them.

The Hindenburg Omen is a perfect example. The exact thresholds used to trigger the signal are seen as written in stone as if by some oracle, when we should instead be focused on the general conditions that show uptrending markets, losing underlying momentum, that are heavily split between winners and losers. The exact thresholds don’t matter.

Same with Dow Theory. There are strict adherents that require certain specific criteria, which is preposterous. Instead, we should just be concerned whether Industrial and Transportation stocks are in gear…or not. When they are, markets do well; when they aren’t, they don’t.

And right now, they’re not.”

![]()

Here is the important point:

“The Dow indexes are out of gear. The Dow Transportation Average continues to badly lag its brother index, the Dow Industrial Average. The Transports are not only below their 200-day average, they just dropped to a fresh multi-month low. Yet the Industrials are more than 5% above their own 200-day average, a divergence which has tended to resolve to the downside for both indexes, especially in the shorter term.”

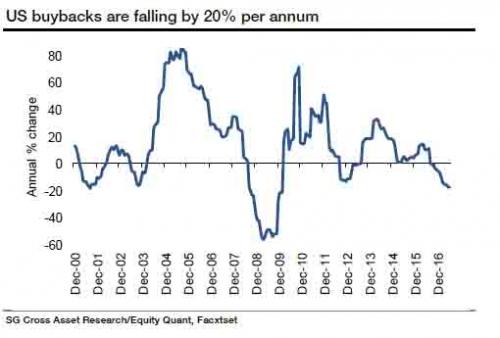

Another major concern is the slide corporate share buybacks. Buybacks have been one of the biggest supports of the bull market which was directly fueled by the Federal Reserve’s ultra-low interest policy and a flood of liquidity. As noted recently by Zerohedge:

“Share buybacks have slumped by over 20% YoY. Ominously, this is the sharpest drop in corporate buybacks since the financial crisis effectively shut down bond markets in 2008, as a result of the market no longer rewarding companies that lever up just to repurchase their own stock.”

“In fact, according to a chart from Credit Suisse, Fink may be more correct than he even knows. As CS’ strategist Andrew Garthwaite writes, ‘one of the major features of the US equity market since the low in 2009 is that the US corporate sector has bought 18% of market cap, while institutions have sold 7% of market cap.’

What this means is that since the financial crisis, there has been only one buyer of stock: the companies themselves, who have engaged in the greatest debt-funded buyback spree in history.”

With the Trump Administration about to have “crash course” in Washington politics when he has to deal with both a budget and a debt ceiling debate in the next couple of weeks, the realities of passing tax legislation to support current earnings and valuation levels are becoming much less likely. Furthermore, as I noted on Friday:

“The REAL problem with a government shutdown is it will serve as another distraction to keep the current Administration off of their primary task of passing their legislative agenda of tax reform, cuts, infrastructure spending and immigration reform. As I have stated many times previously, this is one of the biggest risks to the markets currently.”

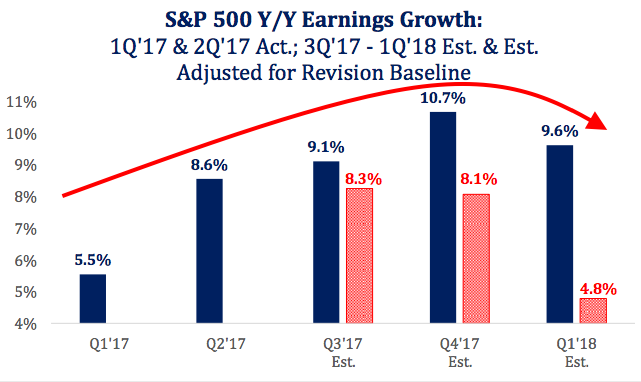

With legislative agenda stalled AND stock buybacks declining, this is going to weigh on the marginal earnings growth that has been inflated through the reduction is shares outstanding. As Strategas points out, Wall Street is not preparing for the decline in EPS that is coming.

“Last year’s easy comps become this year’s tougher comps starting now, so the natural progression is for the growth rate to slow. Adjusting prevailing estimates for the historical revision baseline, which is negative, shows earnings growth falling to mid-single digits rates by next year.

This is not to say earnings will begin to decline straightaway, but they will mathematically increase at a decreasing rate. This progression is typical of a late-cycle profit re-acceleration running out of steam.”

Don’t get all depressed. These are just things you NEED to be paying attention to.

The good news is that on a VERY short-term basis, the markets are oversold enough to garner a bounce next week. Given the points above, that bounce will need to be strong enough to reverse the negative trends currently running through the markets. The last time the market broke the 50-dma, and failed to reclaim it in a very short-period, led to a much deeper correction heading into the Presidential election.

Based on the current backdrop, I continue to recommend, again this week, that investors should take some actions in rebalancing portfolio risks accordingly.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

This doesn’t mean “sell everything” and run into cash. It simply means pay attention to your exposure and have a plan in place in case something goes wrong.