Written by Lance Roberts, Clarity Financial

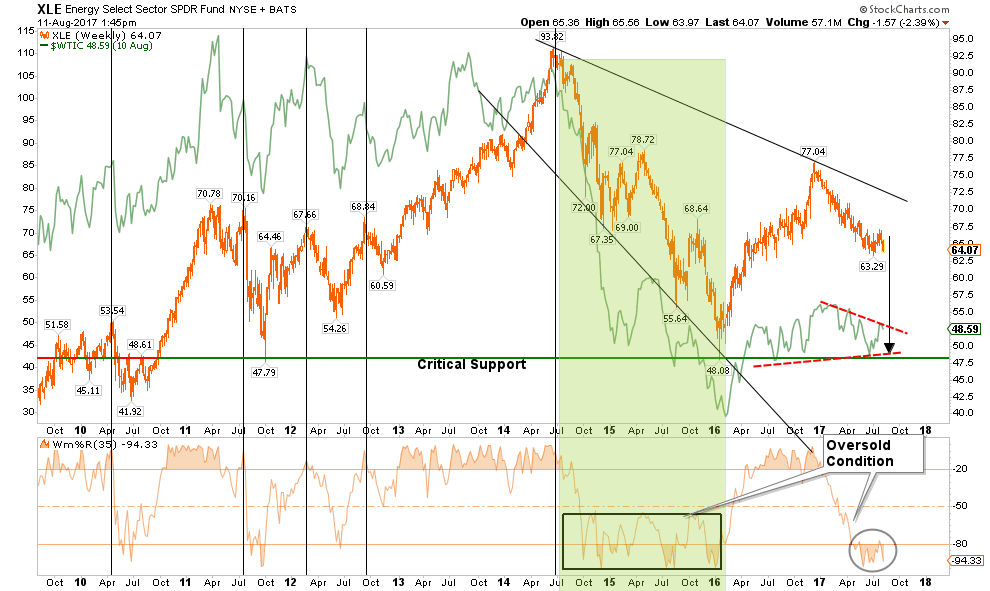

ENERGY

As shown below, there is an unsurprisingly high correlation between oil and energy prices. As such, it is worth paying attention to the underlying dynamics of oil prices from a technical perspective to determine the “path of least resistance” for energy-related companies.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Following the surge in oil prices in 2016 as hopes rose for a deal with OPEC to cut production, the outcome of that oil production cut has been less than beneficial. The rush to increase drilling in the Permian Basin by domestic suppliers have more than offset the cuts in production by the OPEC nations. Currently, oil prices remain in a downtrend and the recent failure at the downtrend resistance put’s the mid-$40 level back in focus in the near term.

Furthermore, the recent boost to energy stocks from earnings season has been very short-lived as the bullish breakout of the downtrend from the 2016 highs failed with a break back below the moving average. While energy stocks are oversold, once again, we have continued to recommend being OUT of this sector until the fundamental and technical dynamics improve. There is little evidence of that currently.

Stops should be placed at recent lows.

HEALTH CARE

The health care sector moved from laggard to leader, as anticipated last December, as the raging debate over the repeal/replacement of the Affordable Care Act failed. (Also, as anticipated.) With the future of the ACA now in limbo, it was not surprising to see some profit taking in the sector. However, given that government sponsored support of insurance companies is here to stay, the sector remains a “hold” for now.

Current holdings should be reduced to market-weight for now as there is not a good stop-loss setup currently available. A correction to $75-76 would provide an entry point while maintaining a stop at $73.

FINANCIALS

After a large surge following the election of President Trump, financials have weakened as of late in terms of relative performance. The sector is currently working off the extremely overbought condition and a correction back to support at $23 could provide for an entry point with a stop at $22.50.

There is a tremendous amount of exuberance in the sector at a time that loan delinquencies are rising and loan demand is falling. Caution is advised.

INDUSTRIALS

Industrials, like Financials, relative performance has begun to lag as of late. However, the “Make America Great Again” infrastructure trade is still on. Importantly, this sector is directly affected by the broader economic cycle which continues to remain weak so the risk of disappointment is very high if “hope” doesn’t become reality soon.

While the sector has receded from recent highs, the sector has not reached a deep enough oversold level to warrant an entry. I would reduce holdings back to portfolio weight and take in some of the gains while maintaining a stop below the post-election bullish trendline at $66.

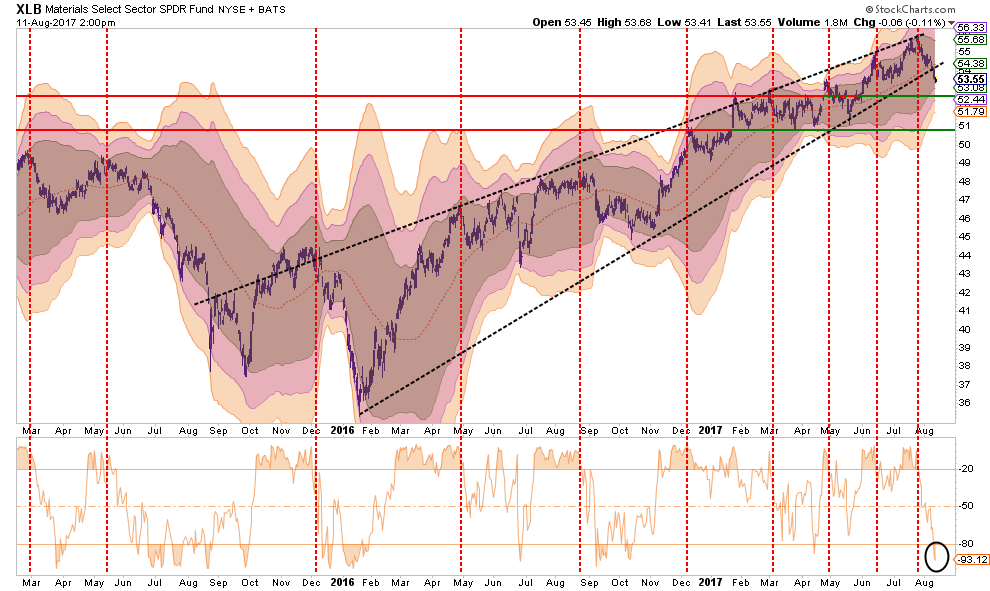

MATERIALS

Basic Materials, also a beneficiary of the dividend / “Make America Great Again” chase is showing a fairly sharp pickup in weakness following a rather lackluster earnings season for the sector. Currently, the very oversold condition of the sector suggests a short-term rally couple present itself to allow for a rebalancing back to portfolio weight. Stops should be set at the recent support of $52.50.

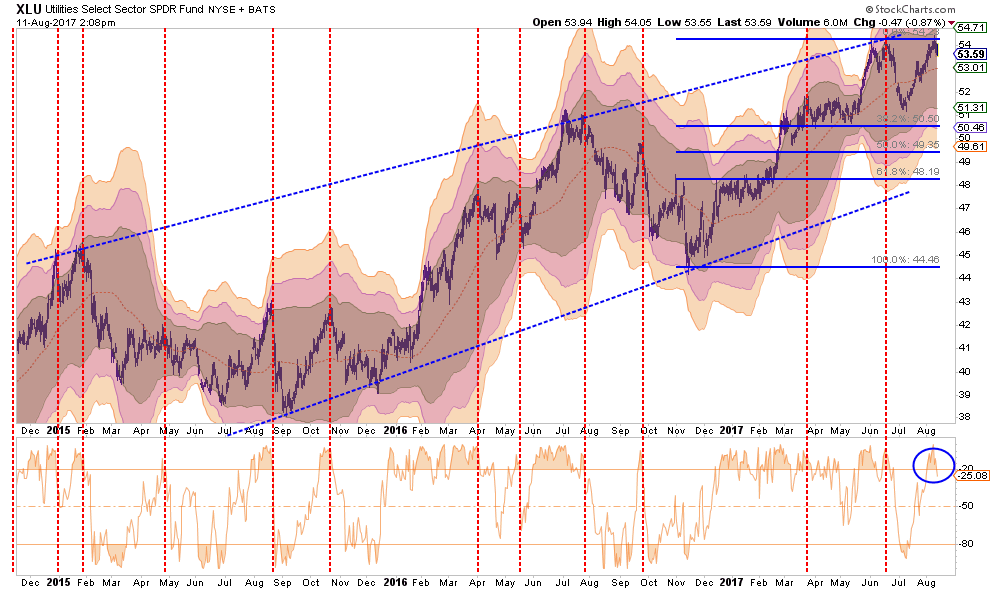

UTILITIES

Back in January, I discussed the “rotation” trade into Utilities and Staples. That performance shift has played out nicely and the sector is now extremely overbought. Utilities have continued to receive the benefit of weaker economic data, and since the sector is interest rate sensitive, have participated with the relative decline in interest rates.

As stated, the sector is now overbought along with interest rates, so reducing the position back to portfolio weight seems prudent. Maintain a stop at $51.00.

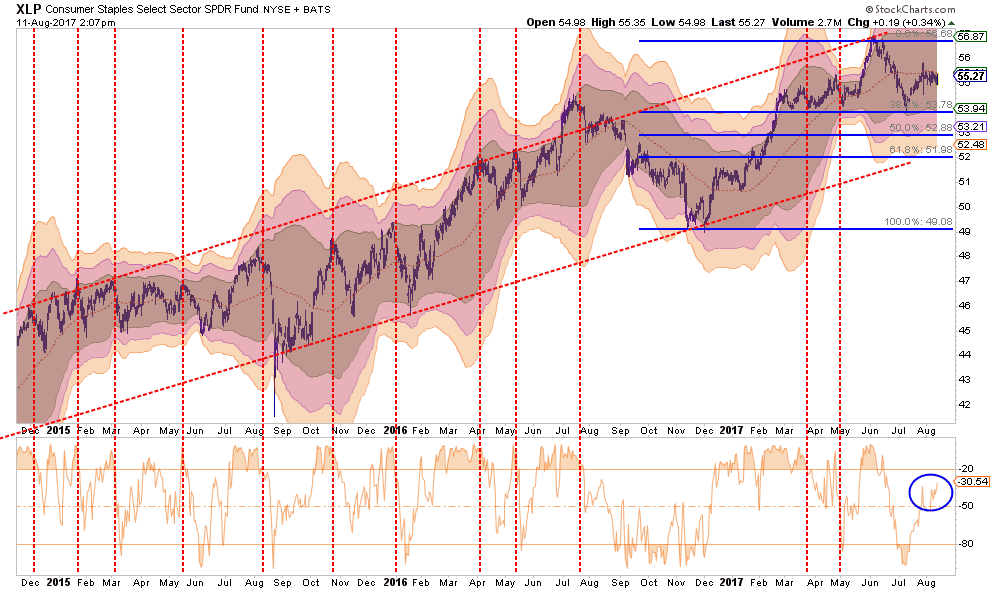

STAPLES

Like Financials, Staples, have been holding support around $54 since March. Currently, the sector is trapped below its short-term moving average but above important support. Reduce overweight exposure until the technical backdrop improves.

Set stops at $53.50.

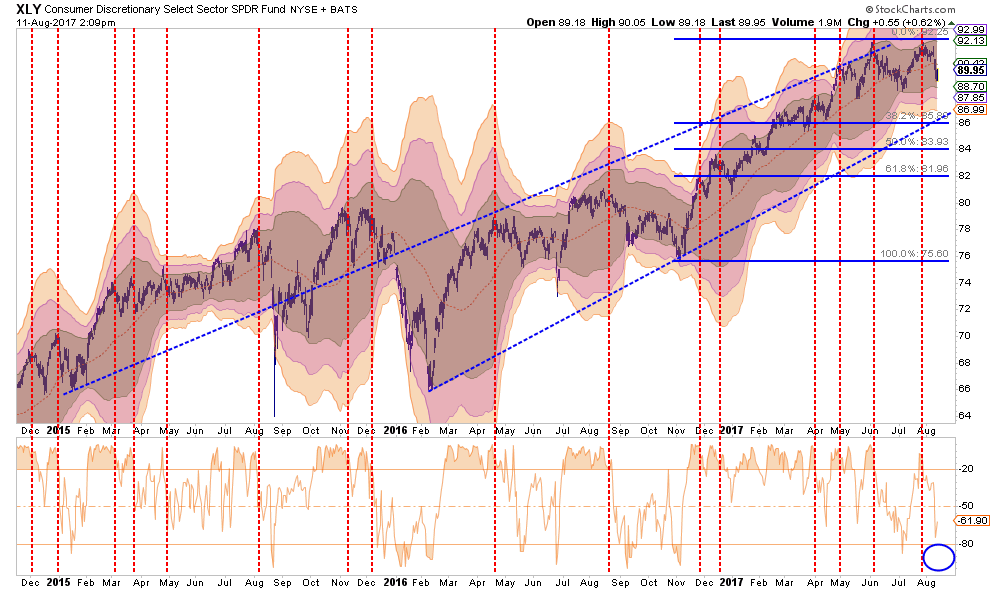

DISCRETIONARY

Discretionary has been running up in hopes the pick-up in consumer confidence will translate into more sales. There is little evidence of that occurring currently, BUT with discretionary stocks near recent highs, profits should be harvested on a rally that fails at the short-term moving average at $90.

Set stops set at $88.50. With many signs the consumer is weakening, caution is advised and stops should be closely monitored and honored.

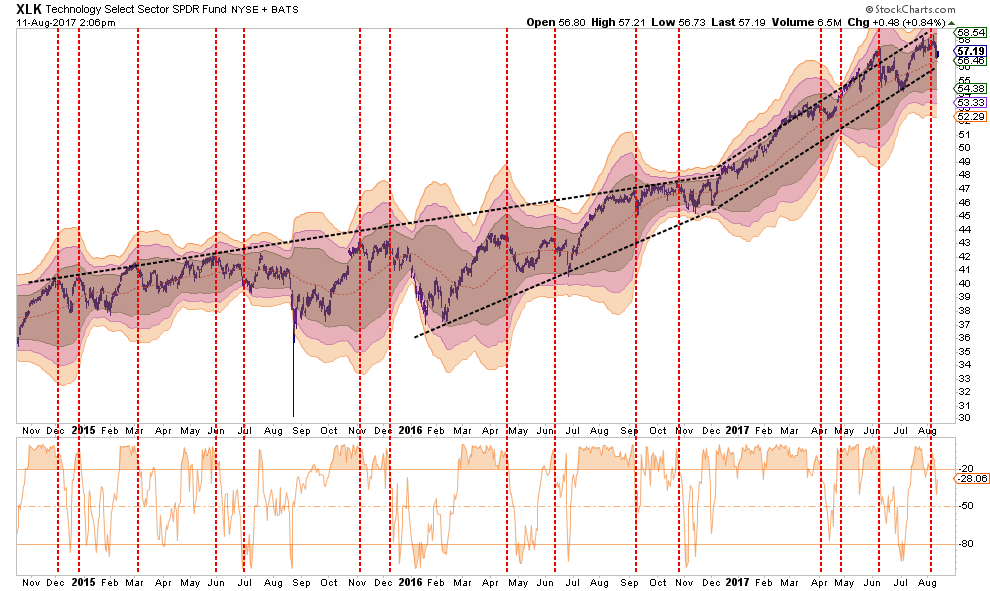

TECHNOLOGY

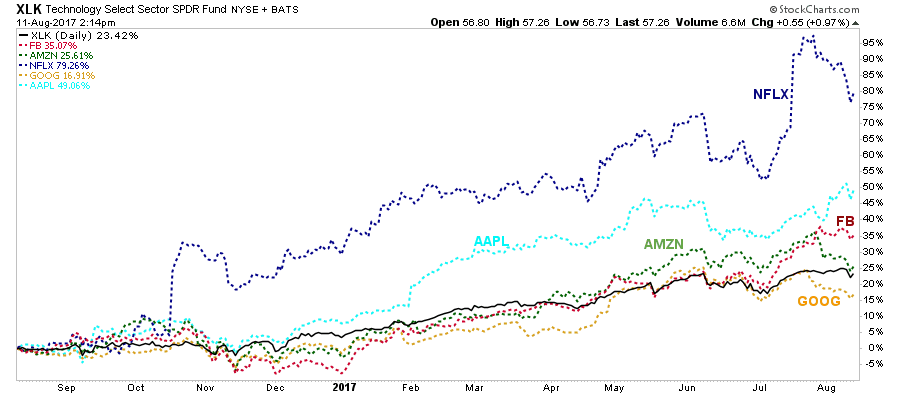

The Technology sector has been the “obfuscatory” sector since the beginning of 2016. Due to the large weightings of Apple, Google, Facebook, and Amazon, the sector kept the S&P index from turning in a worse performance than should have been expected prior to the election and are now elevating it post election.

The so-called FANG stocks (FB, AMZN/AAPL, NFLX, GOOG), for the most part, have continued to support the overall indices due to their large weightings. Watch for weakness in these stocks as a key to the broader market as well.

The sector is overbought and recent weakness could continue. Stops should be moved up to $56 where the bullish trend line currently resides. Weightings should be trimmed back to portfolio weight.

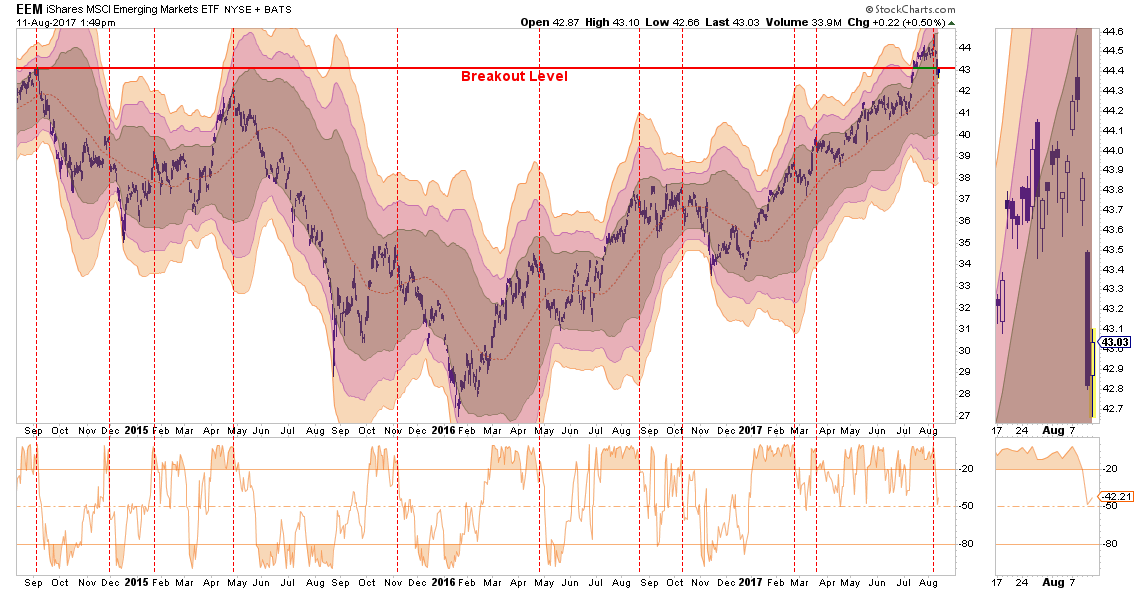

EMERGING MARKETS

Emerging markets have had a very strong performance and recently broke out to all-time highs. This has been helped by the weakening of the US Dollar which has likely neared its end.

Furthermore, the rhetoric that “valuations are cheap” relative to the U.S. is a “false flag.” There have been 6-historical emerging market bubbles in history and they have all failed miserably. The reason is simple. Their economies are DEPENDENT upon the good-will of their neighbors to buy their exports. If the major industrialized countries catch a cold, emerging market economies get the “Flu.” With a recession in the not so distant future, being extremely long emerging markets will likely not play out well.

With the sector beginning to correct an extremely overbought condition, the majority of the gains in the sector have likely been achieved. Profits should be harvested and the sector moved back to normal portfolio weights. There is no reasonable stop level, so a break of $41 can be used for now.

INTERNATIONAL MARKETS

As with Emerging Markets, International sectors are also correcting an extremely overbought condition. Reduce weighting back to portfolio weights by harvesting some profits, and set stops at 64.50.

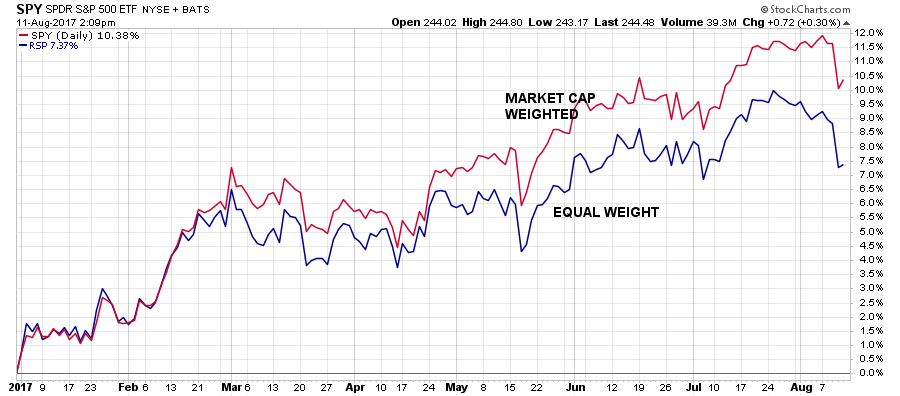

DOMESTIC MARKETS

As stated above, the Technology sector, which is heavily weighted in the S&P 500 index on a market-capitalization weighted basis, has obfuscated much of the weakness in the other sectors of the index. As shown below, the difference in performance since March between the market-cap and equally weighted indices has been significant.

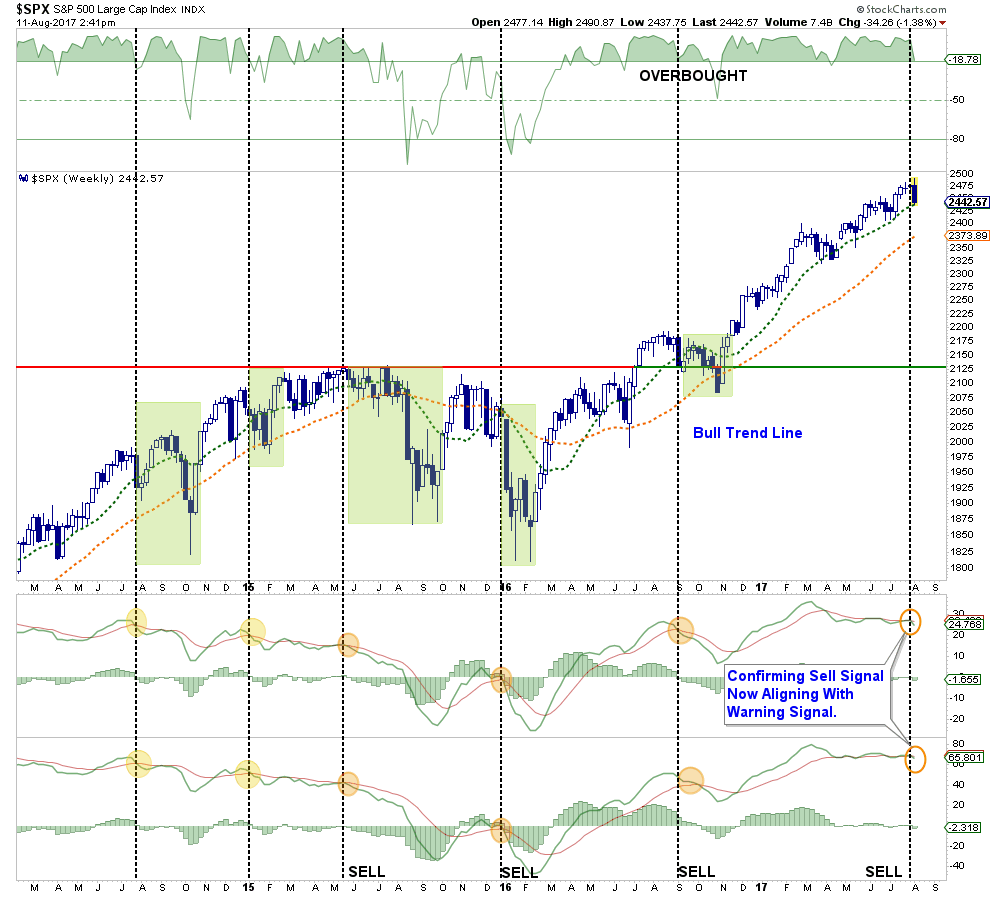

Currently, the S&P 500 remains extremely overbought, overextended, over valued, and overly exuberant. Furthermore, the recent weakness in the market, and sell-off on Thursday, have triggered an initial “sell signal.” Furthermore, a sell signal registered from such a high level has previously coincided with bigger corrections.

Caution is advised for now.

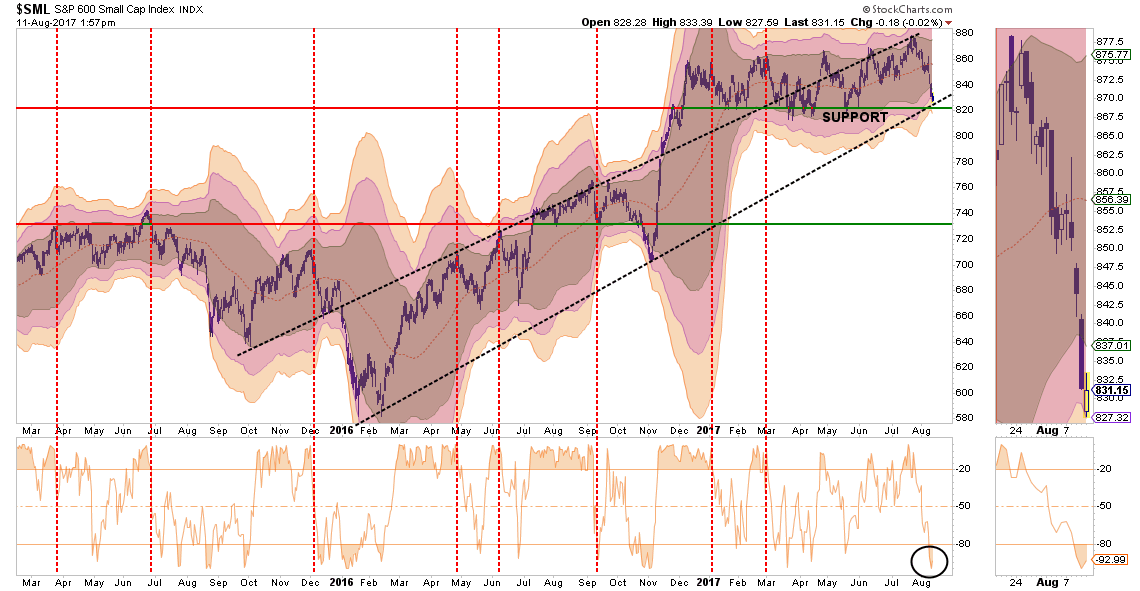

SMALL CAP

Small cap stocks went from underperforming the broader market to exploding following the Trump election. However, as of late, that performance has stalled and the sector has now threatening to violate the bullish trend line and support levels going back to 2016.

Importantly, small capitalization stocks are THE most susceptible to weakening economic underpinnings which are being reflected in the indices rapidly declining earnings outlook. This deterioration should not be dismissed as it tends to be a “canary in the coal mine.”

Currently, small caps are back to an oversold condition which suggests the current corrective process is likely near completion. However, a failed rally attempt and a break below $820 would suggest a much deeper reversion is in process. Reduce exposure back to portfolio weight for now and carry a stop at $820.

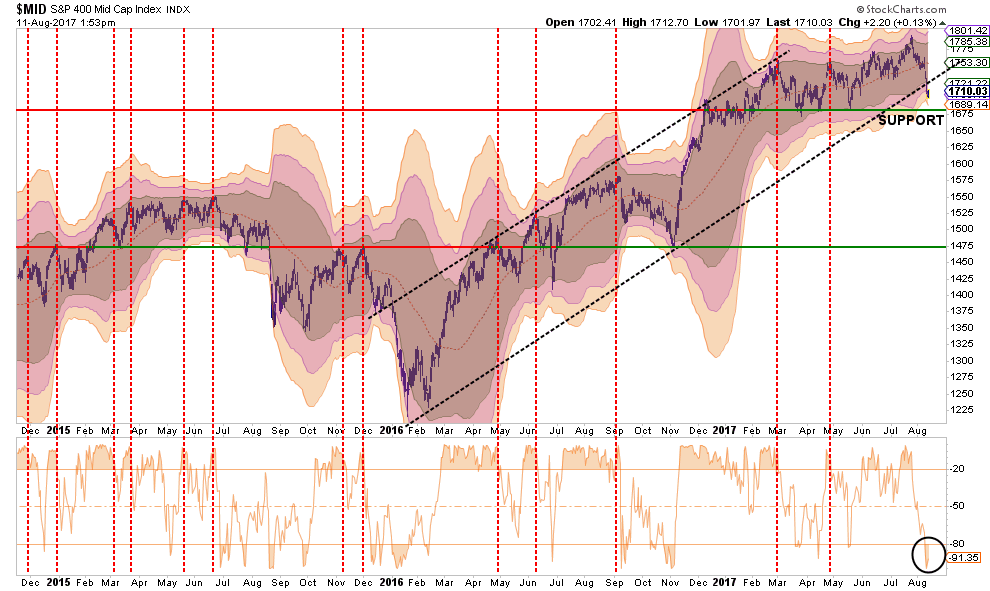

MID-CAP

As with small cap stocks above, mid-capitalization companies had a rush of exuberance following the election. Mid-caps are currently also oversold on a short-term basis, have broken the bullish trend and are threatening lower support levels.

Like small-caps, there may be a short-term investment opportunity forthcoming, but risk is elevated. A rally above $1730 is required to reverse the bearish setup currently. Continue to carry a stop at $1675.

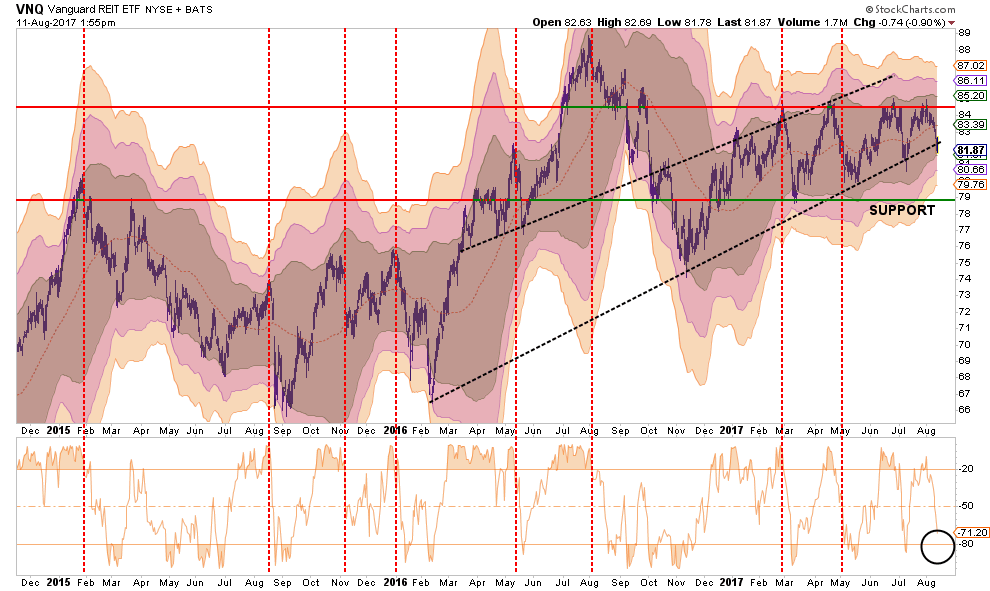

REIT’s

REIT’s have been under pressure and are currently wrestling with their bullish trendlines. However, the sector is now approaching oversold and near support. Hold current positions with a stop set at $80.

TLT – BONDS

Like Utilities, bonds are now overbought and pushing up towards resistance. I wrote previously:

“With the massive ‘short interest’ position currently outstanding on bonds, a retracement of the previous decline to anywhere between $126 and $132 is very possible.”

That call was very contrarian to mainstream analysts who were calling for a bond “bear market” at the time. With bonds back to extreme overbought conditions, take some profits and reduce holdings back to portfolio weights.

Stops should currently be set at $122.

IMPORTANT NOTE:

If you go back through all the charts and note the vertical RED-DASHED lines, you will discover that each time previously these lines denoted the peak of the current advance. Overall, in the majority of cases above, the risk/reward of the market is NOT favorable.

If, and when, the market corrects some of the short-term overbought conditions which currently exist, equity risk related exposure can be more aggressively added to portfolios.

Just be cautious for the moment.

It is much harder to make up losses than simply adding preserved cash back into portfolios.