Written by Lance Roberts, Clarity Financial

Last week I penned an article questioning “Is This The Bubble?”

Not surprisingly, it didn’t take long for someone to ask THE question.

Please share this article – Go to very top of page, right hand side, for social media buttons.

First, let me show you where it is in 3-charts.

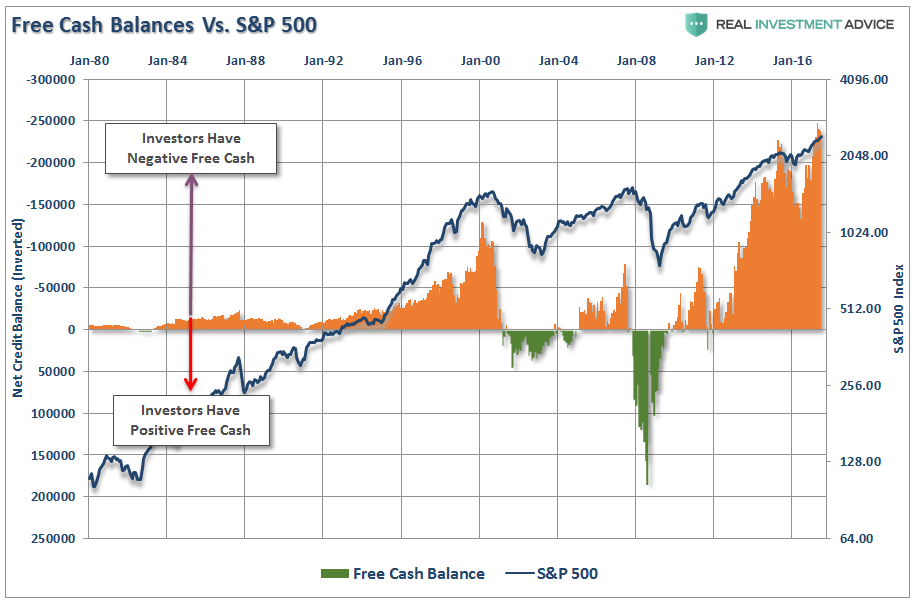

Leverage

The level of negative net credit balances is near the highest level on record. While margin debt is not a problem as long as markets are rising as leverage fuels the bullish advance, it burns uncontrollably on the way down.

Exuberance

The following chart is a composite gauge built on several measures of investor psychology as noted. I have also smoothed the index using a 4-week moving average.

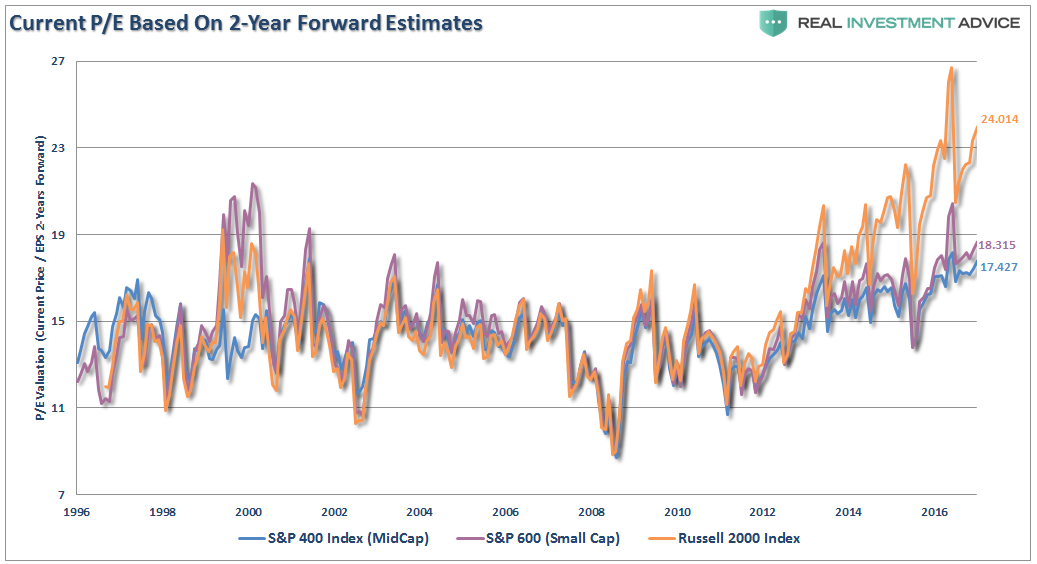

Valuations

We can look at valuations in small to mid-capitalization companies as a measure of speculation in the markets. With the Russell 2000 and Small Cap 600 currently running near all-time valuation levels, and Mid Cap 400 at record levels, based on earnings estimates 2-years forward (which are always overstated), there is little to suggest speculation is not currently running rampant.

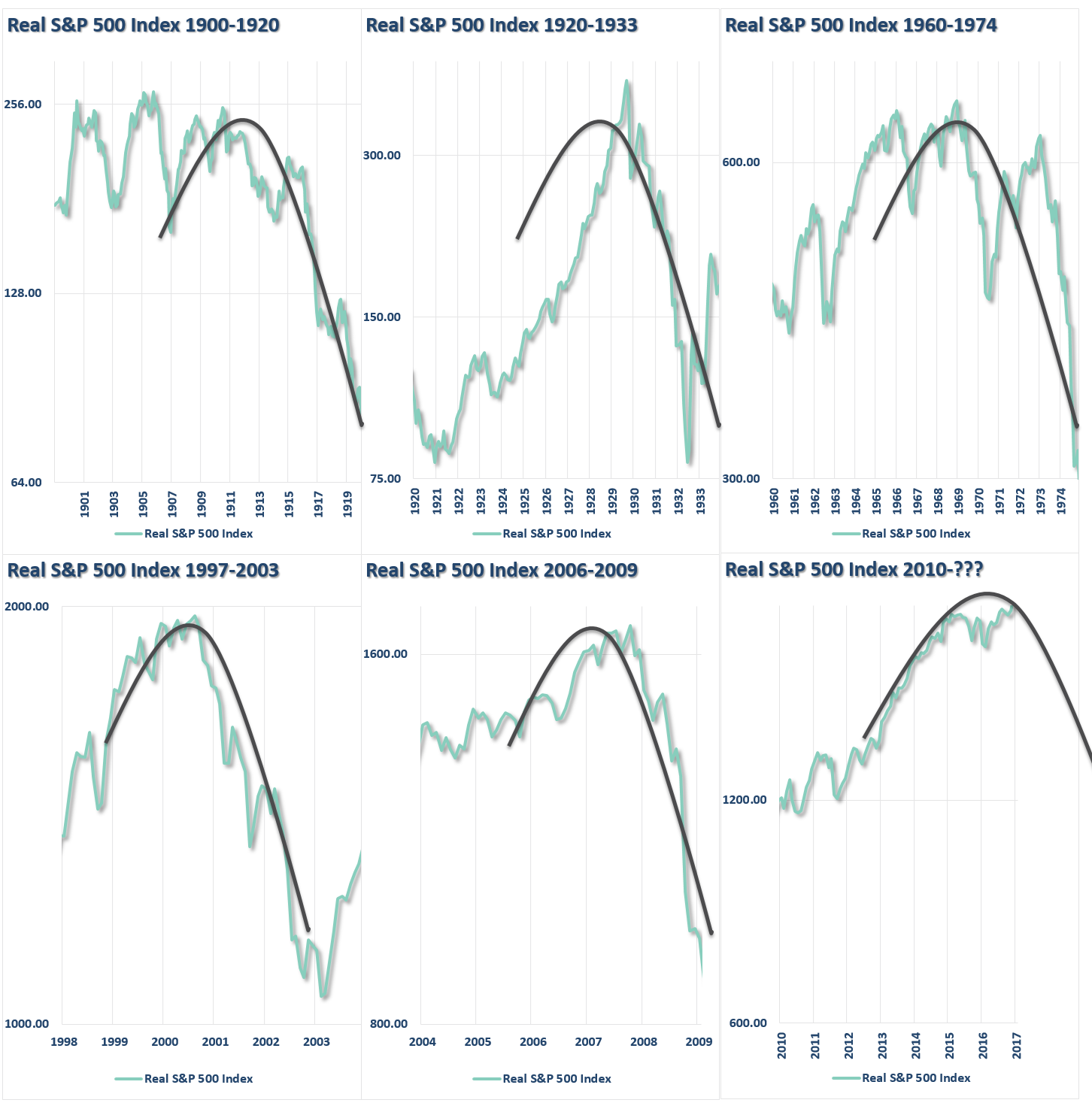

Unfortunately, bubbles are never seen in advance. The chart below is an example of asymmetric bubbles.

This idea of asymmetric bubbles was discussed by George Soros who stated:

“Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions.”

Soros’ view on the pattern of bubbles is interesting because it changes the argument from a fundamental view to a technical view. Prices reflect the psychology of the market which can create a feedback loop between the markets and fundamentals. As Soros stated:

“Financial markets do not play a purely passive role; they can also affect the so-called fundamentals they are supposed to reflect. These two functions, that financial markets perform, work in opposite directions. In the passive or cognitive function, the fundamentals are supposed to determine market prices. But, in the active or manipulative function market, prices find ways of influencing the fundamentals.

When both functions operate at the same time, they interfere with each other. The supposedly independent variable of one function is the dependent variable of the other, so that neither function has a truly independent variable. As a result, neither market prices nor the underlying reality is fully determined. Both suffer from an element of uncertainty that cannot be quantified.”

The chart below utilizes Dr. Robert Shiller’s stock market data going back to 1900 on an inflation-adjusted basis. I then took a look at the markets prior to each major market correction and overlaid the asymmetrical bubble shape as discussed by George Soros.

There is currently much debate about the health of financial markets. Have we indeed found the “Goldilocks economy?” Can prices can remain detached from the fundamental underpinnings long enough for an economy/earnings slow down to catch back up with investor expectations?

The speculative appetite for “yield,” which has been fostered by the Fed’s ongoing interventions and suppressed interest rates, remains a powerful force in the short term. Furthermore, investors have now been successfully “trained” by the markets to “stay invested” for “fear of missing out.”

The increase in speculative risks, combined with excess leverage, leave the markets vulnerable to a sizable correction at some point in the future. The only missing ingredient for such a correction currently is simply a catalyst to put “fear” into an overly complacent marketplace.

In the long term, it will ultimately be the fundamentals that drive the markets. Currently, the deterioration in the growth rate of earnings, and economic strength, are not supportive of the current levels of asset prices or leverage. The idea of whether, or not, the Federal Reserve, along with virtually every other central bank in the world, are inflating the next asset bubble is of significant importance to investors who can ill afford to, once again, lose a large chunk of their net worth.

It is all reminiscent of the market peak of 1929 when Dr. Irving Fisher uttered his now famous words: “Stocks have now reached a permanently high plateau.” The clamoring of voices proclaiming the bull market still has plenty of room to run is telling much the same story. History is replete with market crashes that occurred just as the mainstream belief made heretics out of anyone who dared to contradict the bullish bias.

It is critically important to remain as theoretically sound as possible. The problem for most investors is their portfolios are based on a foundation of false ideologies. The problem is when reality collides with widespread fantasy.

Does an asset bubble currently exist? Ask anyone and they will tell you “NO.” However, maybe it is exactly that tacit denial which might just be an indication of its existence.