Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

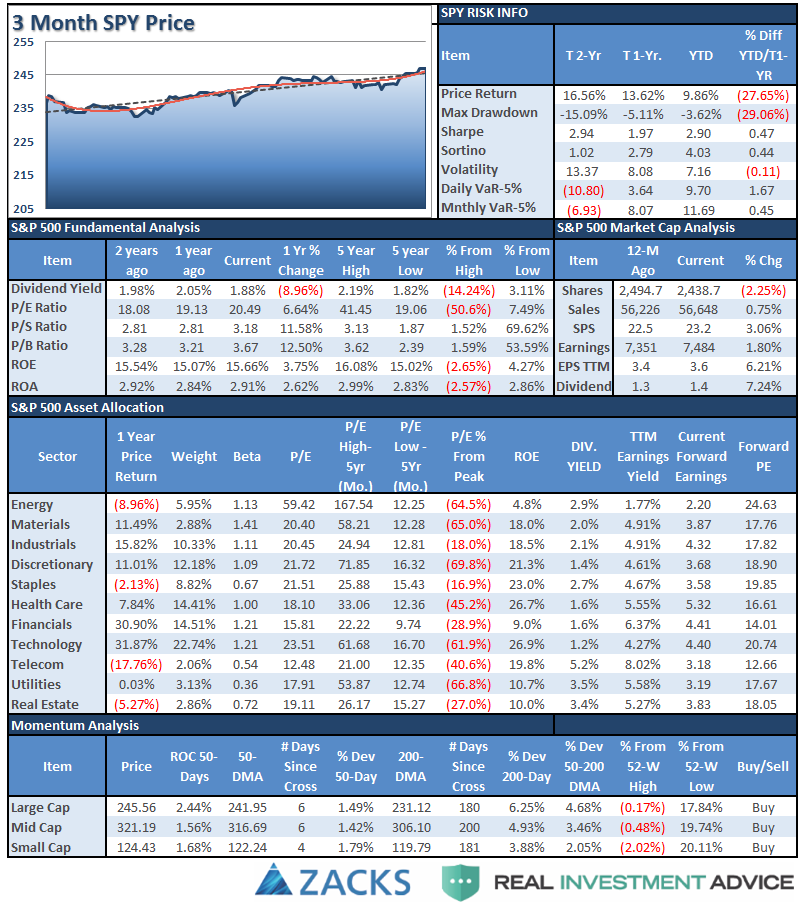

S&P 500 Tear Sheet

Performance Analysis

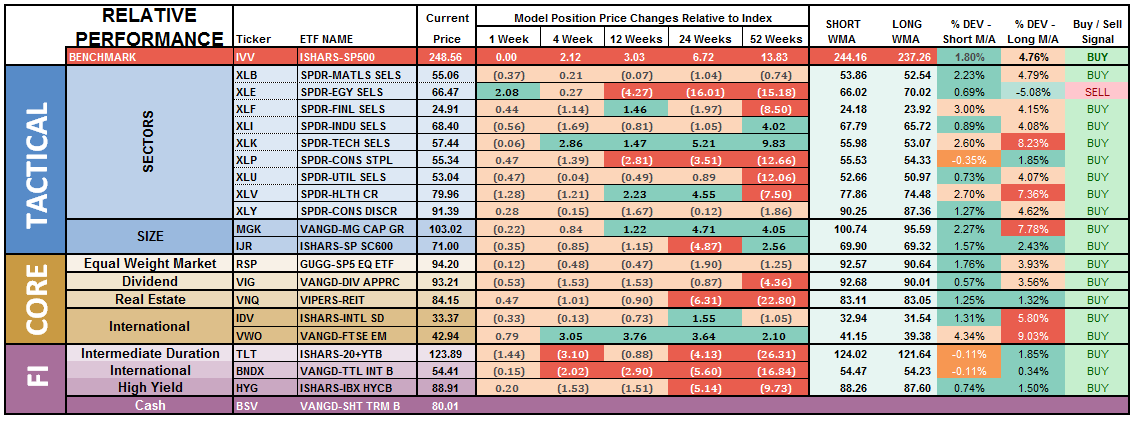

ETF Model Relative Performance Analysis

Sector Analysis:

This past week, the markets struggled with recent highs as tight trading ranges with limited drawdowns have been common place. Not much changed this week from last week, but groupings of sectors, in terms of relative performance, have become much tighter.

Health Care, Materials, Financials, and Industrials continued to perform better this week relative to the S&P 500 index itself. However, that outperformance is beginning to show signs of deterioration.

Staples, Utilities, Technology, and Discretionary were weaker on a relative basis but are still holding bullish trends so nothing much to worry about at this juncture other than just tightening up stop levels and watching sector rotation and leadership changes.

Energy – wait…WHAT IS THAT? Over the last few months, I have been discussing the declining trend of energy stocks due to the weakness in oil prices. With both extremely oversold, we finally saw a rash of short-covering this past week pushing both the commodity and energy sector higher.

It is still TOO early to institute positions in oil as we need to see oil prices stabilize above $48/bbl. Also, estimates for energy companies are being rapidly slashed for the rest of the year so we need to see stabilization there as well. However, with that said, energy is back on the radar for a potential entry point. Let’s give it another week and reassess our positioning next week.

Small and Mid-Cap stocks continued to gain ground on performance relative to the S&P 500 index which keeps positions long in portfolios. Hold current positions and move stops up to the moving averages.

Emerging Markets and International Stocks as noted two week’s ago the bullish “buy point” occurred which allowed us to add international exposure to portfolios. However, the subsequent explosion of these sectors higher reduces the opportunity somewhat until there is some correction to work off the excessive overbought condition. That has not occurred currently, continue to be patient for a better entry point.

Gold – is once again trying to muster a rally from extremely oversold conditions. There is a good bit of work to do before this sector becomes interesting, but the move last week above the 200-dma does put the commodity back onto our radar for now.

S&P Dividend Stocks, after adding some additional exposure recently we are holding our positions for now with stops moved up to recent lows. With the sector becoming overbought, wait to add new exposure until a better opportunity presents itself.

Bonds and REIT’s both took a hit, but recovered a bit, from a rather surprising spike in rates. With inflationary pressures declining on every front, the most likely path for rates is lower. The drop in bond prices back to support can allow for adding bond exposure to portfolios if needed. Any push back towards 2.4% continues to be an ideal zone to add bonds and REIT’s to portfolios.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

The bullish trend remains positive, which keeps us allocated on the long side of the market for now. However, more and more “red flags” are rising which suggests a bigger correction may be in the works over the next couple of months.

Several weeks ago, during the correction, we added modestly to our core holdings for the second time this year. Then, with the breakout of the market week before last, we added further to our portfolio positions and increasing exposure again. We also added to our bond holdings as well as rates hit our buy targets.

Stops have been raised to trailing support levels and we continue to look for ways to “de-risk” portfolios at this late stage of a bull market advance.

We remain invested. We just remain cautious and highly aware of “risks” to capital.