Written by Lance Roberts, Clarity Financial

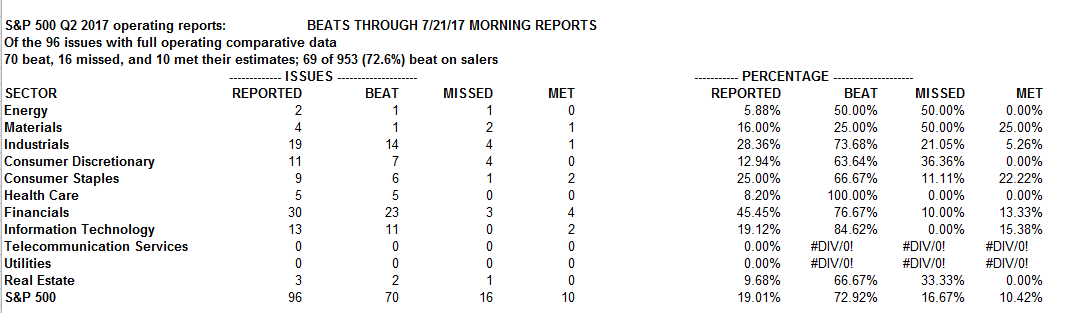

This past week, despite the Fed’s “non-event” meeting, the story of the market has been earnings. As of July 20th, the latest update from S&P 500 showed the statistics shown below.

Please share this article – Go to very top of page, right hand side, for social media buttons.

With a slew of new companies reporting this week these numbers will change, but not drastically so.

While the backdrop of 72.92% of companies beating estimates is certainly bullish, it should be remembered these “beats” come from two primary factors:

1) Lowered estimates

As my friend Anora Mahmudova recently wrote:

“But despite positive quarterly reports, an analysis of earnings calls suggests optimism may have peaked, the analysts said in a note, observing ‘a drop-off in mentions of ‘better’ relative to ‘worse’ or ‘weaker’ words.’

Moreover, the cut to third-quarter consensus earnings-per-share estimates is so far the largest since the fourth quarter of 2015, when profit growth was still declining and recession fears were percolating.”

“The rapid deterioration in outlook is worrisome due to stretched valuations and other macro risks.”

As she notes, the upside in the market is limited, given already stretched valuations. If markets rise further from here, it will be due to euphoria rather than fundamentals. With health care reform failing to be passed, the legislative agenda of tax reform is now officially dead because it had to be done through reconciliation. Furthermore, the risk of a debt ceiling debate looms as well as potential policy errors by the Federal Reserve.

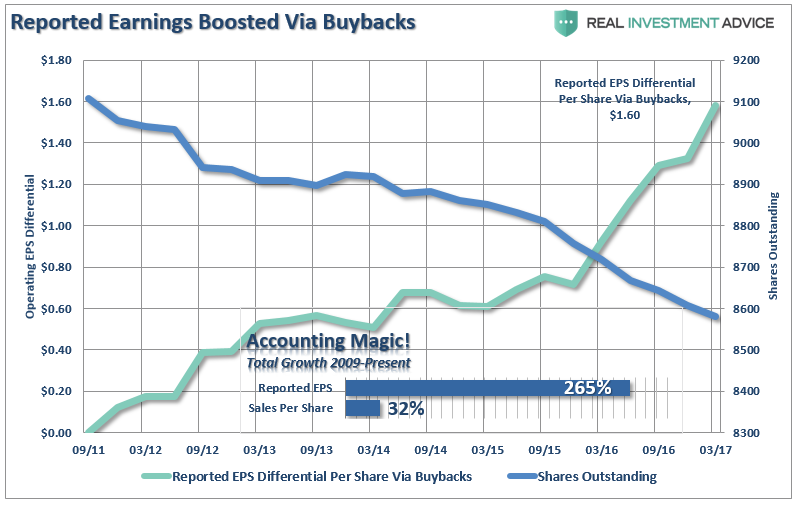

2) Share buybacks

Yes, earnings look good, only due to the fact that 72.94% of the companies n the S&P 500 have lower shares outstanding than just one year ago. One of the best ways to show the impact of lowered shares as it relates to higher operating profits is as follows: (For more information read this.)

It has been these share buybacks that have allowed companies to win the“beat the estimate” game which has kept the bulls clearly in charge of the markets and our portfolios allocated on the long-side currently.

However, in the longer-term, the benefits derived from continuing levels of share reductions, accounting gimmicks, wage suppression, etc. are finite. (Read more here) As shown above, with total top-line revenue growth since 2009 running at a very weak 32%, there is not a tremendous amount of wiggle room to offset a drop in consumer demand or a weaker economic outlook.