Written by Lance Roberts, Clarity Financial

Last week, I discussed “why” interest rates can NOT much substantially higher from current levels.

Please share this article – Go to very top of page, right hand side, for social media buttons.

To wit:

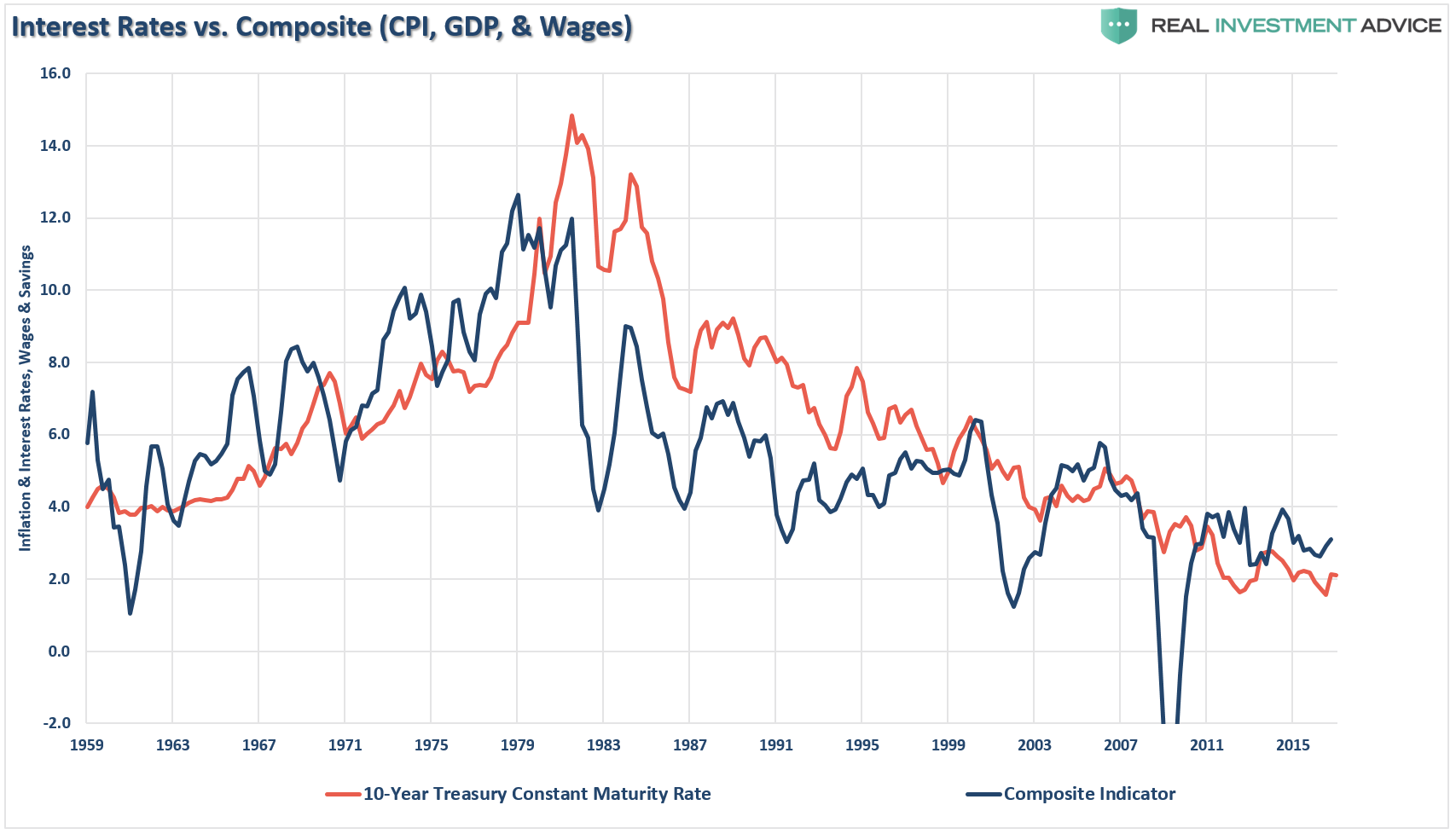

“As I have discussed many times in the past, interest rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be clearly seen in the chart below by combining inflation, wages, and economic growth into a single composite for comparison purposes to the level of the 10-year Treasury rate.”

“As you can see, the level of interest rates is directly tied to the strength of economic growth and inflation.”

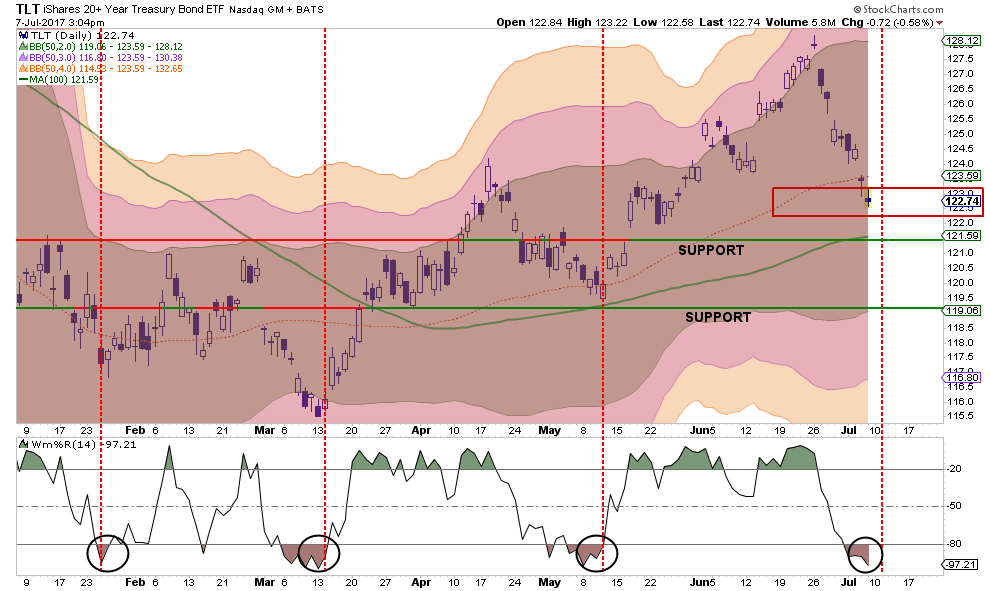

This week, I want to look at interest rates from a purely technical point. Interest rates, like stock prices, are bound by the laws of physics. Prices can move only so far in one direction, before eventually returning to the mean. When rates plunged from 2.6% to 2.15% recently, bond prices had become extremely overbought and some correction action was expected.

I have been recommending to readers over the last couple of months to withhold adding bond positions given the level of richness in bond prices. That advice has played well, and the recent spike in interest rates has pushed bond prices to important levels of support while reducing much of the previous overbought condition.

As noted last week:

“However, bonds are not yet oversold. Therefore, we will hold off on adding to existing bond exposures, or adding new positions, this week with the expectation rates could rise a bit further.”

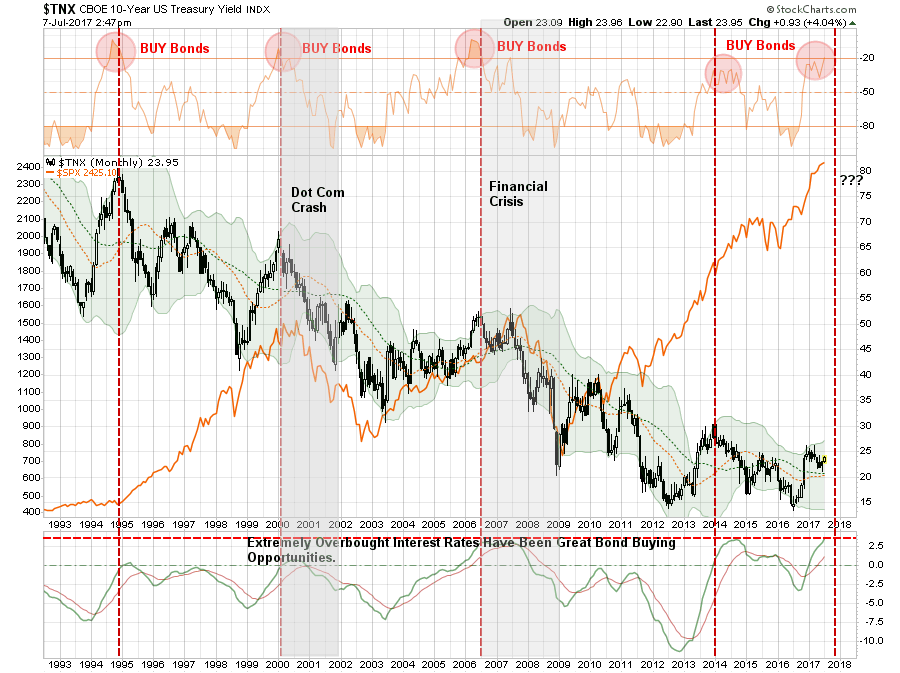

The rise in rates last week has pushed the 10-year yield to some of the highest “overbought” conditions witnessed in the past 25-years. Each time rates have been at these levels previous TWO things have happened.

- There was an economic or financial market backlash, and;

- It was a great time to buy bonds.

Sure. Maybe this time IS different and rates will “magically” decouple from the underlying drivers of economic and inflation and go spiraling higher. Such an event would last about 37-seconds until higher borrowing costs choke off what bit of nascent economic growth we currently have.

As David Rosenberg noted this past week:

“In fact, when you go back and look at the announcements of QE1, QE2, and QE3, the Treasury market actually did not rally on these … but the stock market sure did! And you know what, in those intermittent periods when the Fed stopped its balance sheet expansion (only to then precipitate the next round), the ensuing pullback in risk appetite and the correction in the S&P 500 actually caused the bond market to rally on the safe-haven effect!”

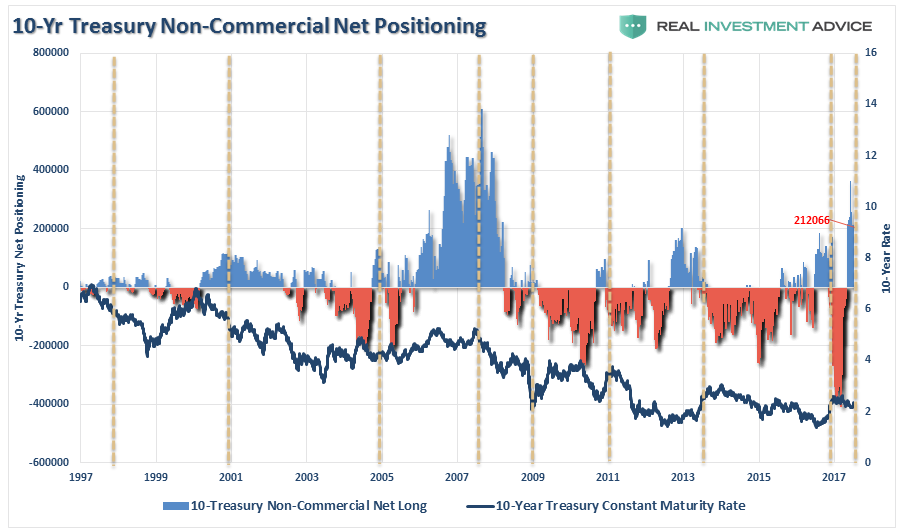

Furthermore, the net positioning of commercial traders also recently reached a peak LONG position in bonds, historically the reversal of such a net long, to a net short position, has denoted the peak in interest rate increases and a prime opportunity to buy bonds. That reversal has already begun.

However, as noted in the chart above, when the economy slips into the next recession, interest rates will once again join the long-term downtrend towards 1% or less.

Bonds will be the right place to be. Stocks won’t be.

So, as I stated, we are looking to BUY bonds…and will likely start nibbling at positions next week.