Written by Lance Roberts, Clarity Financial

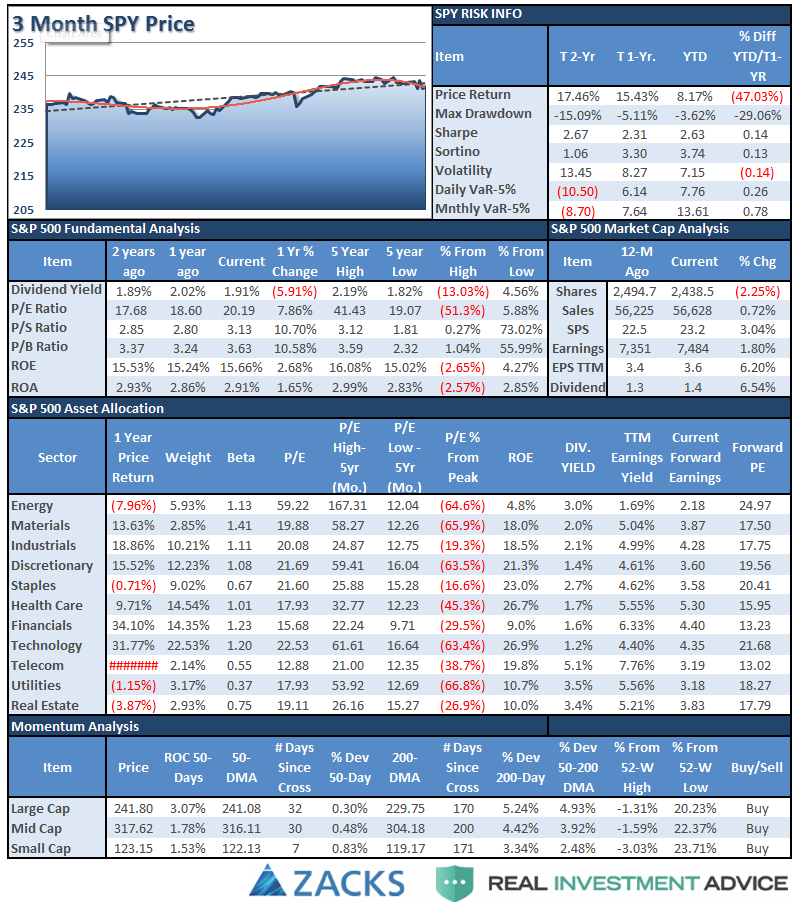

S&P 500 Tear Sheet

The “Tear Sheet” below is a “reference sheet” provide some historical context to markets, sectors, etc. and looking for deviations from historical extremes.

Please share this article – Go to very top of page, right hand side for social media buttons.

If you have any suggestions or additions you would like to see, send me an email.

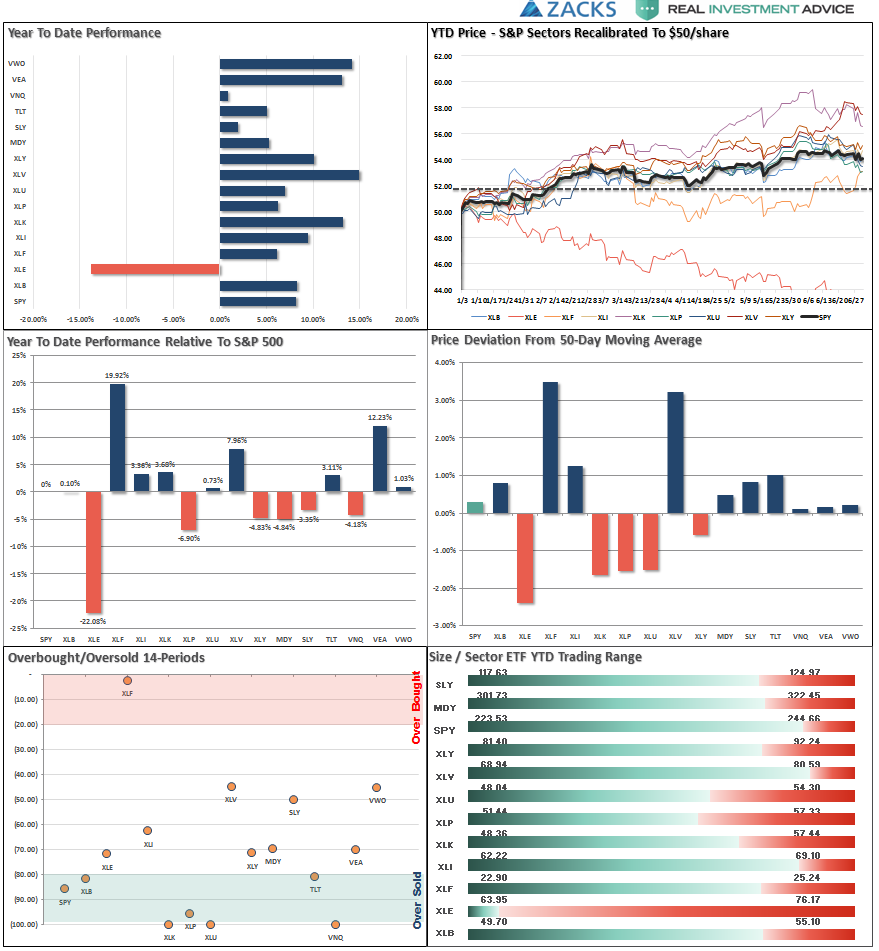

Performance Analysis

New! Thank you for all the comments on the performance analysis below. Due to many of the emails I got, I have swapped out the sector weight graph for a year-to-date performance range analysis. Keep the comments coming. (Email Me)

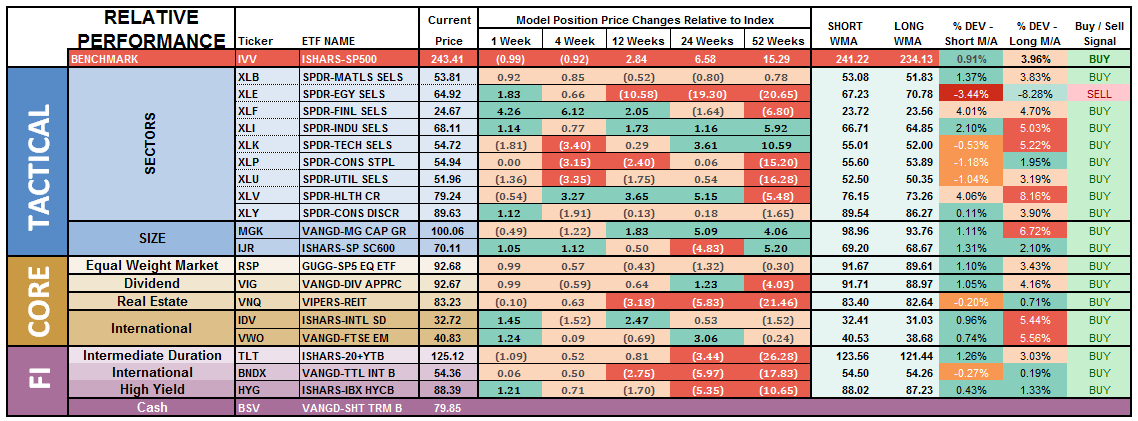

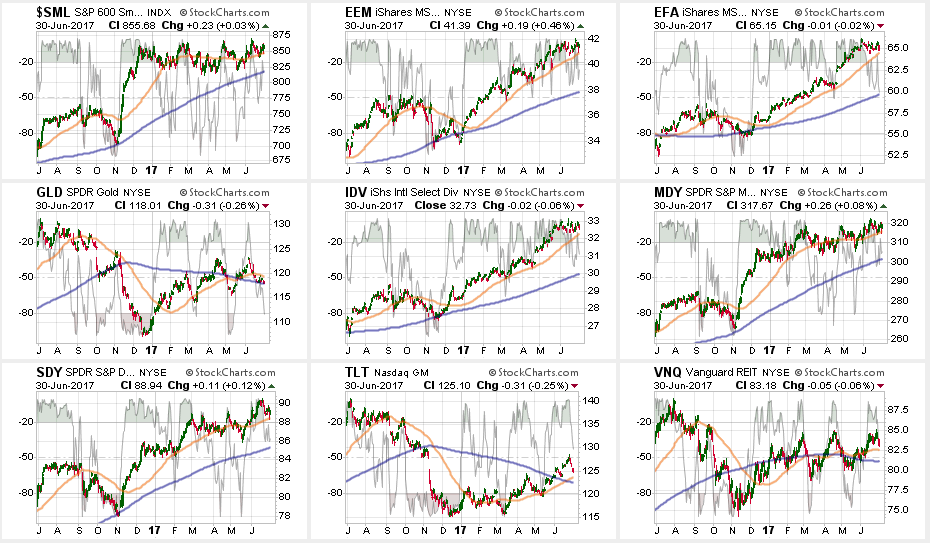

ETF Model Relative Performance Analysis

Sector Analysis

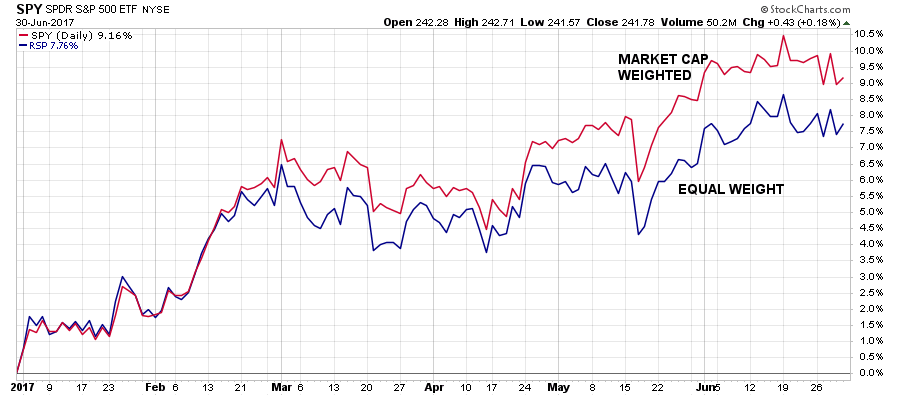

Taking a look at the individual sectors of the S&P 500, we see a bit more deterioration than what the market currently reflects. This is due to the heavy weightings of certain sectors of the market which can skew the index somewhat versus what is happening internally. This can be more clearly seen by looking at a chart which compares an EQUAL weight to a market-capitalization weighted S&P 500 index:

Let’s look at the damage occurring internally at the moment.

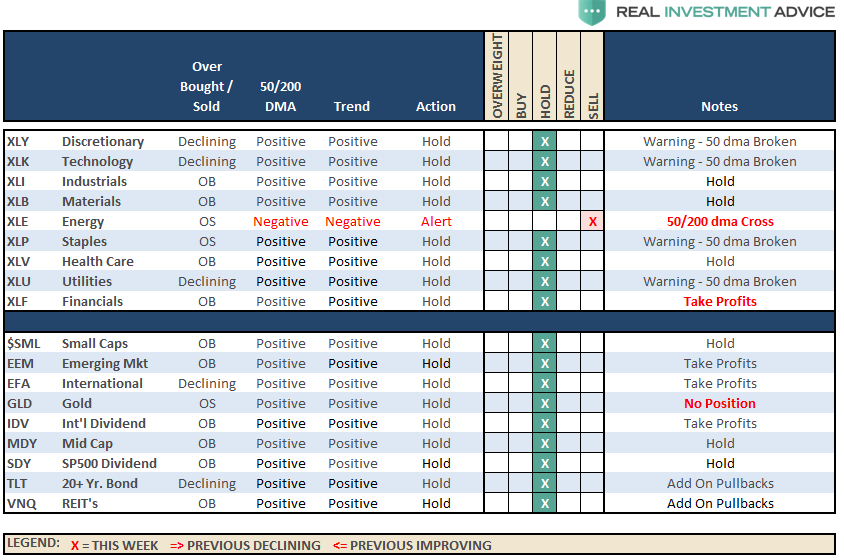

Technology, Discretionary, Utilities, and Staples continued their recent weakness, with all sectors having now BROKEN their respective 50-dma’s. The correction does set up a potential trading opportunity provided support holds, but the break below the 50-dma raising a warning flag. If current supports in these sectors give way, we will recommend reducing overall portfolio weightings.

Financials, Health Care, Materials, and Industrials again maintained their lead as money flows rotated primarily in Financials out of Tech and Discretionary. All of these sectors remain overbought so some profit-taking and rebalancing is advised.

Energy – Oil prices rallied last week, finally, as noted in the main missive above. The supply of oil remains a problem with rig counts rising and economic weakness prevalent. With a major sector sell signal, and the cross of the 50-dma below the 200-dma, we remain out of the space for the time being. Use any rally to reduce exposure accordingly until the technical trends improve.

Small and Mid-Cap stocks regained their respective 50-dma’s which removes their warning signs but remained weak relative to the broader market. This keeps concern elevated at the moment, however, maintain exposure for now, but do so cautiously with stops at support.

Emerging Markets and International Stocks as noted previously:

“There is a good bit of risk built into international stocks currently. We took profits a few weeks ago, but the recent extension suggests another round of rebalancing is likely wise. Take profits and rebalance sector weights but continue to hold these sectors but stop levels should be moved up to the 50-dma.”

A pull back to support will provide an opportunity to rebalance holdings in the short-term. The consolidation in industrialized internal markets is bullish and a potential point to add exposure may be approaching. We will update next week if such becomes the case.

Gold – The failure of the precious metal at critical resistance of 1300/oz keeping us out of our long-term positions currently. The short-term trading positions were also stopped out on the drop below $1260/oz for now. With Gold back below the 50-dma, caution remains advised with hard stops set on a break below $1240/oz or the 200-dma.

S&P Dividend Stocks, along with other more interest rate sensitive sectors, are being sold on the technical bounce in interest rates this past week. We have recommended previously taking profits in these sectors which now provides an opportunity to add exposure at a lower cost as this opportunity develops. Continue to hold current positions but maintain stops at the recent lows.

Bonds and REIT’s were hit with the profit taking we recommended last week. With the 50-dma’s moving upward, these sectors are attractive but extremely overbought. Wait for a pullback to add to exposures.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

The bullish trend remains positive, which keeps us allocated on the long side of the market for now. However, more and more “red flags” are rising which suggests a bigger correction may be in the works over the next couple of months.

Two weeks ago, during the correction, we added modestly to our core holdings for the second time this year. However, we are still maintaining slightly higher levels of cash currently.

We are currently holding positions in portfolios with near full exposure. We did rebalance positions last week, like Health Care and Technology, which had large run-ups and were grossly extended.

As I stated last week:

“While I am not excited about the overall risk/return makeup of the market currently, as a portfolio manager it is the discipline and strategy that drives action. Everything else is secondary.”