Written by Lance Roberts, Clarity Financial

Last week the Fed hiked their lending rate 1.25% which is the highest level since the financial crisis. More importantly, they announced they will consider beginning to allow their $4.5 Trillion balance sheet to begin to reduce by not “reinvesting” proceeds from redemptions and interest payments.

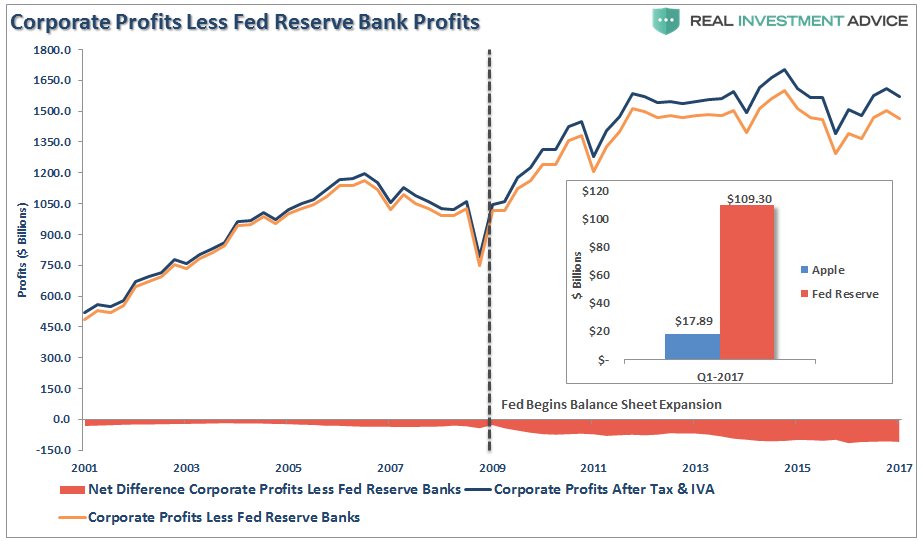

First, just so you know, the Fed’s balance sheet inflates two important things besides asset prices: 1) corporate profits, and 2) government revenues.

I addressed in “Earnings Vs. Profits & The Bull Market” the impact of the Fed’s balance sheet on corporate revenues. To wit:

“The profits generated by the Federal Reserve’s balance sheet are included in the corporate profits discussed here. As shown below, actual corporate profitability is weaker if you extract the Fed’s profits from the analysis. As a comparison, in the first quarter of 2017, Apple reported a net income of just over $17 billion for the quarter. The Fed reported a $109 billion profit.”

With respect to government revenues, it is also not a minor issue. The Federal Reserve can NOT buy bonds directly from the Treasury. When the Treasury issues bonds to fund the difference between Government revenues and expenses, the deficit, those bonds are sold to the 20-primary dealers. When the Fed is active doing “Quantitative Easing,” the Fed creates a “swap” with the primary dealer by crediting their reserve account and the Fed now owning the bonds.

Here is the interesting thing. When the Treasury pays the interest on the bonds, that interest is accounted for as an “expense” for the Government. Periodically, the Fed remits “profits” back to the Treasury which is essentially returning to the Treasury the interest payments received by the Fed. These profits, or returned interest payments, are then counted as “revenue” for the Government.

How much is that you ask? In 2016, it was $92.7 Billion which was slightly lower than the previous record of $97.7 Billion in 2015 which was up from $96.9 Billion in 2014. So, in the years ahead, as the Fed reduces their balance sheet, the income to the Treasury will also fall.

I digress.

Now, nearly a decade after the start of the financial crisis, the Fed has announced its plan for shrinking the size of its balance sheet. From Business Insider:

“The basic idea is that the Fed will stop reinvesting the principal of securities when they mature.

Put another way, when a 10-year Treasury on the Fed’s books comes due, the money it gets back from that investment will not be used to go out and buy another Treasury.

The slowing of reinvestment will be phased in over time. To start, the Fed will invest money back into the market only if it gets back more than $6 billion in principal returned a month. From there, the ‘cap’ will increase by $6 billion every three months over the course of a year until it hits $30 billion a month.

The Fed said it would ultimately have a balance sheet ‘appreciably below that seen in recent years but larger than before the financial crisis’ in part because the Fed expects banks to maintain higher demand for reserves supplied by the central bank. But that is a pretty broad endpoint given that the Fed held roughly $800 billion in assets before the financial crisis and $4.5 trillion now.”

The fact the Fed will not be SELLING Treasuries to reduce the balance sheet is why interest rates did not move up appreciably following the announcement.

However, for those that believe this is a “bulletproof” market, this announcement means a great deal.

As I have shown you previously, the Fed’s timing of the reinvestment of proceeds back into the market has acted as a “Stealth QE” to support asset prices against an economic or geopolitical shock.

That activity has also acted to suppress volatility in the markets by providing the “Fed Put” to keep investors betting on the “long side.”

Axel Merk summed up well what happens when these things run in reverse:

“I have little doubt that a substantial driver of low volatility may be central banks. Low interest rates and quantitative easing (QE) compress risk premia; in plain English, this means not only that junk bonds trade at a lower premium over Treasuries, but that perceived risk is reduced in all markets, including equities, causing volatility to be lower. When central bankers ‘do whatever it takes,’ it is no surprise that investors chase yield without being concerned about negative consequences.

But when central bankers ‘taper’ their purchases, odds are that volatility comes back as taper tantrums have shown.”

He is right, there is very little concern about the risk being taken on by investors currently without any regard for the underlying risk as they chase “yield and return.”

The forgotten piece of this “fairytale” is that RISK = How much you LOSE when you are wrong.

Currently, the risk/reward ratio is currently heavily skewed against investors in both the short, intermediate and long-term outlook.