Written by Lance Roberts, Clarity Financial

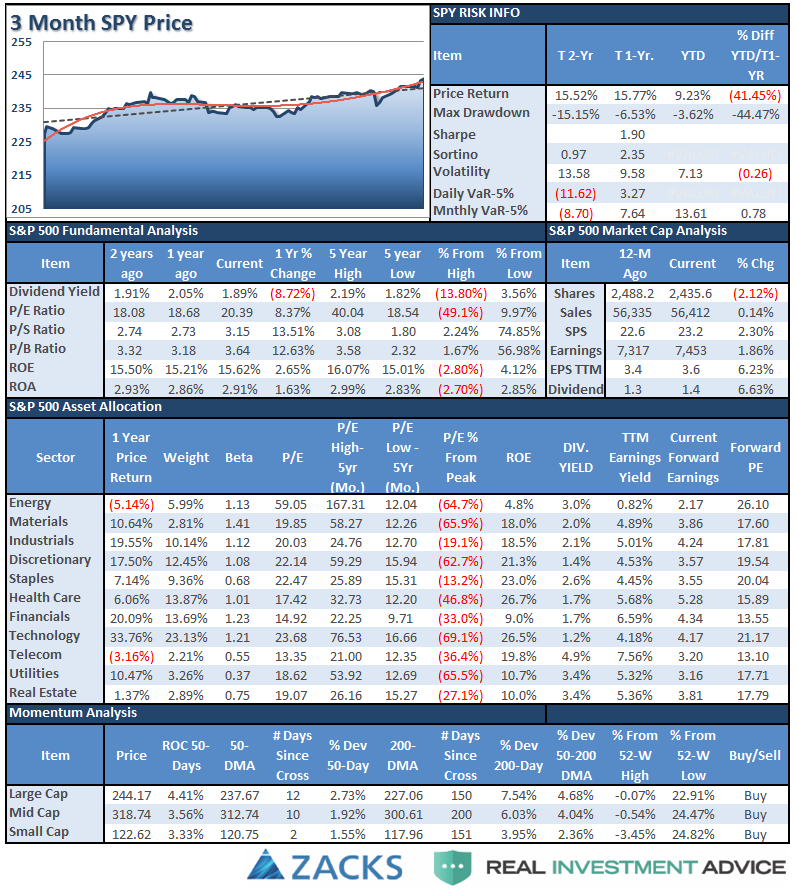

S&P 500 Tear Sheet

The “Tear Sheet” below is a “reference sheet” provide some historical context to markets, sectors, etc. and looking for deviations from historical extremes.

Please share this article – Go to very top of page, right hand side for social media buttons.

If you have any suggestions or additions you would like to see, send me an email.

Performance Analysis

Do you find this chart useful? If you have any suggestions or additions you would like to see, send me an email.

Sector Analysis

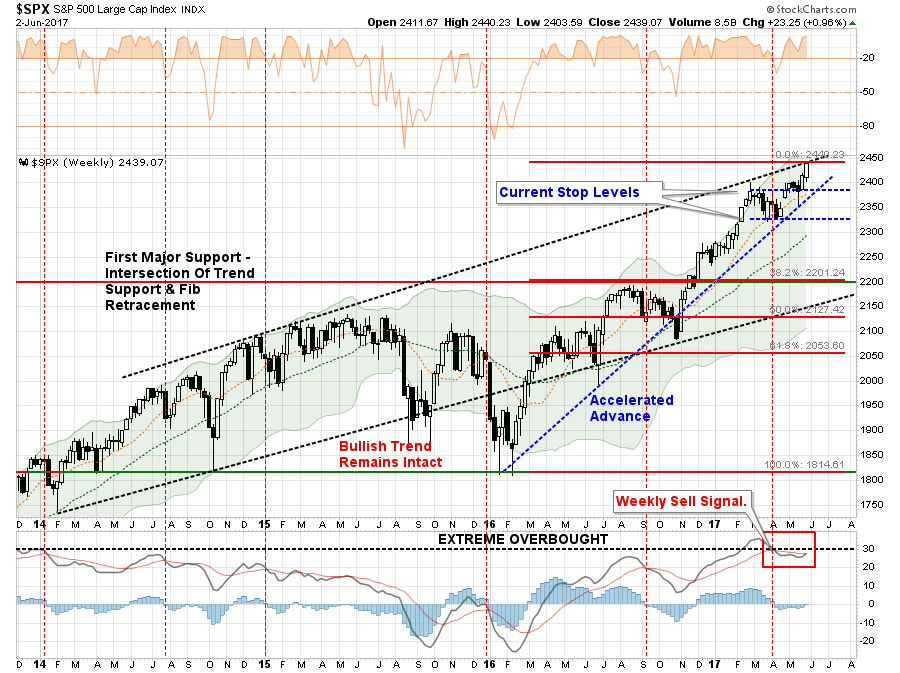

With the markets breaking out of the two-month consolidation and hitting new highs this past week, as stated above, it keeps our portfolios allocated on the long side for now.

Last week, we did add modestly to our broader-based “core” holdings to participate with the breakout. However, as shown below, stops have been moved up and remain very tight. A reversal and failure of the breakout would NOT be surprising given the underlying weakness in the internal breadth and participation measures.

Importantly, notice that despite the “breakout to new highs,” it did NOT reverse the weekly “sell” signal due to the “volumeless” lift. This keeps us cautious at the moment until that signal reverses which would require a further rally next week.

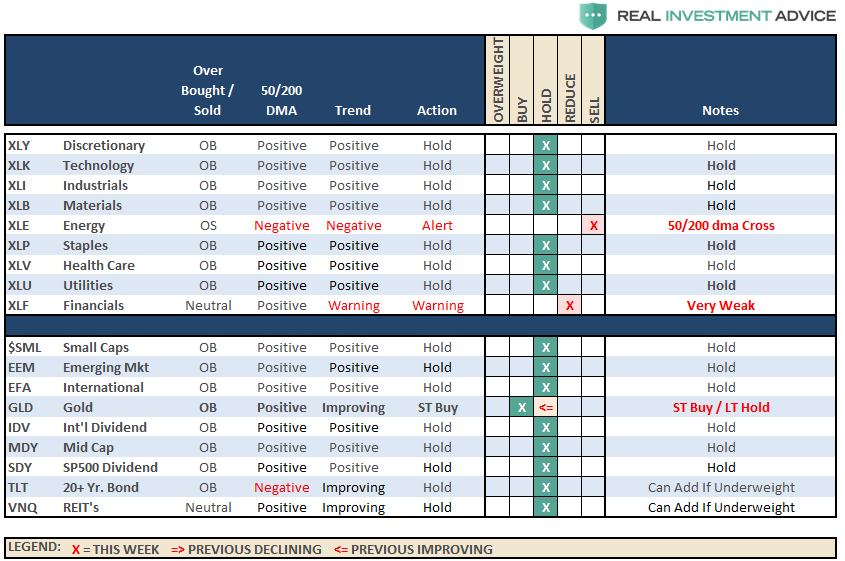

Sector Review

As discussed last week, this continues to be ONE CONFUSED MARKET as, once again, both DEFENSIVE and OFFENSIVE sectors rallied.

Discretionary, Technology, Staples, Utilities, Health Care, Materials, and Industrials all rose last week. However, it was the sharp surge, again, in Staples and Utilities that stood out last week as traditionally defensive sectors took charge in a “bullish breakout.”

Financials remained exceptionally weak and keeps us cautious on these sectors at the current time.

Energy – Despite the OPEC meeting extending production cuts and the rally in oil prices, the sector remains in a negative downtrend. With a major sector sell signal, and the cross of the 50-dma below the 200-dma, we remain out of the space for the time being.

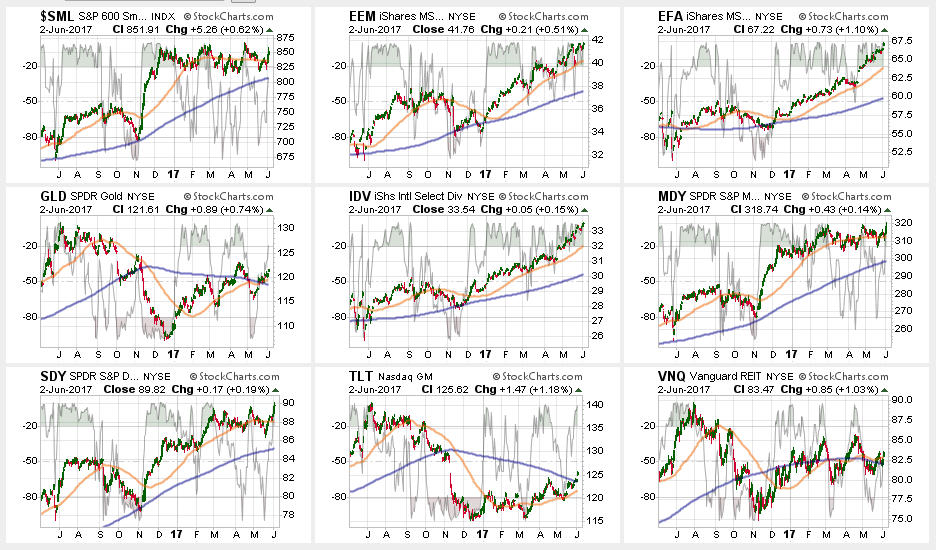

Small and Mid-Cap stocks both broke their respective 50-dma’s which had put these areas in on warning signs. However, last week, they regained their footing and pushed to new highs. However, on a relative basis, they are still underperforming the broad market which keeps the sectors on hold for now.

Emerging Markets and International Stocks continued their strength since their election lows as money continues to chase performance. There is a good bit of risk built into international stocks currently. We took profits a few weeks ago, but the recent extension suggests another round of rebalancing is likely wise. Take profits and rebalance sector weights but continue to hold these sectors but stop levels should be moved up to the 50-dma.

Gold – The rally in Gold last week once again puts a potential trading opportunity in place on a “short-term” basis. For longer-term investors, like us, we still need a breakout of the long-term downtrend at $1300/oz to take on portfolio weightings. With the 50-dma now above the 200-dma, a position can be added with a stop at the 200-dma.

S&P Dividend Stocks regained key support levels currently after briefly breaking below their 50-dma. Hold current positions but maintain stops at the recent lows.

Bonds and REIT’s continued their advances this week breaking solidly above resistance. With the 50-dma’s moving upward, these sectors can be added to selectively if underweight. However, this feeds back into the conundrum of the overall market, with both offensive and defensive sectors rallying, someone is going to be wrong. We will be watching these sectors for clues as to what happens next.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

The bullish trend remains positive, which keeps us allocated on the long side of the market for now, but the weekly “sell signal” alert is not being dismissed.

As noted in last week’s missive:

“With the breakout we did increase our exposures a little bit, but I would like to see some continued strength into next week for confirmation before adding additional risk. This is particularly the case as we move into the seasonally weaker months of the year. We are maintaining stops at recent support levels on all sectors and at 2325 on the S&P 500.”

Given the move higher on Thursday and Friday, we will review portfolios on Monday for potential additions of “risk” exposure where needed. However, be mindful, that we do so with the very strict “sell” discipline in place in the event that something goes wrong.