Written by Lance Roberts, Clarity Financial

Review and Update

Warning: I had a small surgery on Thursday, so I am currently “WUI,” – or Writing Under The Influence. So, hopefully, the following will make some sense.

Please share this article – Go to very top of page, right hand side for social media buttons.

In last week’s missive, I discussed the breakout of the market.

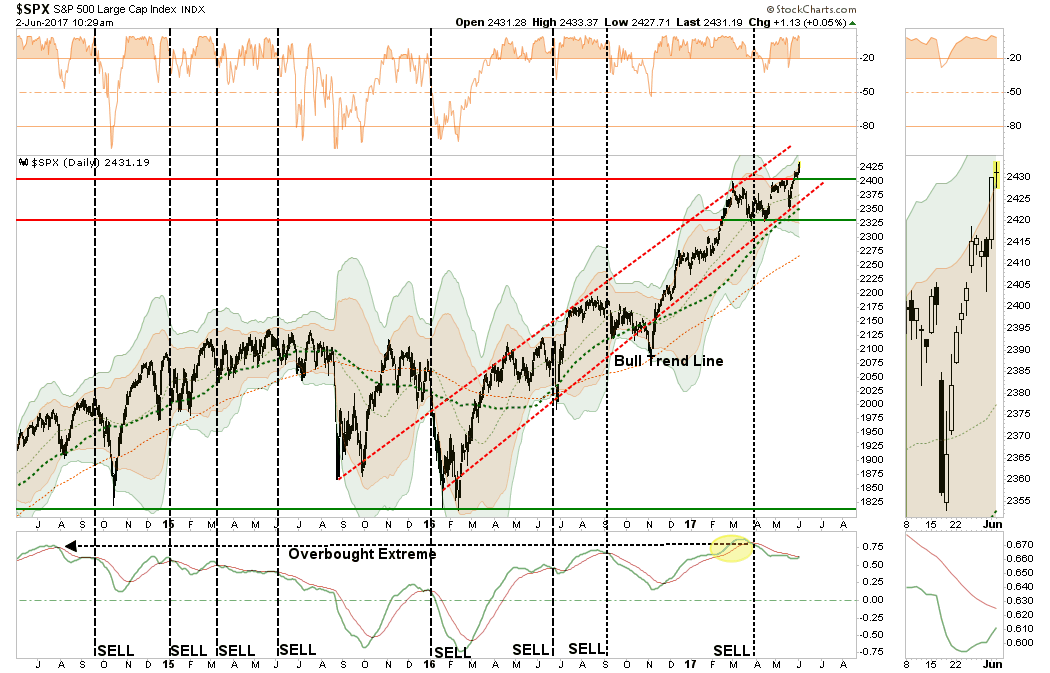

“The breakout does keep our allocation model nearly fully allocated. We are holding onto a little larger than normal cash pile just to hedge some volatility risk during the summer months. Also, stops have now moved up to the bottom of the bullish trendline as shown in the chart below which coincides with the 100-day moving average which has been a running support line.”

The “sell signal” currently remains in place from very high levels, and with a push into 3-standard deviations above the 50-dma currently, we remain cautious for now.

However, there is no denying the “bullish bias” currently remains in the market, and the sharp push higher reconfirms the underlying trend. Because of that “bias,” we remain allocated towards risk in our portfolios.

The biggest problem I have currently is simply that bonds are NOT buying the rally. As I discussed last week, and as we saw on Friday, bonds continue their “bullish bias” and broke through key support levels suggesting lower rates to come.

With interest rates still overbought, and on an important “sell signal,” the downside break from the recent consolidation process will likely prove problematic for stocks going forward as the flight from risk to safety continues.

But, as we discussed a couple of week’s ago, this is a very “confused market” with both offense and defensive sectors taking the lead. As shown in the “spaghetti chart” below, there are currently 8-sectors leading the S&P 500. More importantly, the “riskier” small and mid-cap markets continue to remain weak which is certainly not the backdrop to support a strongly running “bull.”

This really is a more bizarre clustering of markets and sectors that I have witnessed in quite some time. However, for now, the rotation between sectors remains tight and it is the #FANMAG stocks that continue to elevate markets because of their sheer size. ($FB, $AAPL, $NFLX, $MSFT, $AMZN, $GOOG)

The question that continues to linger over the markets is just how stable is the advance? The answer to that question is unclear, but it is quite likely the spat of earnings growth seen over the last couple of quarters will soon end as year-over-year comparisons get decidedly tougher.

Considering that earnings estimates are generally overstated by roughly 30%, the actual net decline in earnings growth will likely be far sharper than currently anticipated. More importantly, since the bulk of the increase in earnings estimates were based upon tax cuts/reforms, when it becomes apparent those legislative policies are not forthcoming, earnings estimates will be ratcheted sharply lower. With the market trading well ahead of earnings growth currently, the risk of disappointment is extremely high.

Lastly, given that much of the recent rebound in earnings came from the sharp rise in oil prices, with those prices once again on the decline, it is quite likely forward earnings are overly optimistic currently.

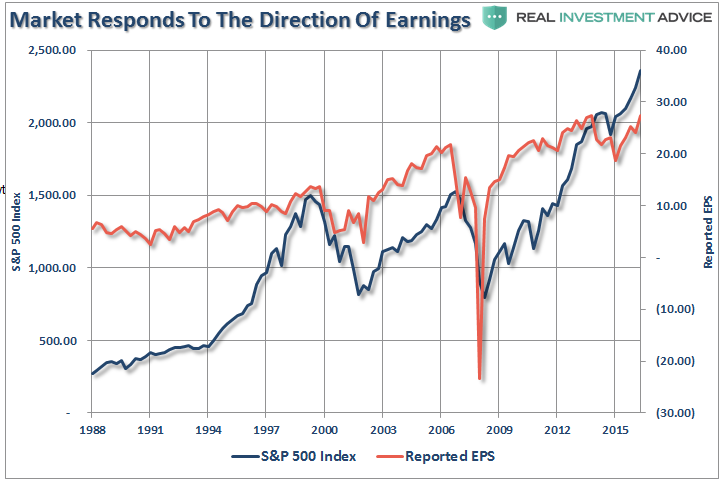

Importantly, and something I am going to address more on Monday, corporate profits after tax are not exhibiting the same “sharp rise” as earnings. In fact, since the lows following the financial crisis, the S&P 500 has grown by 266% versus profit growth of just 98%.

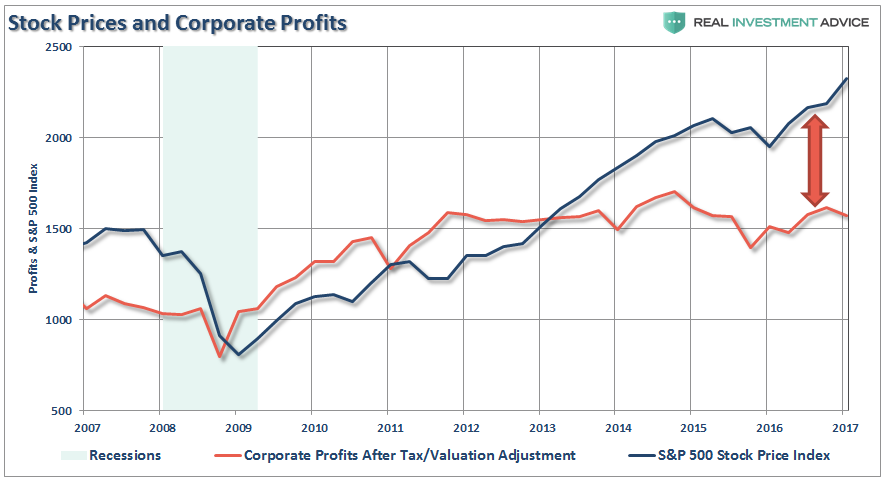

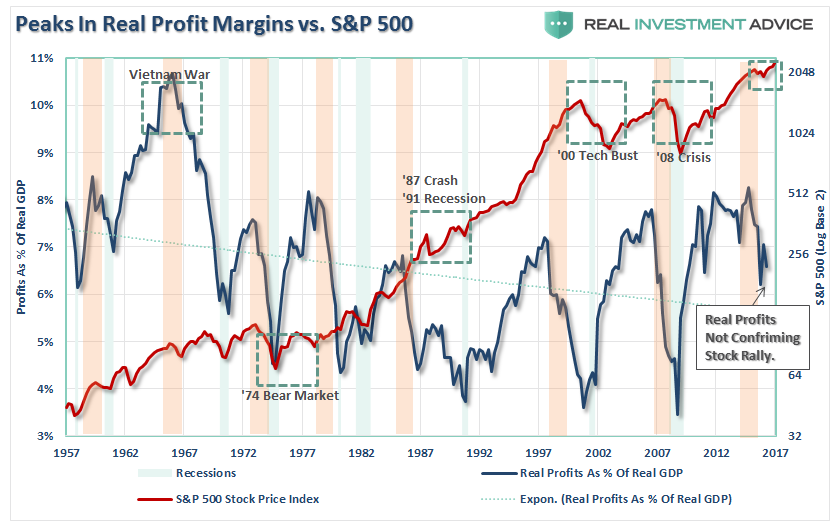

With corporate profits still at the same level as they were in 2011, there is little argument the market has gotten a bit ahead of itself. Since corporate profits are a reflection of what is happening in the economy, we can also look at inflation adjusted corporate profits as a percentage of Real GNP.

The light shaded green bars represent recessions while the light orange bars show peaks in corporate profits. Sure, this time could be different, but it just usually isn’t. The detachment of the stock market from underlying profitability suggests the reward for investors is grossly outweighed by the risk.

However, as has always been the case in the past, the markets can “remain irrational longer than logic would predict.”

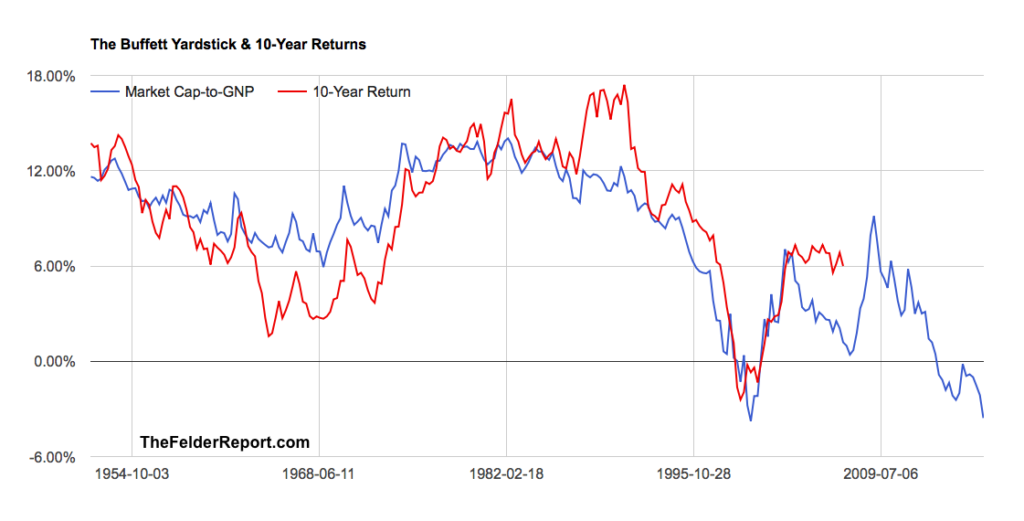

As my friend and colleague, Jesse Felder, recently penned:

“But it’s even more troublesome than that because of the second attribute related to the “margin of safety” concept. Not only are we taking more risk by eliminating our margin for error we are also reducing our potential rate of return. In fact, the higher the price we pay the greater the risk we take AND the lower return we can achieve.

Considering the price-to-sales ratio for the median stock in the S&P 500 is higher than ever before and to a significant degree, you might say investors are taking the greatest amount of risk for the least amount of potential return in history. In other words, if there was ever an example of ‘reward-free risk’ this is it.”

Currently, there has been NO CHANGE in the headlong bullish rush into the ethersphere. Therefore, we remain long, and even added some exposure following the breakout last week, in our portfolio allocations.

I agree with Jesse and remain convinced the longer-term reward is far outweighed by the risk. However, while we are maintaining our allocations to risk currently, we do so with the understanding everything could change very rapidly.

Caution is advised.

See you next week.