Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side for social media buttons.

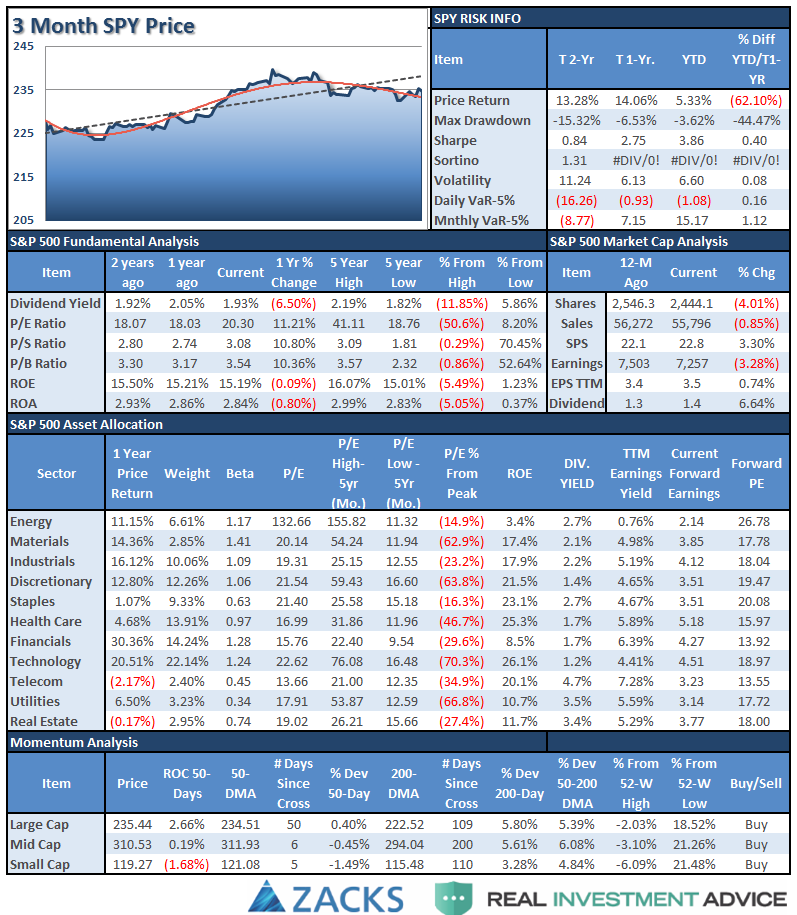

S&P 500 Tear Sheet

The “Tear Sheet” below is a “reference sheet” provide some historical context to markets, sectors, etc. and looking for deviations from historical extremes.

If you have any suggestions or additions you would like to see, send me an email.

Sector Analysis

The slow-motion correction that began back in March continued again this past week, with the market rallying, as expected last week, but failing at the 50-dma as resistance builds. This also triggered a weekly sell-signal as discussed above, and potentially a secondary weekly “sell” signal as well. The markets must significantly gain traction next week if a deeper correction is to be avoided for now.

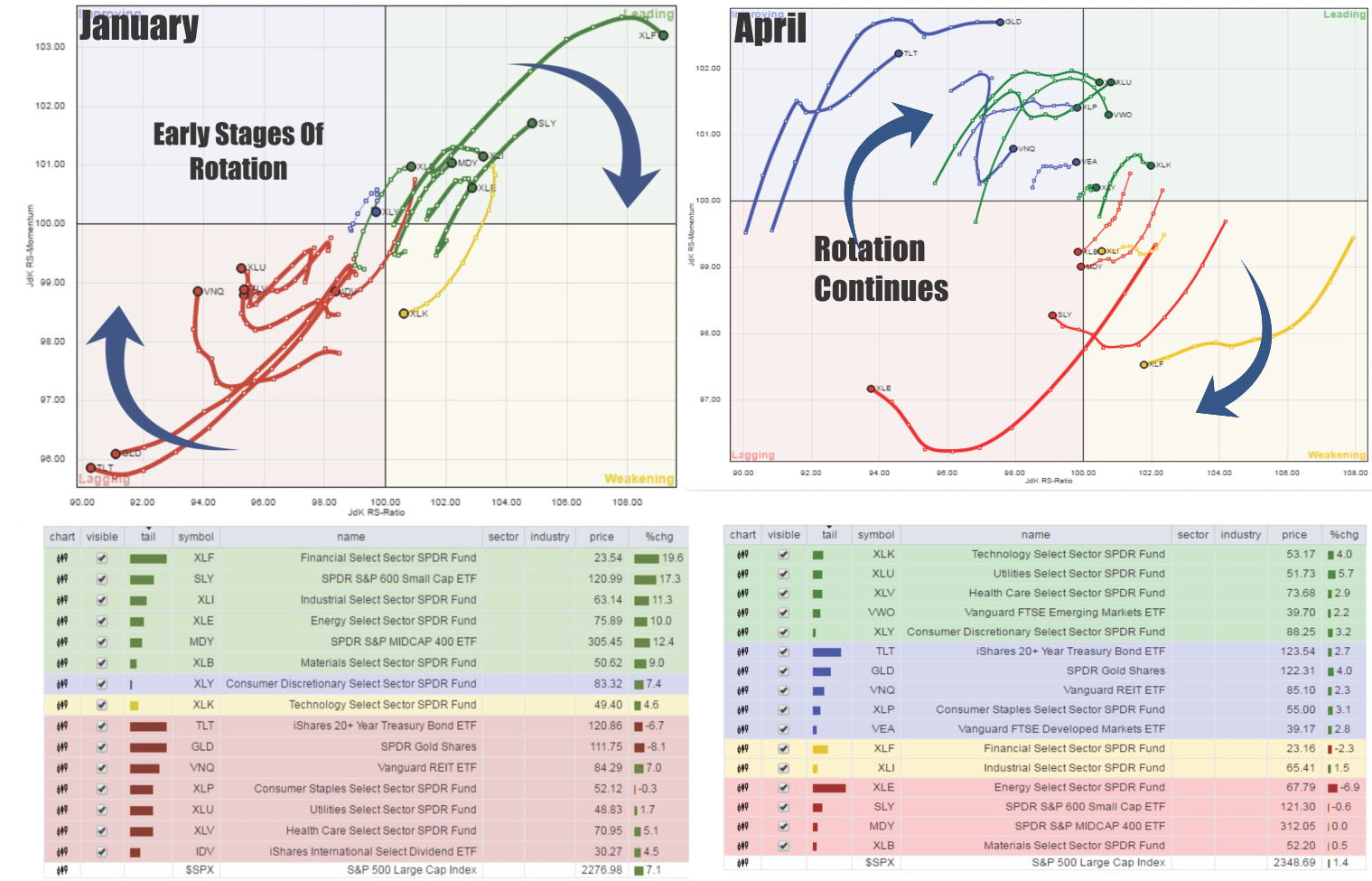

In January of this year, I discussed how the various sectors of the market “rotate” over time. To wit:

“The video below shows the historical “rotation” of sectors over the last 3-years. As you will notice sectors have consistently “swarmed” in a clockwise rotation going from strongly outperforming the S&P 500 index to strongly underperforming. If you watch to the end of the video you will see the post-presidential election anomaly form.”

I have notated the changes on the Sector Rotation model below. In January, the set up for a rotation, following the November election was apparent. It was at that time that we began to overweight bonds, utilities, and REIT’s in portfolios DESPITE the calls from the media that rates had “nowhere to go but up because of the Fed.”

Four months later, we have now lightened up on that trade a bit, but still remain primarily long the improving and leading sectors.

Remain cautious currently as the “Trump Trade” has continued to weaken over the last week.

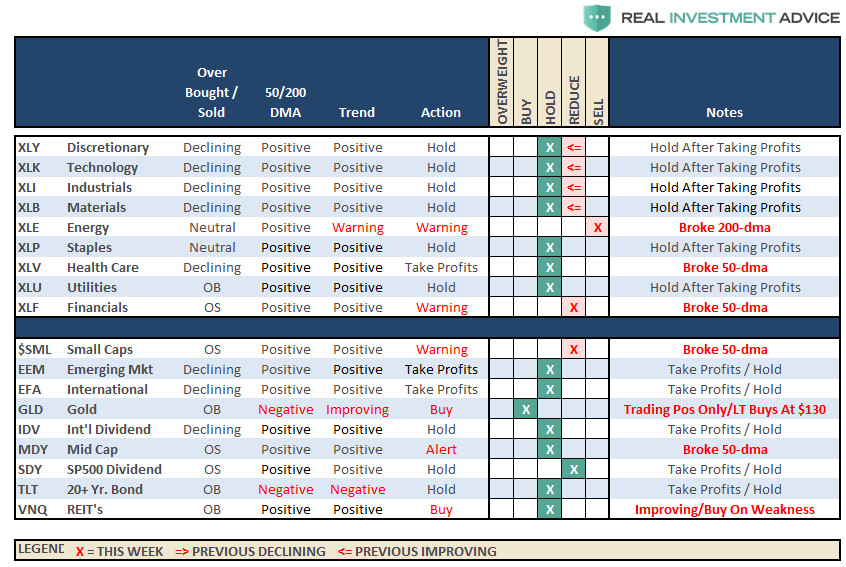

Despite the ongoing struggles with the “retail sector,” Discretionary stocks bounced off their 50-dma last week to maintain its bullish bias. However, that surge also pushed the sector back into overbought status.

Technology, Industrials, and Materials sectors continue to struggle with their respective 50-day moving averages. While still trending positively, relative performance has weakened substantially for now.

Energy continues to struggle after breaking its 50-dma and broke its 200-dma two weeks. While energy had a bit of a bounce last week, and tested resistance at the 50-dma, the bounce failed and the trend continues to materially weaken. Energy is very close to a major sector sell signal. Remain heavily underweight energy for the time being.

Healthcare and Financials have broken their 50-dma. Underweight these sectors for now.

Bonds, Utilities, and Staples all continue to be the clear winners, which we were discussing back in January, as the Trump Trade was going to reverse. Those hedges have continued to perform well despite the weakness in other areas of the market. We did take profits last week in some of our holdings.

Small and Mid-Cap stocks continued to weaken in terms of relative performance and have broken their respective 50-dma’s. The deterioration of relative strength continues to suggest caution.

Emerging Markets, International, and Dividend Yielding Stocks are also showing weakness but remain in a bullish trend currently. Some profit taking and rebalancing is advised.

Bonds and REIT’s currently overbought and some profit taking is advised. If the broader markets can rally over the next week or two, simply due to a reflexive oversold condition, look for these sectors to pull back to provide a better entry point.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

After hedging our long-equity positions 18-weeks ago with deeply out-of-favor sectors of the market (Bonds, REIT’s, Staples, Utilities, Health Care and Staples) we did rebalance some of our long-term CORE equity holdings back to original portfolio weightings harvesting a bit of liquidity.

While the bullish trend is still positive, which keeps us allocated on the long-side of the market, the weekly “sell signal” alert is not being dismissed. As I penned here last week:

“Any rally next week that ‘fails’ to put the market back on more solid footing will be used to reduce risk in portfolios to some degree and rebalance back to target weightings.”

We did raise some cash last week out of overbought sectors, and are waiting to see if the markets can regain some strenth this coming week as noted above.

We are still maintaining hedges until the current corrective action completes. Furthermore, we are currently maintaining ‘new money’ in short-term cash positions and only selectively stepping into core long-term holdings with tight stop-loss levels.”

We continue to maintain very tight trailing stops as the mid to longer-term dynamics of the market continue to remain very unfavorable.