Written by Lance Roberts, Clarity Financial

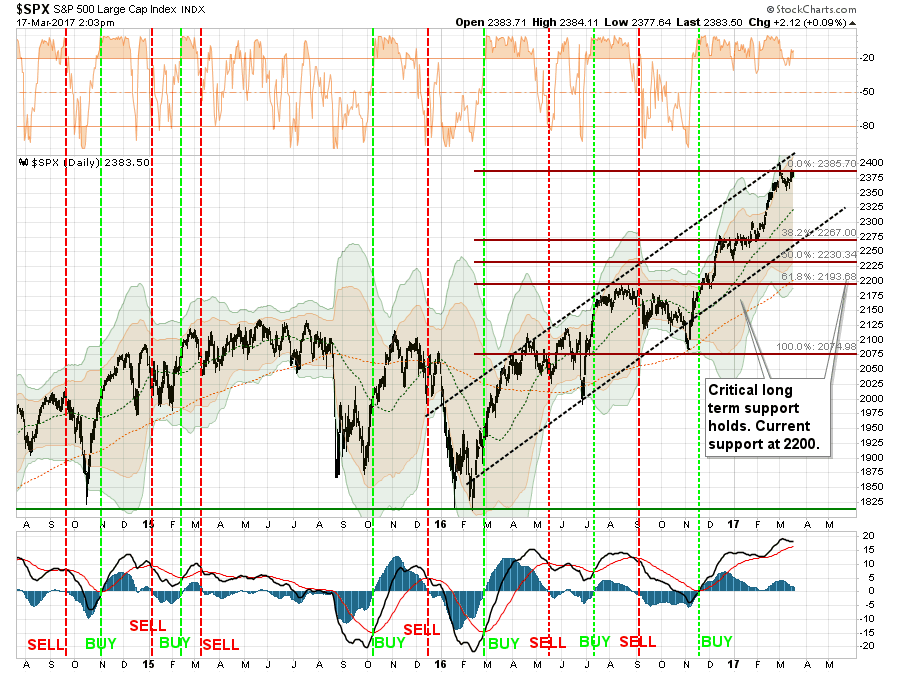

This past Wednesday, on The Real Investment Hour, I spoke with Greg Morris about the technical backdrop of the market. During that interview, he discussed that from a technical perspective the bullish trend of the market is still in place, and despite fundamental underpinnings being stretched, investors should remain allocated to the market.

This is shown in the chart below.

For now, portfolios remain allocated to the market currently. However, as I stated two weeks ago, we did lift profits and rebalance current holdings. Furthermore, we are not adding any “new” positions currently until some of the extreme overbought conditions are resolved.

This is what the “technicals” dictate, at least for now.

As noted in the chart above, the market is very close to a short-term “sell signal,” lower part of the chart, from a very high level. Sell signals instigated from high levels tend to lead to more substantive corrective actions over the short-term. I have denoted the potential Fibonacci retracement levels which suggest a pullback levels of 2267, 2230, and 2193. To put this into “percent terms,” such corrections would equate to a decline of -4.7%, -6.2% or -7.8% from Friday’s close.

To garner a 10% decline, stocks would currently have to fall 237.8 points on the S&P 500 to 2140.20. Given there is little technical support at that level, the market would likely seek the next most viable support levels at the pre-election lows of 2075 or a decline of -12.7%. Such a decline, of course, would not only wipe out the entirety of the “Trump Bump,” but would also “feel” much worse than it actually is given the exceedingly long period of an extremely low volatility environment.

Speaking of low volatility, the market has now gone 108-trading days without a drop of 1% for both the Dow and the S&P 500. This is the longest stretch since September of 1993 for the Dow and December of 1995 for the S&P 500.

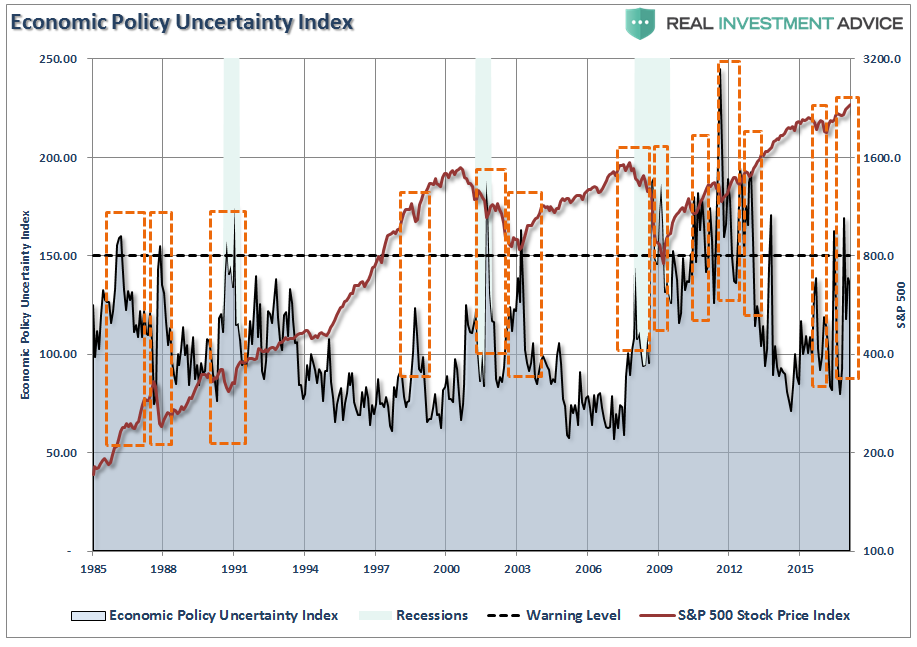

This is a pretty impressive feat given the rise in policy uncertainty since the election, geopolitical tensions on the rise, and economic data remaining weak.

In other words, there is a whole lot more downside risk than upside potential in the current environment.

This is particularly the case following the FOMC’s decision on Wednesday to hike rates further.