Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

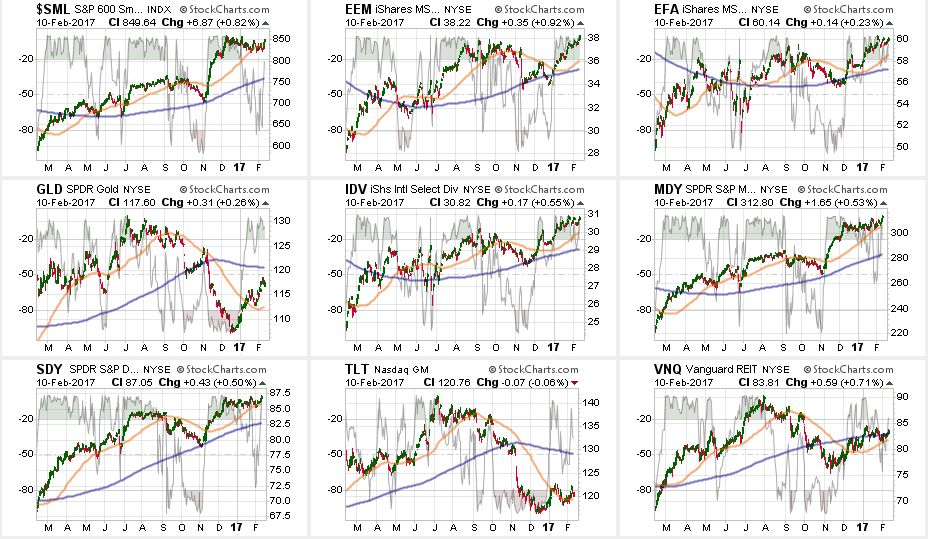

S&P 500 Tear Sheet

The “Tear Sheet” below is a “reference sheet” provide some historical context to markets, sectors, etc. and looking for deviations from historical extremes.

If you have any suggestions or additions you would like to see, send me an email.

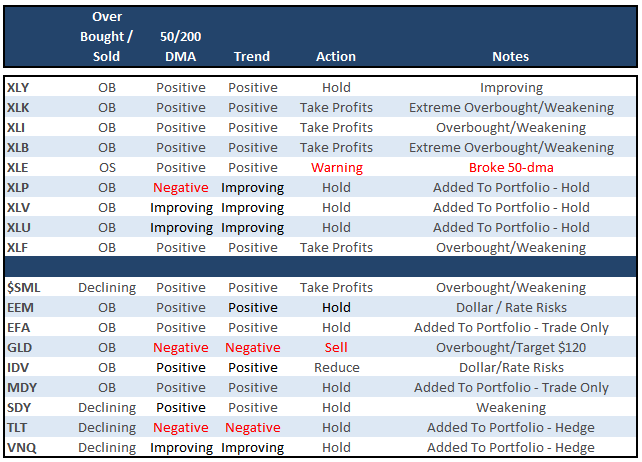

Sector Analysis

The Rotation Becoming More Pronounced

Over the last couple of months, I have been discussing the coming rotation of the “risk on” versus the “risk off” sectors in the market. As I noted (with a video) at the beginning of the year, these rotations usually are early indicators of a “risk off” transition and provide opportunities for investors.

As you can see, that rotation has continued to accelerate over the last couple of weeks.

Portfolio Note: I have made two adjustments to the model below so it will align more closely with our actual portfolio allocations. I have swapped IDV for VEA and added VWO.

Due to the weight of our portfolio hedges in portfolios currently, we are using a position in IWM as a proxy for MDY and SLY.

Portfolios reside at our maximum portfolio equity weightings including hedges.

This rotation is still likely early in its movement. As noted previously, when the “Trump exuberance trade” reached its peak post-election, the rotation trade became very obvious. As noted at the beginning of this missive, from a historical viewpoint corrections in the month of February tend to amass towards the end of the month.

In other words, don’t let this week’s rally fool you. It is historically very well aligned with normal early February advances. The “risk off” trade is likely telling us something more important.

Last week, in response to Matt Drudge’s criticism of the GOP for not pushing tax reform through more quickly, President Trump responded by saying during an interview:

“Lowering the overall tax burden on American business is big league, that’s coming along very well. We’re way ahead of schedule, I believe. And we’re going to be announcing something – I would say over the next two or three weeks – that will be phenomenal.”

From a position view, the commitment of tax cuts sent the “Trump Trade” sensitive sectors higher.

Technology, Discretionary, Industrials, Staples, Utilities, Health Care and Financials pushed higher, but even despite a rise in oil prices, Energy weakened after breaking its 50-dma last week. Basic Materials lagged but held its ground.

Notably, watch Utilities as the 50-dma is heading back up suggesting a cross of the 50-200 dma is likely. The same goes for Staples and Healthcare.

From the broader index positioning:

Small Caps, REIT’s, Mid Caps, Dividend Stocks and Bonds continue to flirt with their respective 50-dmas. Emerging and International markets got a lift from the weakening dollar which prompted an increase in International weightings in portfolios last week from a trading perspective.

Gold retested its 50-dma and bounced higher which is a technical improvement but remains locked in a long-term downtrend.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

Nine weeks ago, as suggested, we hedged our long-equity positions with deeply out-of-favor sectors of the market (Bonds, REIT’s, Staples, Utilities, Health Care and Staples) which have continued to perform well in reducing overall portfolio volatility risk.

As noted last week, we added two new positions from a “Trading” perspective only: IWM – Russell 2000 and VEA – International

The short-term bullish trend and technical setup required an increase in equity risk in portfolios. However, all positions maintain very tight trailing stops as the mid to longer-term dynamics of the market continue to remain very unfavorable.

As I have been warning over the last couple of months, the stronger dollar and the rise in rates should not be dismissed.

Everything is currently pointing to this being a very late stage advance, so profit taking, hedging, and rebalancing remains strongly advised.