Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

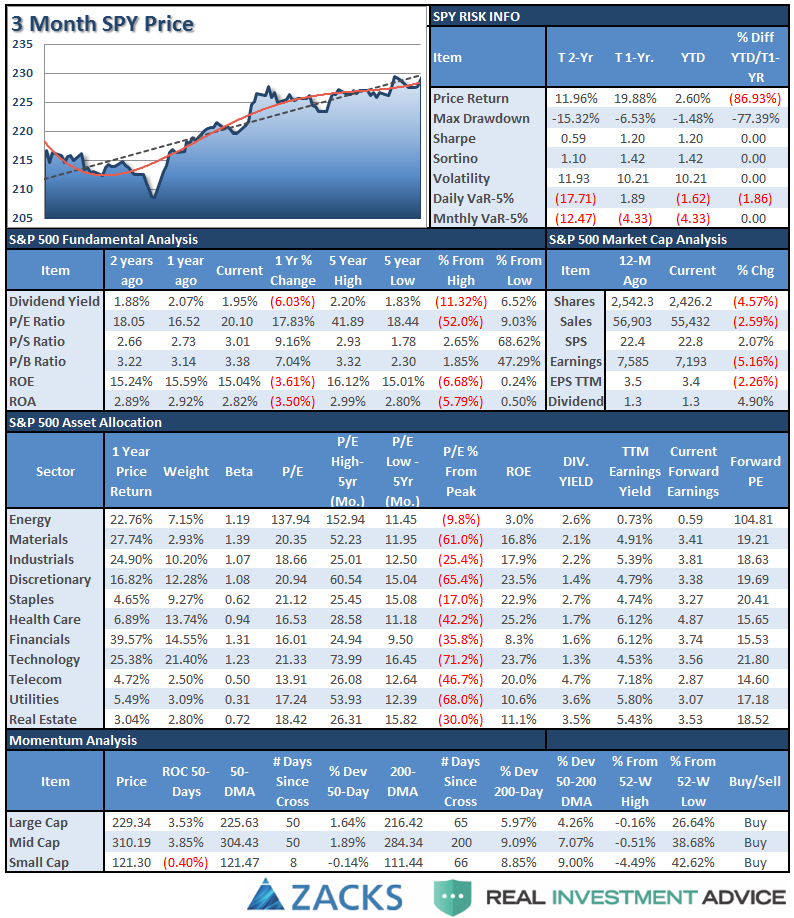

S&P 500 Tear Sheet

The “Tear Sheet” below is a “reference sheet” provide some historical context to markets, sectors, etc. and looking for deviations from historical extremes.

If you have any suggestions or additions you would like to see, send me an email.

Sector Analysis

Comments

With “Week 2″ of the new administration behind us, and a flurry of “executive orders” being issued, the markets were saved on Friday by an “order” to effectively repeal the “fiduciary rule” of Dodd-Frank effectively putting the “Wolf Of WallStreet” back in the proverbial “Investor Hen House.”

As I tweeted on Friday:

(Please “Retweet” If you agree.)

This order sent financial stocks rocketing higher on Friday which pulled the markets higher into the close and offsetting the drag from AMZN following their earnings announcement.

For the second consecutive week, the S&P Index finished higher with a 0.12% or 2.73 point gain. However, the reversal from early trading low was a total reversal of 30 points for the week.

The Rotation Continues

Over the last couple of months, I have been discussing the coming rotation of the “risk on” versus the “risk off” sectors in the market. As I noted (with a video) at the beginning of the year, these rotations usually are early indicators of a “risk off” transition and provide opportunities for investors.

As you can see, that rotation has continued to accelerate over the last couple of weeks.

This rotation is still likely early in its movement. As noted above, while RISK bullishness has reached extremes, SAFETY has been completely disregarded. Reversions tend to be rapid.

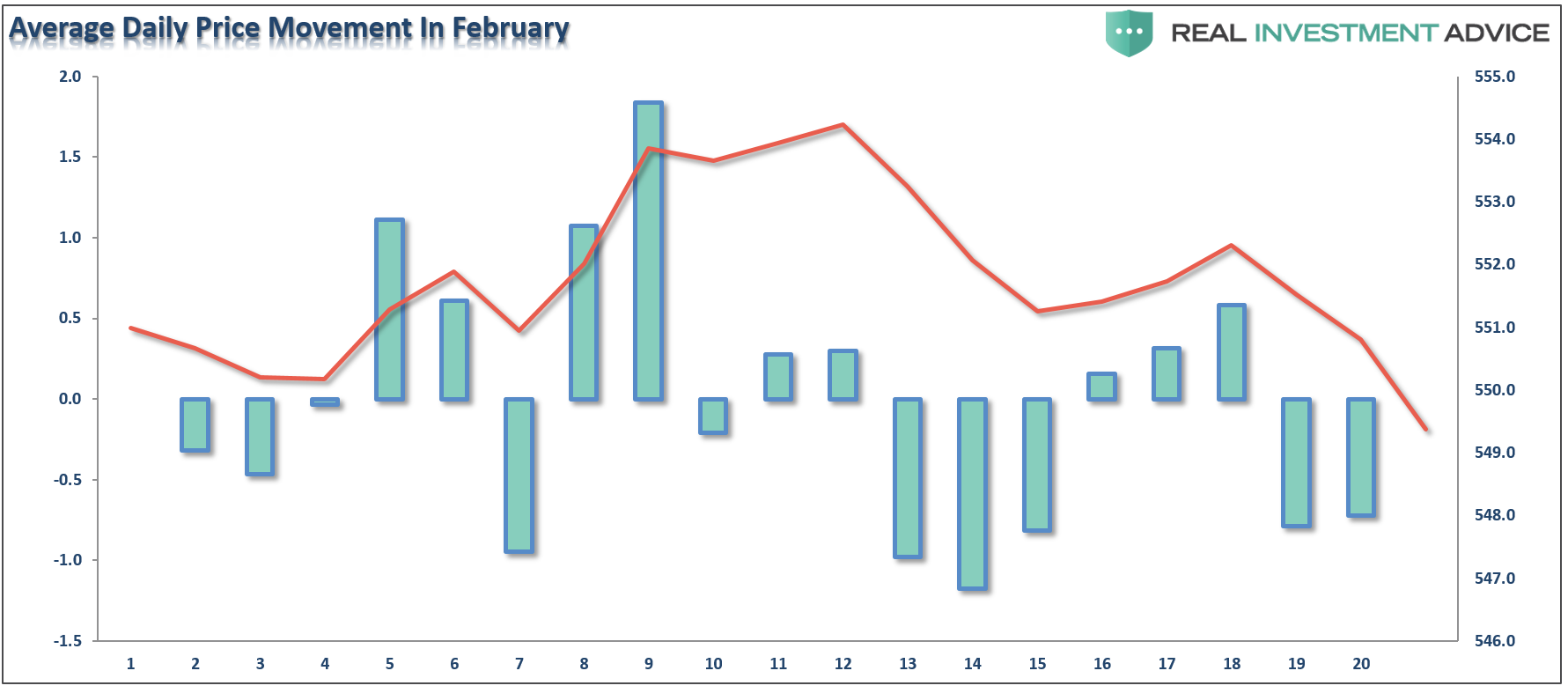

More importantly, from a historical viewpoint, and as I discussed this week, corrections in the month of February tend to amass towards the end of the month.

“A look at daily price movements during the month, on average, reveal the 4th trading day of February through the 12th day provide the best opportunity to rebalance portfolio allocations and reduce overall portfolio risk.”

In other words, don’t let this week’s rally fool you. It is historically very well aligned with normal early February advances. The “risk off” trade is likely telling us something important.

From a position view, Technology pushed higher last week along with Staples, Health Care, Utilities, Financials, and Materials. Discretionary and Industrials lagged while Energy broke below its 50-dma.

From the broader index positioning:

Small Caps, REIT’s, Mid Caps, Dividend Stocks and Bonds continue to flirt with their respective 50-dmas. Emerging and International markets got a lift from the weakening dollar which prompted an increase in International weightings in portfolios last week from a trading perspective.

Gold retested its 50-dma and bounced higher which is a technical improvement but remains locked in a long-term downtrend.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

Eight weeks ago, as suggested, we hedged our long-equity positions with deeply out-of-favor sectors of the market (Bonds, REIT’s, Staples, Utilities) which have continued to perform well in reducing overall portfolio volatility risk.

Early this past week we added two new positions from a “Trading” perspective only: IWM – Russell 2000 and VEA – International

The short-term bullish trend and technical setup required an increase in equity risk in portfolios. However, all positions maintain very tight trailing stops as the mid to longer-term dynamics of the market continue to remain very unfavorable.

As I have been warning over the last couple of months, the stronger dollar and the rise in rates should not be dismissed.

Everything is currently pointing to this being a very late stage advance, so profit taking, hedging, and rebalancing remains strongly advised.