Written by Lance Roberts, Clarity Financial

Let’s take a quick look at the 9-major sectors of the S&P 500 to determine the overall strength of the bullish bias.

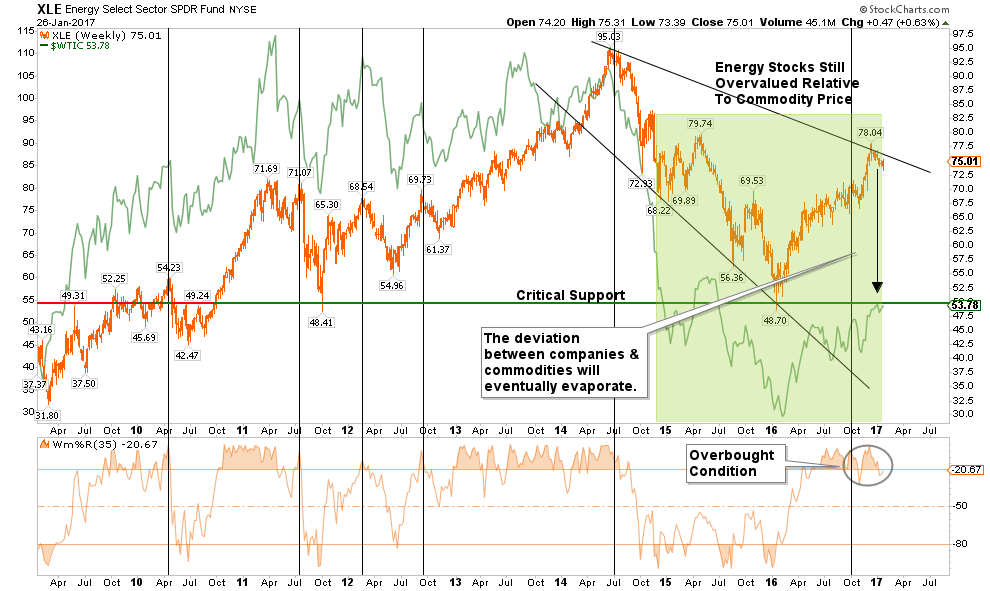

ENERGY

The OPEC oil cut will likely fail in the next two months particularly as the ramp up in protection continues in the Permian Basin. The Saudi’s are only going to give up so much “market share” before returning back to full production.

Like the extreme “short positioning” on the VIX and Treasuries, speculators are extremely net long in oil contracts. There is an extremely high probability the supply increase that is currently happening will not only cap oil price temporarily but will likely push oil prices lower in the months ahead.

Energy companies remain extremely overvalued and disconnected relative to the underlying commodity price. When the next economic recession hits, energy-related equities will likely once again recouple with its base commodity.

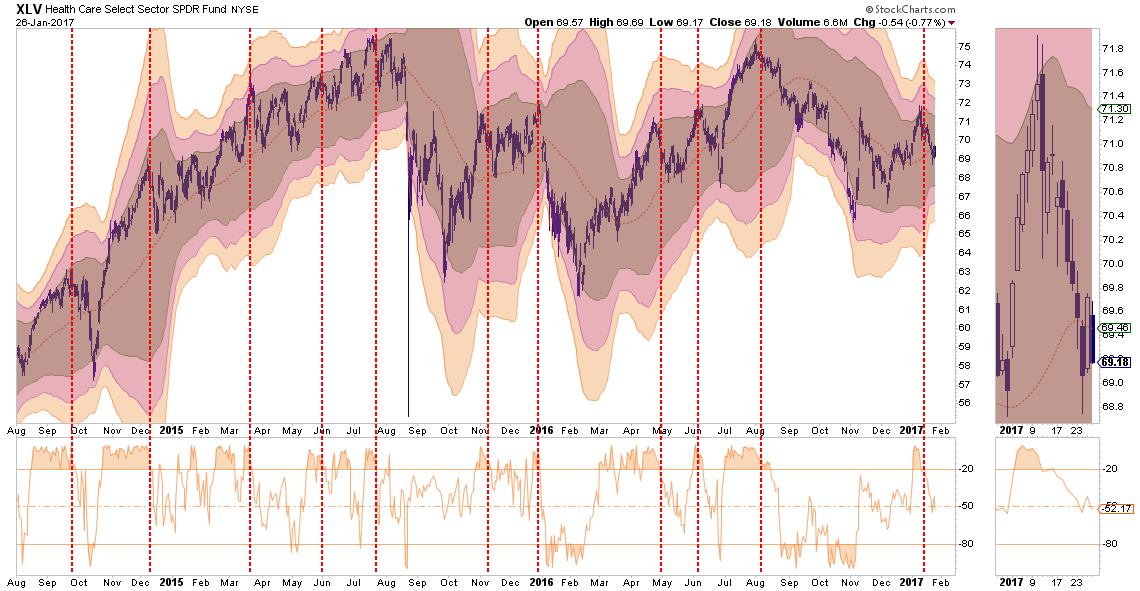

HEALTH CARE

The healthcare sector has been a laggard as of late and continues to struggle with the unknown of what is going to happen with the health care system overhaul under President Trump. With the sector very currently correcting from an overbought condition, there is not a reasonable risk/reward setup currently in the sector.

Current holdings should be reduced to under-weight for now as there is not a good stop-loss setup currently available.

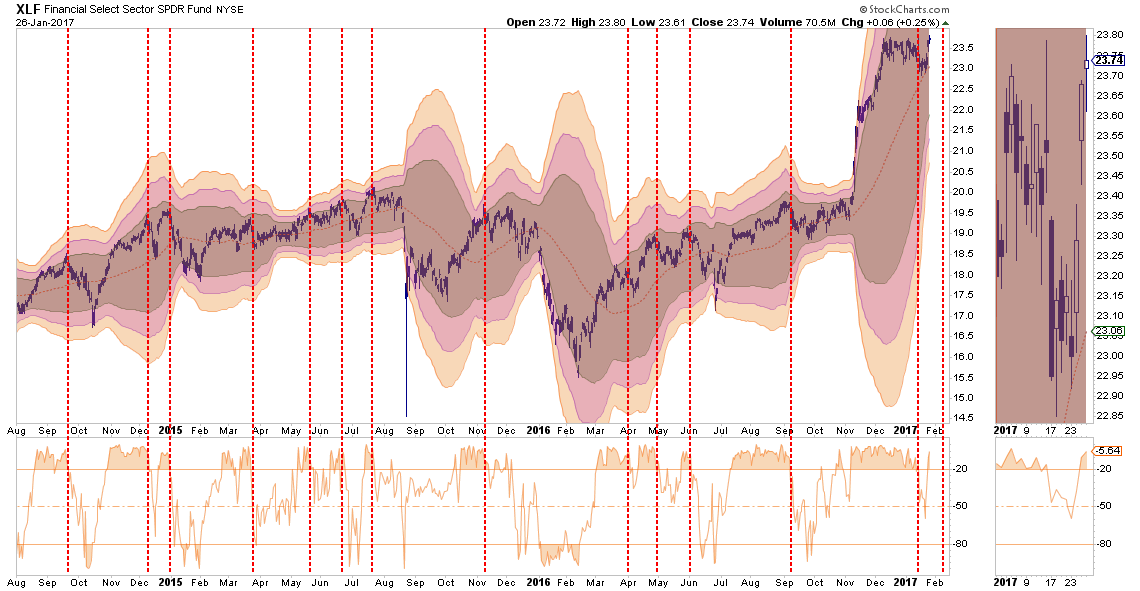

FINANCIALS

Financials continue to be the leader with respect to overall relative performance. There is a tremendous amount of exuberance being built into Financials which makes this sector ideal for reducing back to portfolio-weight, taking profits and setting a stop-loss at $22.50

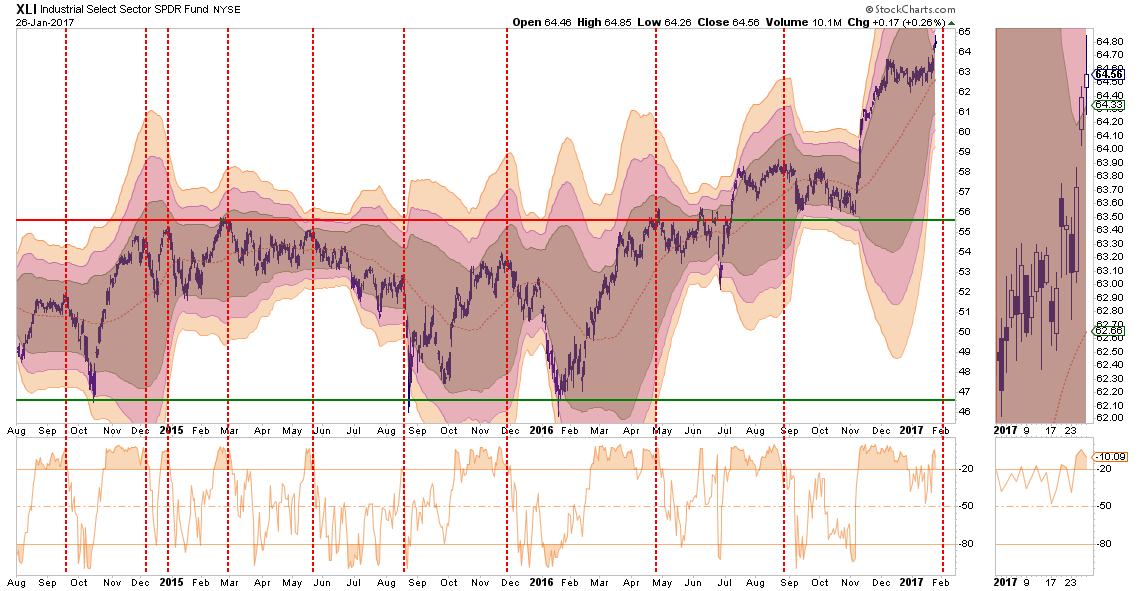

INDUSTRIALS

Industrial stocks, because of the dividend yield, have been a big beneficiary of the “yield chase” previously. Now, like Materials, they are the subject of the “Make America Great Again” infrastructure trade. However, this sector is directly affected by the broader economic cycle which continues to remain weak.

While the sector broke out to new highs, there is not a good risk/reward setup as there is a long way to a good stop level at $50. I would reduce holdings back to portfolio weight for now and take in some of the gains.

MATERIALS

As with Industrials, the same message holds for Basic Materials, which are also a beneficiary of the dividend / “Make America Great Again” chase. This sector should also be reduced back to portfolio weight for now with stops set at the lower support lines $49.50.

UTILITIES

Utilities have been picking up performance over the last couple of weeks as money begins to rotate back into “safety” plays of bonds and interest rate sensitive sectors. Stops should be set on current holdings at the lower support levels $47.50 for now and a break above resistance should set the sector up for a further advance.

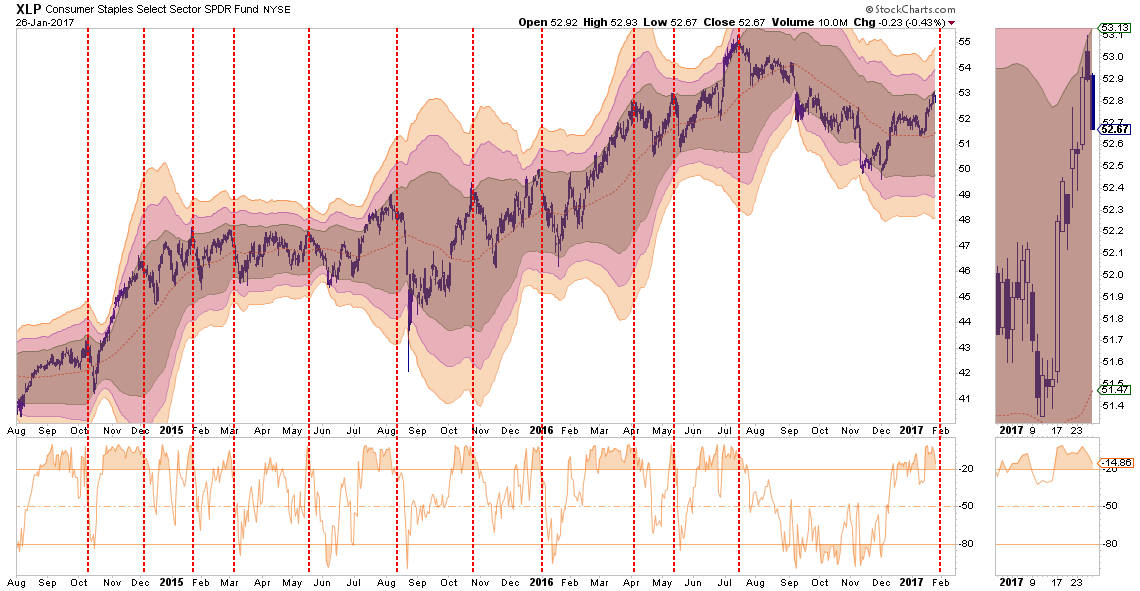

STAPLES

Staples, have recovered as of late and are now back to extreme overbought, along with every other sector of the market. Set stops at $52 for now and look for a correction that does not break support to increase exposure to the sector.

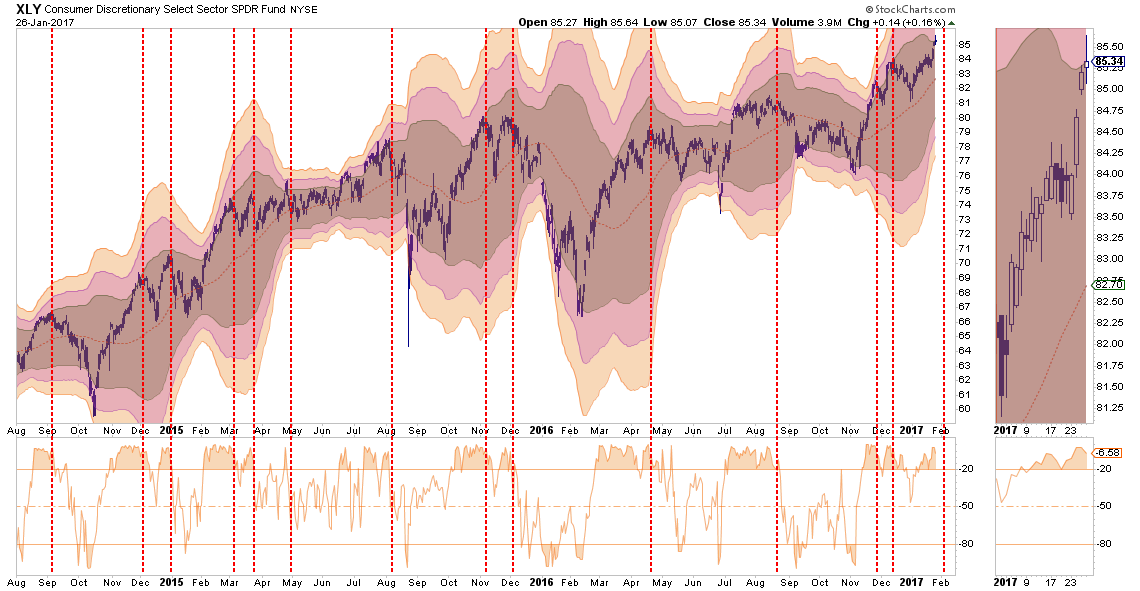

DISCRETIONARY

Discretionary has been running up in hopes the pick-up in consumer confidence will translate into more sales. There is little evidence of that occurring. Portfolio weightings should be trimmed back to underweight at the current time with stops set at $81. With many signs the consumer is weakening, caution is advised and stops should be closely monitored and honored.

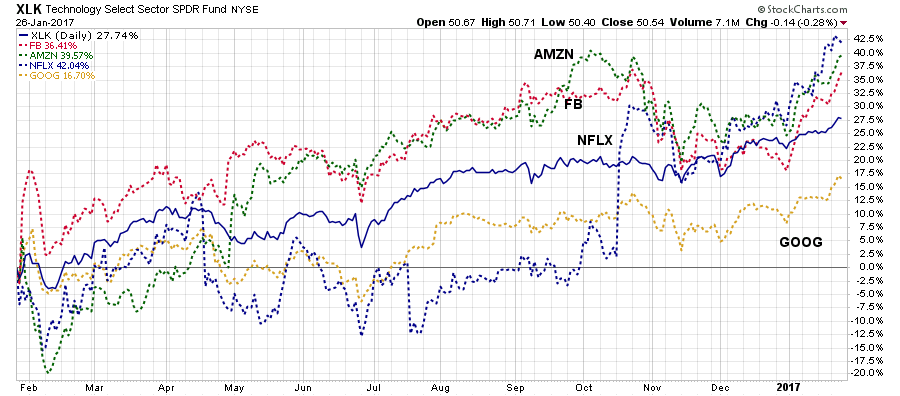

TECHNOLOGY

The Technology sector has been the “obfuscatory” sector over the past couple of months. Due to the large weightings of Apple, Google, Facebook, and Amazon, the sector kept the S&P index from turning in a worse performance than should have been expected prior to the election and are now elevating it post election.

The so-called FANG stocks (FB, AMZN, NFLX, GOOG) continue to push higher, and due to their large weightings in the index, push the index up as well.

The sector is extremely overbought and stops should be moved up to $48 where the bullish trend line currently resides. Weighting should be revised back to portfolio weight.

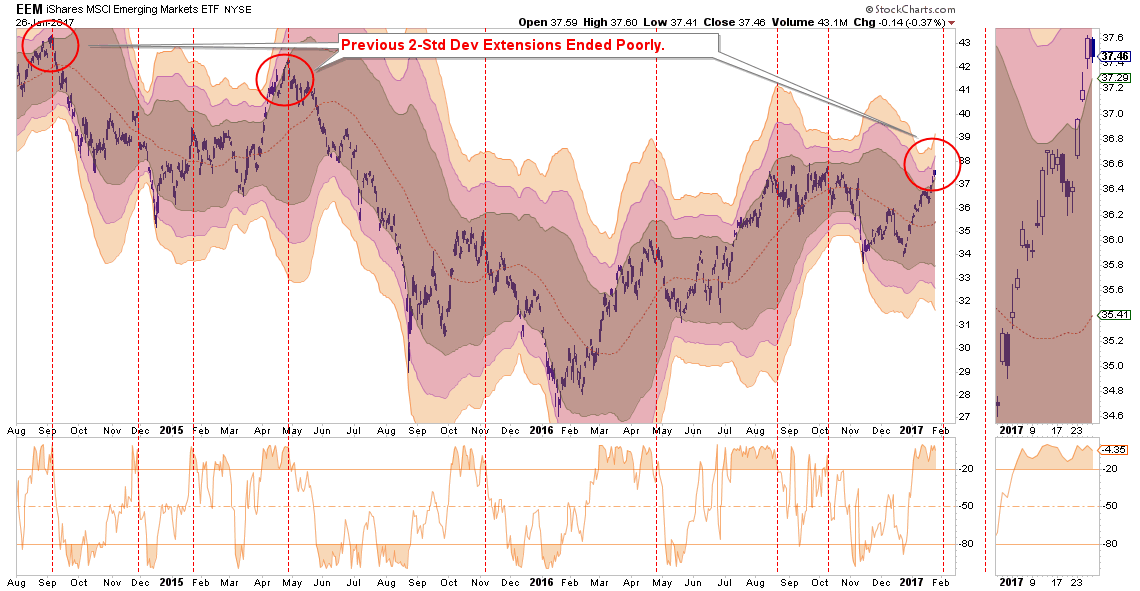

EMERGING MARKETS

Emerging markets have had a very strong performance as of late and are now 3-standard deviations above the mean which is “rarefied air.” The strengthening of the US Dollar will weigh on the sector and will only get worse the longer it lasts. With the sector overbought, the majority of the gains in the sector have likely been achieved. Profits should be harvested and the sector under-weighted in portfolios. Long-term underperformance of the sector relative to domestic stocks continues to keep emerging markets unfavored in allocation models for now.

INTERNATIONAL MARKETS

As with Emerging Markets, International sectors also remain extremely overbought and unfavored in models due to the long-term underperformance. Underweight the sector, take profits, and focus more on domestic sectors for now.

DOMESTIC MARKETS

As stated above, the S&P 500 is extremely overbought, extended and exuberant. However, while a “buy signal” is currently in place, a sell signal registered from such a high level has previously coincided with bigger corrections.

Caution still advised for now.

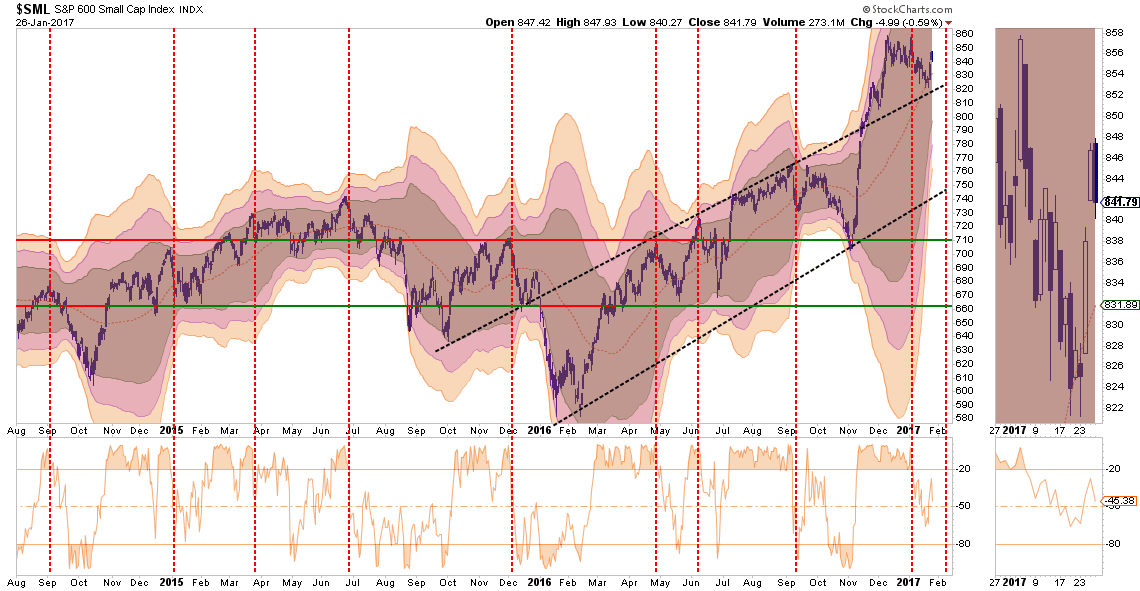

SMALL CAP

Small cap stocks went from underperforming the broader market to exploding following the Trump election. With the index bouncing off the bullish uptrend line recently, a break out to new highs could signal a continued move higher.

Currently, small caps are between overbought and oversold which suggests the current corrective process is likely not complete yet. Reduce exposure back to portfolio weight for now and carry a stop at $820.

MID-CAP

As with small cap stocks above, mid-capitalization companies having a rush of exuberance. However, Mid-caps currently remain extremely overbought. Reduce exposure back to portfolio weight for now and carry a stop at $1660.

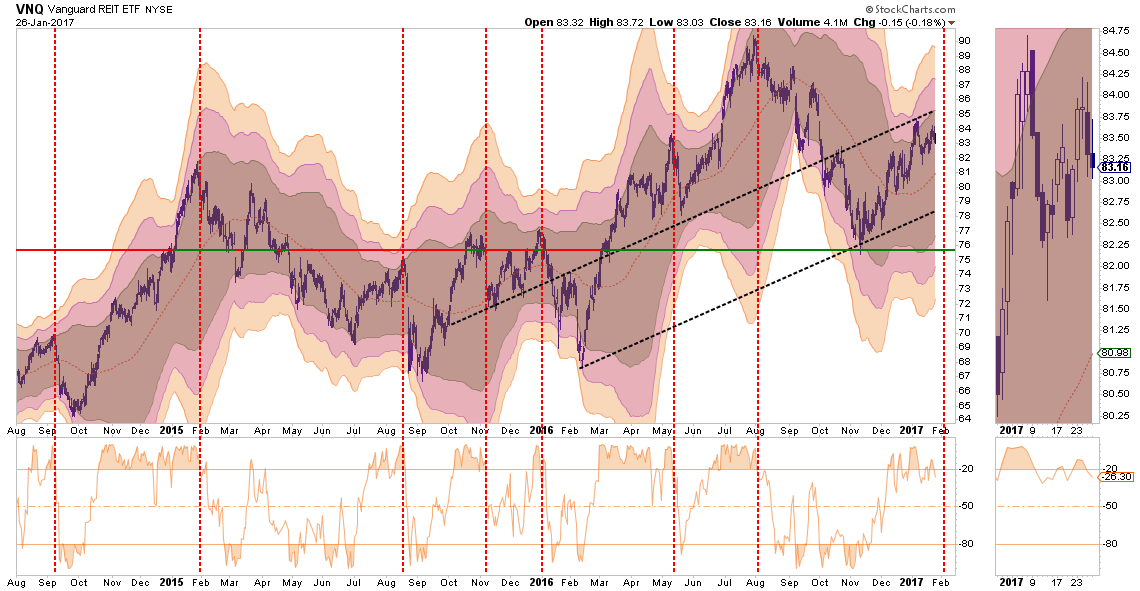

REIT’s

REIT’s had been under pressure heading into the election. However, since then there has been a nice reversal of performance for the sector. However, when rates begin to reverse as “risk” rotates back into “safety,” the risk-reward setup to add REIT’s to portfolios is positive. Positions can be added on a pullback to support at $81 with a stop set at $78.

IMPORTANT NOTE:

If you go back through all the charts and note the vertical RED-DASHED lines, you will discover that each time previously these lines denoted the peak of the current advance. Overall, in the majority of cases above, the risk/reward of the market is NOT favorable.

If, and when, the market corrects some of the short-term overbought conditions which currently exist, equity risk related exposure can be added back to portfolios.

Just be cautious for the moment.

It is much harder to make up losses than simply adding preserved cash back into portfolios.