Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market & Sectors For Traders

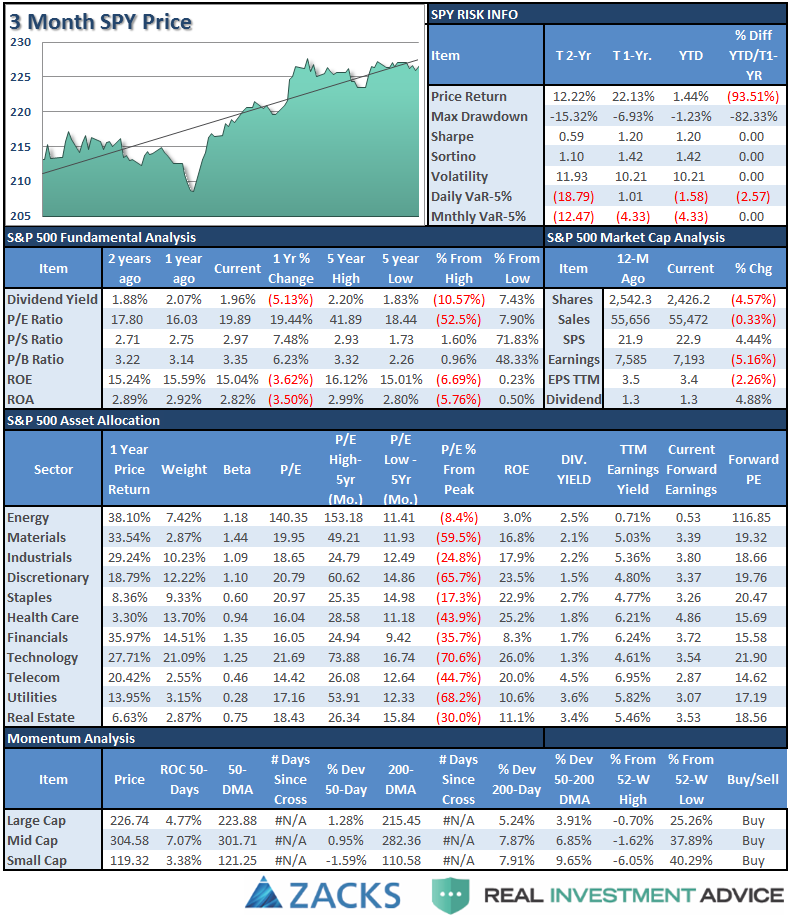

S&P 500 Tear Sheet

The “Tear Sheet” below is a “reference sheet” provide some historical context to markets, sectors, etc. and looking for deviations from historical extremes.

If you have any suggestions or additions you would like to see, send me an email.

Sector Analysis

Comments

With the “inauguration” now behind us, the markets will likely return its focus to earnings, the economy and will keep a close eye on policy indications and changes coming from the White House.

For the second consecutive week, the S&P Index finished lower by 0.15% or -3.33 points. This crushing of investors follows the previous week’s smashing of .1% or -2.74 points. (Once again: #SarcasmAlert)

From last week in case you missed it.

“The video below shows the historical “rotation” of sectors over the last 3-years. As you will notice sectors have consistently “swarmed” in a clockwise rotation going from strongly outperforming the S&P 500 index to strongly underperforming. If you watch to the end of the video you will see the post-presidential election anomaly form.”

I have notated on the Sector Rotation model below, the early stages of the reversion process of the extreme bifurcation between sectors below. Notice interest rate sensitive sectors and Financial’s are beginning to trade momentum.

This rotation is likely very early in its movement. As noted above, while RISK bullishness has reached extremes, SAFETY has been completely disregarded. Reversions tend to be rapid.

Importantly, notice that while Financials, Small and Mid-cap stocks, Energy, Materials, and Industrials continue to lead the S&P 500, their overall strength has begun to weaken.

From a position view, Technology pushed higher last week along with Discretionary, Industrials, Materials, and Staples pushing above it 50-dma. Energy, Financials, and Health Care turned lower.

From the broader index positioning:

Small Caps and Bonds turned lower and are testing their 50-dma. Emerging and International markets stagnated even though the dollar weakened a bit as these markets are extremely overbought. Dividend yielding stocks, REIT’s and Mid-Caps stalled while Gold turned up and broke above its negative trending 50-dma.

The table below shows thoughts on specific actions related to the current market environment. (These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Seven weeks ago, as suggested, we hedged our long-equity positions with deeply out-of-favor sectors of the market (Bonds, REIT’s, Staples, Utilities) which have continued to perform well in reducing overall portfolio volatility risk.

As I have been warning over the last couple of months, the stronger dollar and the rise in rates should not be dismissed.

Everything is currently pointing to this being a very late stage advance, so profit taking, hedging, and rebalancing remains strongly advised.