Written by Lance Roberts, Clarity Financial

I still expect such could very well be the case with a ‘”Santa Claus” rally into the end of the year as fund managers scramble to add performance before the year-end reporting period comes to an end. This would certainly coincide with the “hope” that investors have currently built into the market during the recent advance.

As I noted last Thursday:

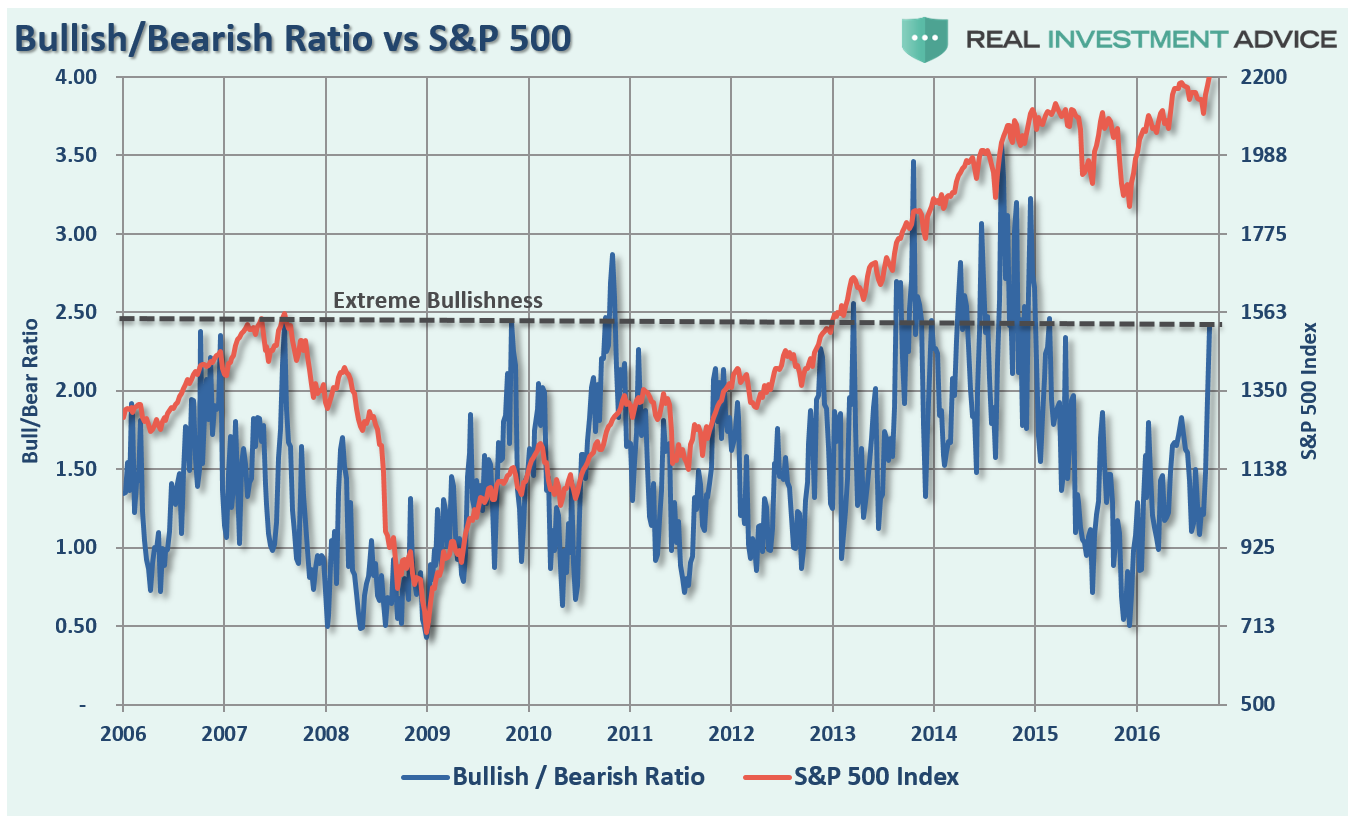

“This post-election surge in investor optimism is shown below. The first chart is the bull/bear ratio of both professional investors (as represented by the INVI Index) and individuals (from AAII). Currently, the level of bullishness has surged to levels more normally associated with intermediate term tops in the market.”

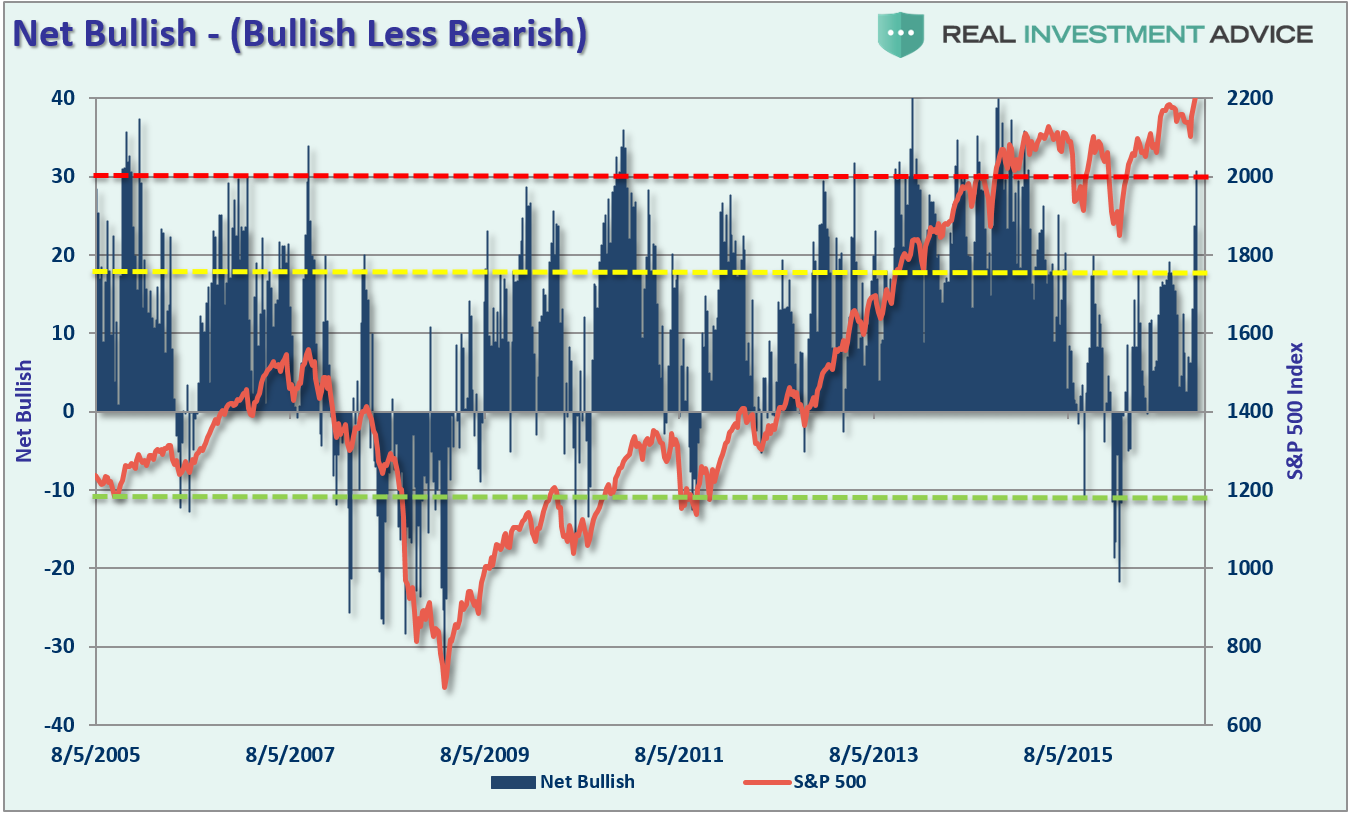

“The net bullishness (bulls minus bears) of both individual and professional investors has likewise surged to levels which again have been more historically representative to intermediate term tops in the market.”

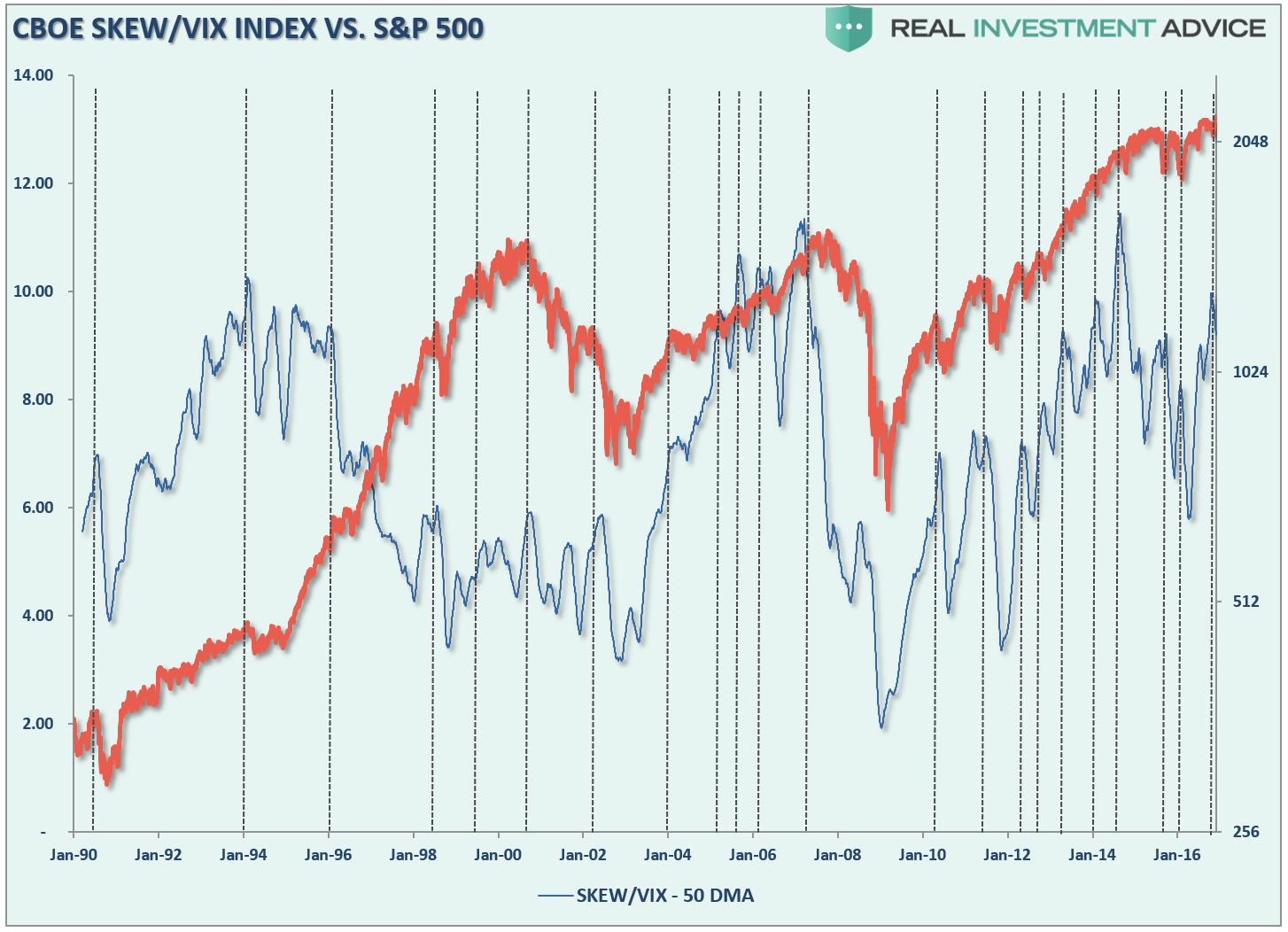

This exuberance, and risk of a correction, is further confirmed by the CBOE SKEW index which is an option-based indicator that measures the perceived tail risk of the distribution of S&P 500 log returns at a 30- day horizon. Tail risk is the risk associated with an increase in the probability of outlier returns, returns two or more standard deviations below the mean. Think stock market crash, or black swan. This probability is negligible for a normal distribution, but can be significant for distributions which are skewed and have fat tails.

I have taken the SKEW index and divided it by the VIX to create a “fear gauge.” To smooth out the volatility of daily data I have used a 50-day moving average. The vertical dashed lines show that peaks in the SKEW/VIX index have corresponded to either short to intermediate-term peaks.

Importantly, you will notice that historically when the gauge has gotten to these levels previously, we have been near major market peaks. Maybe this time will be different, but some caution is likely wise.

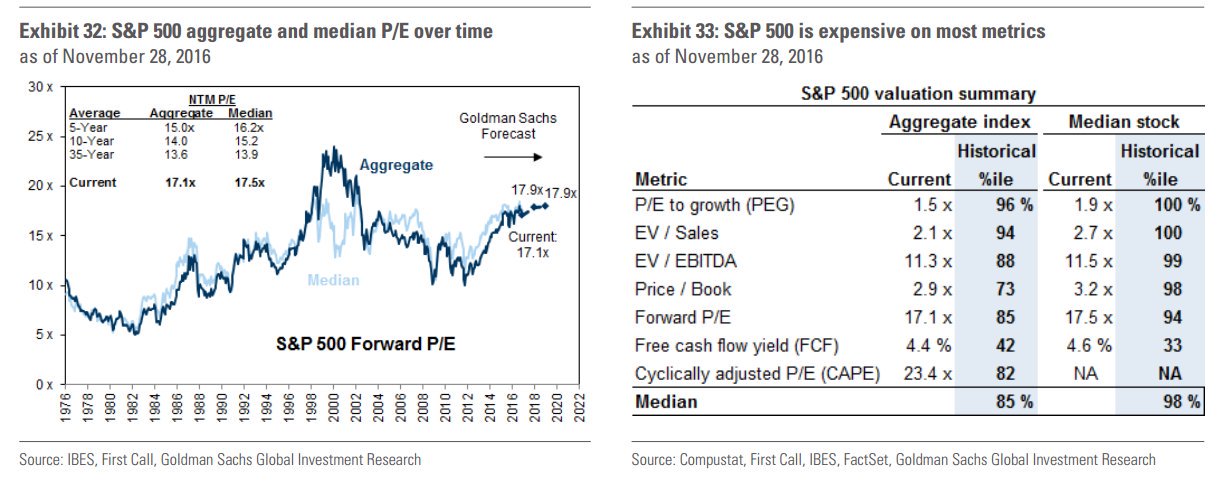

This is particularly the case when you combine the underlying fundamentals with the current levels of exuberance. To wit from Jesse Felder yesterday

Valuations via @NickatFP pic.twitter.com/axpniWsSB8

– Jesse Felder (@jessefelder) November 30, 2016

It is unlikely that with valuations currently all pushing upper deciles that a new secular bull market has begun. However, there are many more similarities to the exuberance seen in 1999 versus 1980.

With that said, it is quite likely a bulk of “hope generated” market gains from “Trumponomics” is complete.

While I am not suggesting the market is about to “crash” in a fiery mass, I am suggesting the “ebullience” of the markets over the last 8-years has likely priced in any real net effects of fiscal policy changes at this point.

In other words, changes to fiscal policy will likely only offset retractions of monetary policy.