Written by Lance Roberts, Clarity Financial

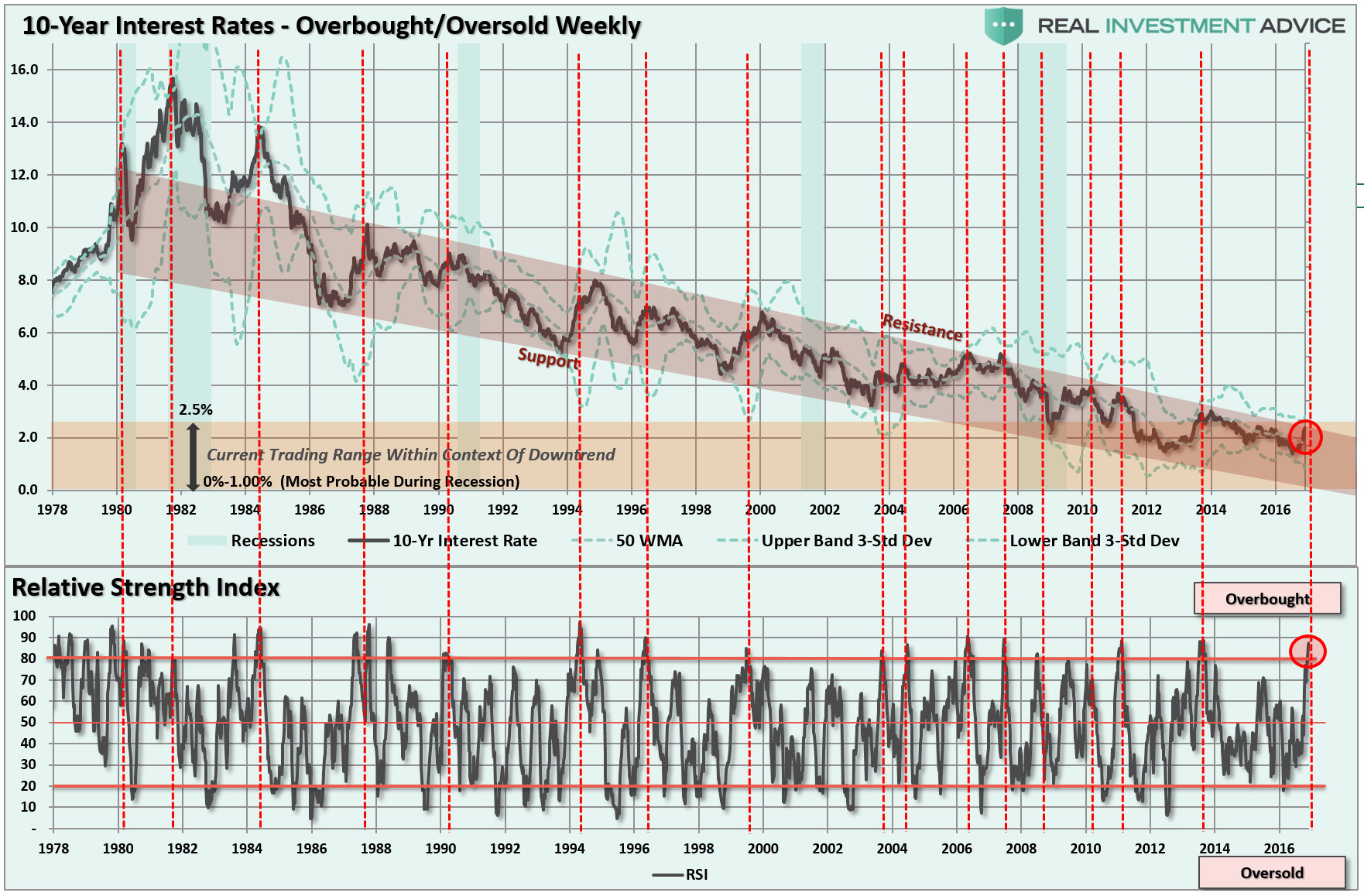

Rates did drift slightly higher this past week but still well within the context of the long-term downtrend. The chart below shows the long-term trend of the 10-year Treasury going back to 1978 as compared to its RSI index and I have circled the recent “surge” in rates.

When put into this context, the rise is barely noticeable. However, what is notable is that historically whenever the RSI on rates has exceeded 80%, red dashed lines, it has preceded a subsequent decline in rates. In other words, overbought rates are a signal to buy oversold bonds for a potential reversion trade.

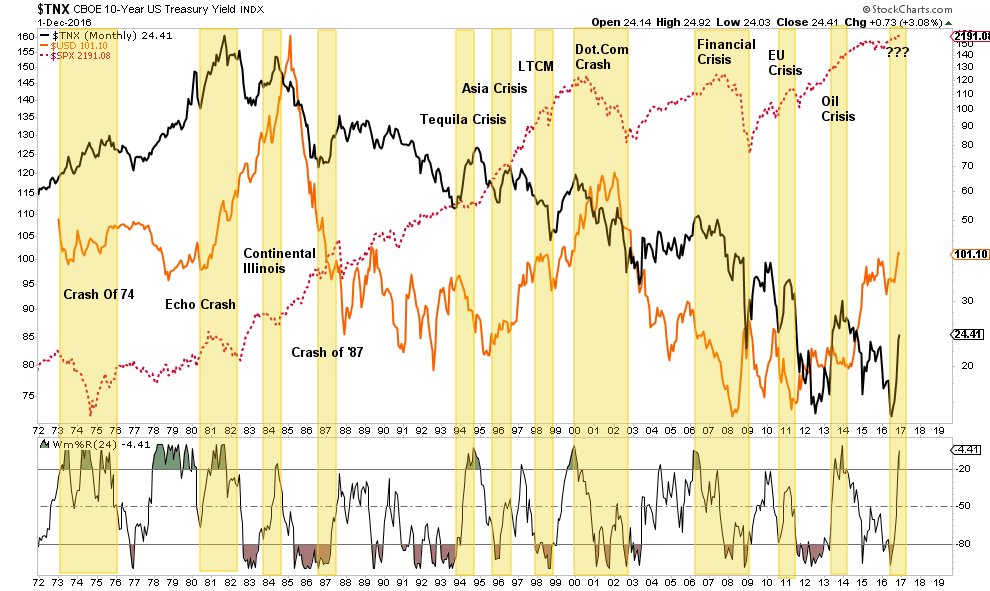

However, the coincident surge in both rates AND the dollar have also put the markets at risk of a bigger “impact correction” due to the simultaneous strain the surging dollar and rates put on foreign exchange and economies. History is littered with incidents that have coincided with similar environments.

Sure, this time could be different…it just usually isn’t.

As Jeff Gundlach noted on Thursday:

“The strong U.S. stock market rally, surge in Treasury yields and strength in the U.S. dollar since Trump’s surprising presidential victory more than three weeks ago look to be ‘losing steam.’

The bar was so low on Trump to the point people were expecting markets will go down 80 percent and global depression – and now this guy is the Wizard of Oz and so expectations are high. There’s no magic here.”

“Investors are misguided in betting that promised tax cuts, infrastructure spending and deregulation will spur faster growth, as the benefits from such fiscal stimulus likely would be temporary.

A strong dollar and continuing structural headwinds including aging demographics, de-globalization trade policies, and accelerating debt-to-GDP in almost all countries at now higher interest rates, promise to contain productivity at perhaps 1 percent annual growth rates and therefore real GDP growth at 2 percent.“

Here is the most important point to remember. Just two months ago, we were told that U.S. equities should rise because bond yields would be low forever, discount rates should trend toward 0%, and therefore equity valuations should trend toward infinity over time.

Now, we’re told that despite bond yields surging we can still count on U.S. equities trending toward infinity because they’re better positioned to absorb higher rates than emerging markets.

It can’t be both.

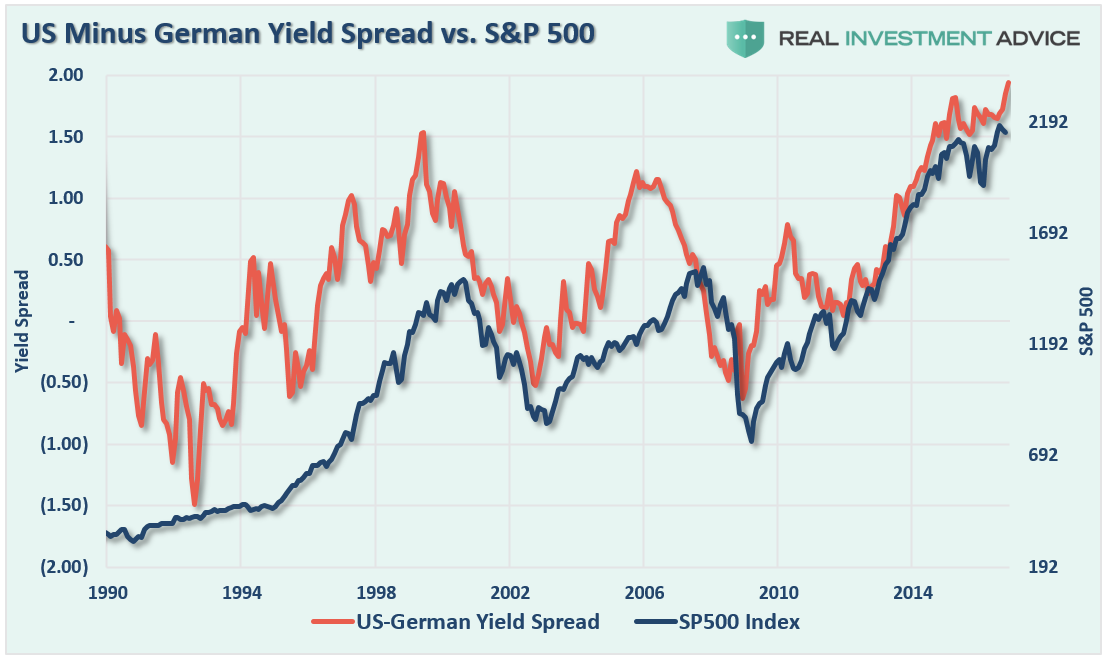

The chart below shows the 10-year Treasury rate the German Bund rate. Not surprisingly, since rate spreads directly impact economic activity, trade, and currency flows, whenever spreads widen to such a degree, bad things have tended to happen.

Just pay attention.