Written by Lance Roberts, Clarity Financial

The Great Bond Crash of 2016

“OMG…Are interest rates ever going to stop rising? My bond funds are getting crushed.”

Actually, it isn’t just bond funds it is all interest rate sensitive sectors of the market. But, as I have discussed many times in the past, this is the problem particularly with bond funds and ETF’s – WHICH ARE NOT BONDS.

Actual bonds, which are the only thing you should buy for fixed income in your portfolio, have two key factors:

An actual interest payment is made at specific intervals during the life of the bond, and;

A return of principal function at maturity.

Everything else, bond funds, bond ETF’s, preferred stocks, REIT’s, MLP’s, closed-end funds, and target-date funds that have been passed off as bond substitutes, ARE NOT BONDS.

Interest rates sensitive investments are a trade on the direction of interest rates, just as stocks are a trade on the direction of the equity markets. No more. No less.

And, as you have seen recently, they can, do and will lose value.

However, let’s also put the recent correction in rates into a bit of perspective.

Let’s start with my analysis from last week:

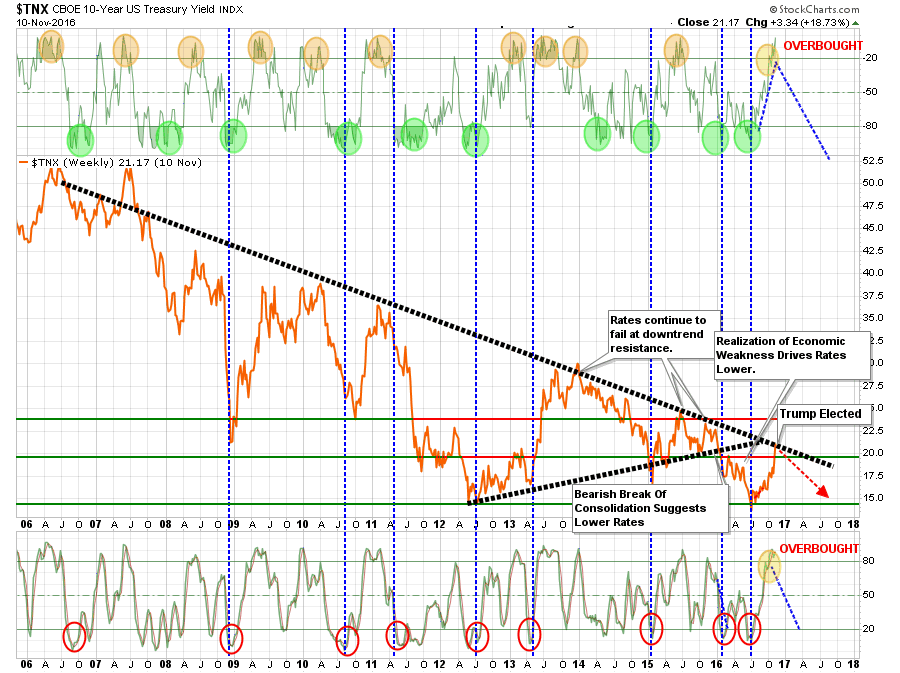

“However, the spike in rates this past week, now has me buying bond ETF”s for a trading opportunity. As shown below, interest rates are now pushing overbought conditions only seen near absolute peaks in interest rates movements. (Orange circles)”

Click on any chart below for larger image.

“What is interesting is that stock buyers are told to buy stocks after big corrections, yet it works EXACTLY the same way with bonds. When interest rates spike, bonds become VERY oversold and operate on exactly the same premises as stocks.

So, bonds are now EXTREMELY oversold and this is as good of an opportunity as one will get to buy bonds.

Does this mean rates will plunge on Monday? No. Rates could go a bit higher from here, but it will likely not be much. As Jeff Gundlach stated last week:

“I do think this rate rise is about 80% through. If yields rise beyond ‘critical resistance’ levels, including 2.35% on the 10-year note, then things are in really big trouble.”

He is right, higher rates negatively impact economic growth. But in BOTH CASES, the outcome for bonds is EXCELLENT.”

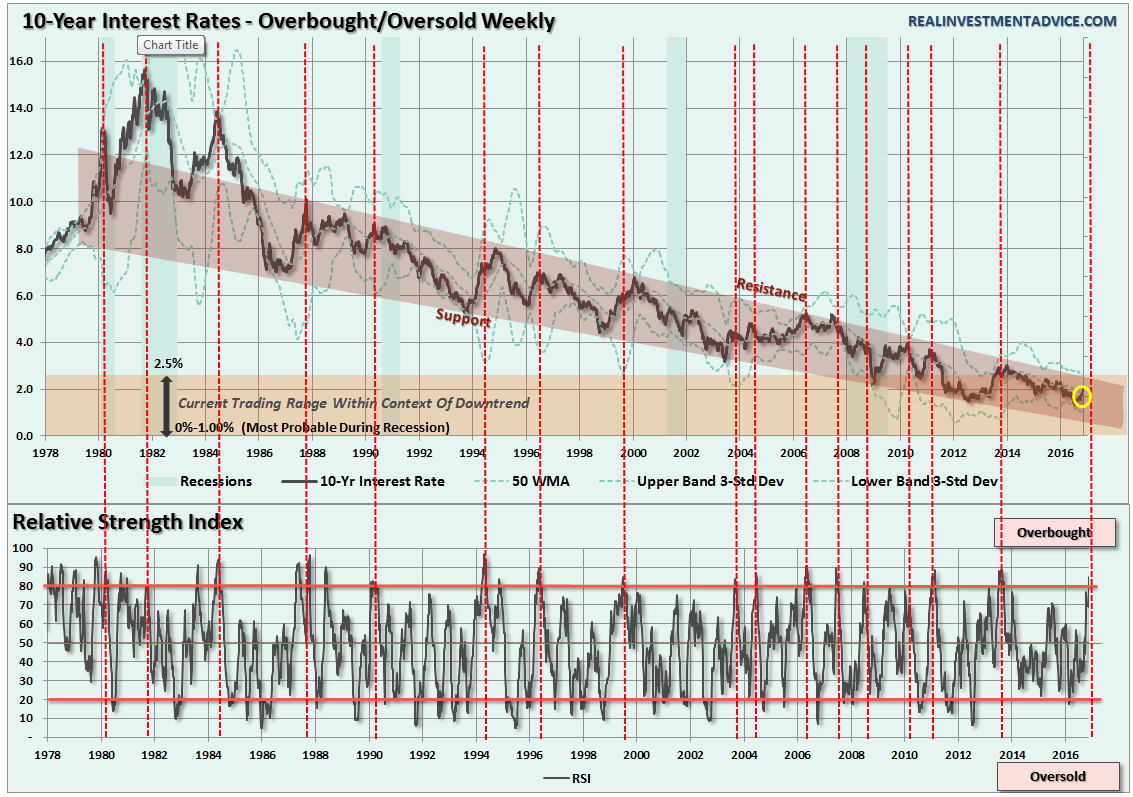

Rates did drift slightly higher this week as stated but still well within the context of the long-term downtrend. The chart below shows the long-term trend of the 10-year Treasury going back to 1978 as compared to its RSI index and I have circled the recent “surge” in rates.

When put into this context, the rise is barely noticeable. However, what is notable is that historically whenever the RSI on rates has exceeded 80%, red dashed lines, it has preceded a subsequent decline in rates. In other words, overbought rates are a signal to buy oversold bonds for a potential reversion trade.

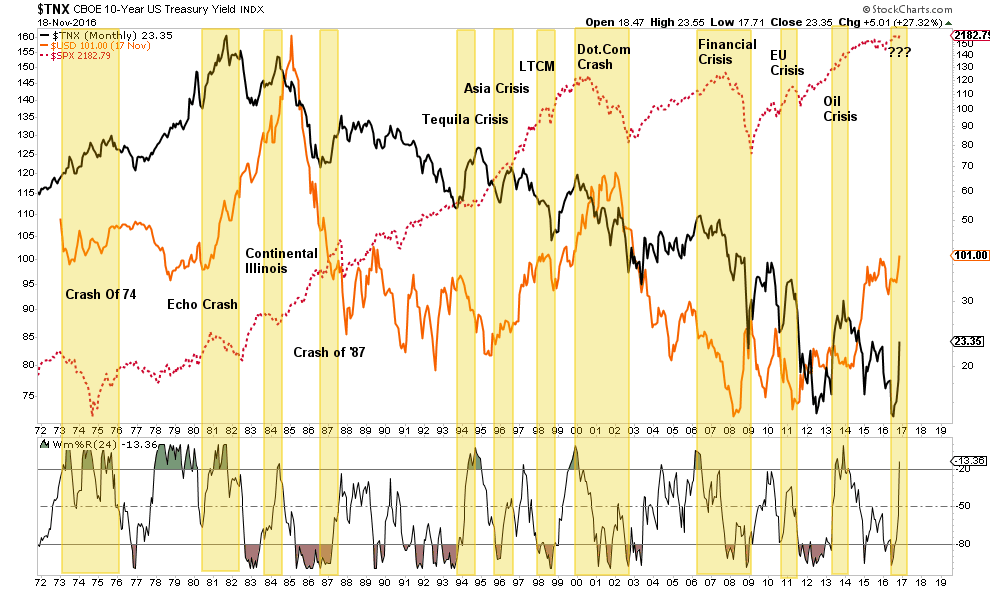

However, the coincident surge in both rates AND the dollar have also put the markets at risk of a bigger “impact correction” due to the simultaneous strain the surging dollar and rates put on foreign exchange and economies. History is littered with incidents that have coincided with similar environments.

Sure, this time could be different…it just usually isn’t.

As Horseman Capital recently penned in a letter to their investors:

“The problem with sharply higher US bond yield is that this tightens financial conditions. We have often seen rises in yield coincide with financial market crises. A rise in yields preceded the 1987 market crash. A rise in yield in 1994 preceded the Tequila crisis, when the Mexican peso devalued by half. After both events, yields quickly fell to new lows. Yields rose in 1996/7 before the Asian Financial Crisis, and yields again rose in 1999 before the dot com crash. After both events, yields fell to new lows. More recently, bond yields rose in 2006 before the Global Financial Crisis, and again in 2010/1 before the Euro-crisis. There was also a rise in yields before the crash in oil prices in 2014. In all cases yields fells to new low.”

Let me repeat:

“While the punditry continues to push a narrative that ‘stocks are the only game in town,’ this will likely turn out to be poor advice. But such is the nature of a media driven analysis with a lack of historical experience or perspective.

From many perspectives, the real risk of the heavy equity exposure in portfolios is outweighed by the potential for further reward. The realization of ‘risk,’ when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower.”

Here is the most important point.

“Just one month ago, we were told that U.S. equities should rise because bond yields would be low forever, discount rates should trend toward 0% and therefore equity valuations should trend toward infinity over time. Now, we’re told that despite bond yields surging we can still count on U.S. equities trending toward infinity because they’re better positioned to absorb higher rates than emerging markets.”

It can’t be both.

While the belief currently is the policies being promoted by President-elect Trump are both stimulative and inflationary, my view aligns with Dr. Lacy Hunt of Hoisington Capital Management:

“Markets have a pronounced tendency to rush to judgment when policy changes occur. When the Obama stimulus of 2009 was announced the presumption was that it would lead to an inflationary boom. Similarly, the unveiling of QE1 raised expectations of a runaway inflation.

Yet, neither happened. The economics are not different. Under present conditions, it is our judgment that the declining secular trend in Treasury bond yields remains intact.”

This is the most important point. Over the intermediate to longer-term time frame, when considering economic and fundamental underpinnings, the consequences of aggressive equity exposure are entirely negative as the rising dollar/yield combination exacerbates the ongoing earnings recession.

In other words, a traditionally overvalued equity market will die a very traditional death.