by Lance Roberts, Clarity Financial

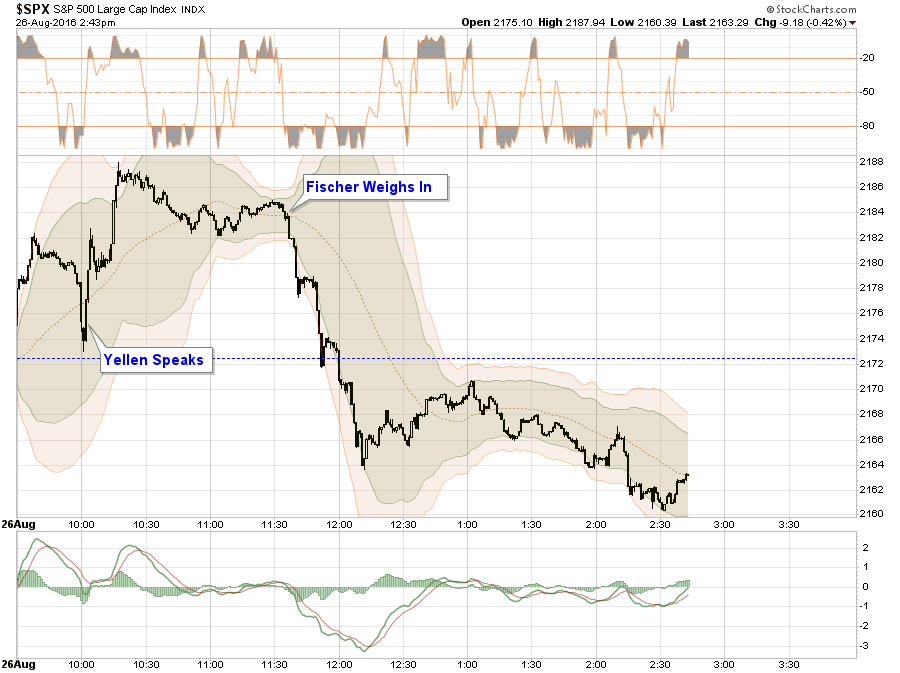

As Yellen spoke on Friday, the markets surged back into the trading range that we have been locked into for the past few weeks. Despite GDP being revised lower and economic data continuing to remain weak, the hopes for a strengthening economic recovery from the Fed remain.

Here are Yellen’s key points:

YELLEN SAYS RATE-HIKE CASE `HAS STRENGTHENED IN RECENT MONTHS’

YELLEN SAYS ECONOMY NEARING FED’S EMPLOYMENT, INFLATION GOALS

YELLEN: FOMC NOT ACTIVELY CONSIDERING ADDITIONAL TOOLS

YELLEN SAYS GROWTH NOT RAPID BUT ENOUGH TO IMPROVE LABOR MKT

On those headlines, the market rallied as the expectations for a September rate hike dissolved.

Remember, raising the Fed Funds rate is a tightening of monetary policy which withdraws liquidity from the financial markets. With fundamentals and economics weak, the only supportive argument for higher asset prices, and for “yield chasers” paying 3.5x sales for a 2.5% dividend, is continued accommodative policy.

But it was this statement that sent the markets surging higher:

“On the monetary policy side, future policymakers might choose to consider some additional tools that have been employed by other central banks, though adding them to our toolkit would require a very careful weighing of costs and benefits and, in some cases, could require legislation. For example, future policymakers may wish to explore the possibility of purchasing a broader range of assets.”

This, of course, dovetails with my article from Thursday discussing the recent Fed research paper on the possibility of another $4 Trillion in QE to offset the next recession. To wit:

“David Reifschneider, deputy director of the division of research and statistics for the Federal Reserve board in Washington, D.C., released a staff working paper entitled ‘Gauging The Ability Of The FOMC To Respond To Future Recessions.‘

The conclusion was simply this:

‘Simulations of the FRB/US model of a severe recession suggest that large-scale asset purchases and forward guidance about the future path of the federal funds rate should be able to provide enough additional accommodation to fully compensate for a more limited [ability] to cut short-term interest rates in most, but probably not all, circumstances.’

In other words, the Federal Reserve is rapidly becoming aware they have become caught in a liquidity trap keeping them unable to raise interest rates sufficiently to reload that particular policy tool. As I have discussed in recent weeks, and below, there are an ever growing number of indications the U.S. economy is currently headed towards the next recession.

He compares three policy approaches to offset the next recession.

Fed funds goes into negative territory but there is no breakdown in the structure of economic relationships.

Fed funds returns to zero and keeps it there long enough for unemployment to return to baseline.

Fed funds returns to zero and the FOMC augments it with additional $2-4 Trillion of QE and forward guidance.

In other words, the Fed is already factoring in a scenario in which a shock to the economy leads to additional QE of either $2 trillion, or in a worst case scenario, $4 trillion, effectively doubling the current size of the Fed’s balance sheet.

Here is the problem with the entire analysis. It assumes a normalized economic environment in which the Federal Reserve has several years before the next recession AND that large-scale asset purchases actually create economic growth. Both are likely faulty conclusions.”

Unfortunately, the post-Yellen speech push higher in stocks was quickly reversed when the Federal Reserve’s own Stan Fischer clarified the situation:

FISCHER: I DON’T THINK FED IS BEHIND THE CURVE

FISCHER: YELLEN’S COMMENTS CONSISTENT WITH POSSIBLE SEPT. HIKE

FISCHER: ON EMPLOYMENT, WE’RE DOING WELL

FISCHER: NOT TOO CONCERNED ABOUT ASSET BUBBLES NOW

So, just as quickly as the rally came, it went away as the specter of a September rate hike weighed on the market.

In a nutshell, the best summation of Yellen’s speech came from Macquarie’s Thierry Wizman who simply said:

“Yellen’s speech was a whole lot of nothing.” – h/t Zerohedge

Let’s Be Like Japan

But let’s revisit Ms. Yellen’s comments for a moment. As noted, she made two very interesting points. The first was the call for more “fiscal” policy out of Government. This is essentially a call for more government spending. ($19 Trillion In Debt Is A Problem)

Clearly, more expansive government spending, represented in the chart above by the surge in Federal Debt, is having no substantial impact to economic growth. As I have written previously, debt is a retardant to organic economic growth as it diverts dollars from productive investment to debt service.

The second, and most important, was the suggestion of expanding monetary policy programs to include other assets.

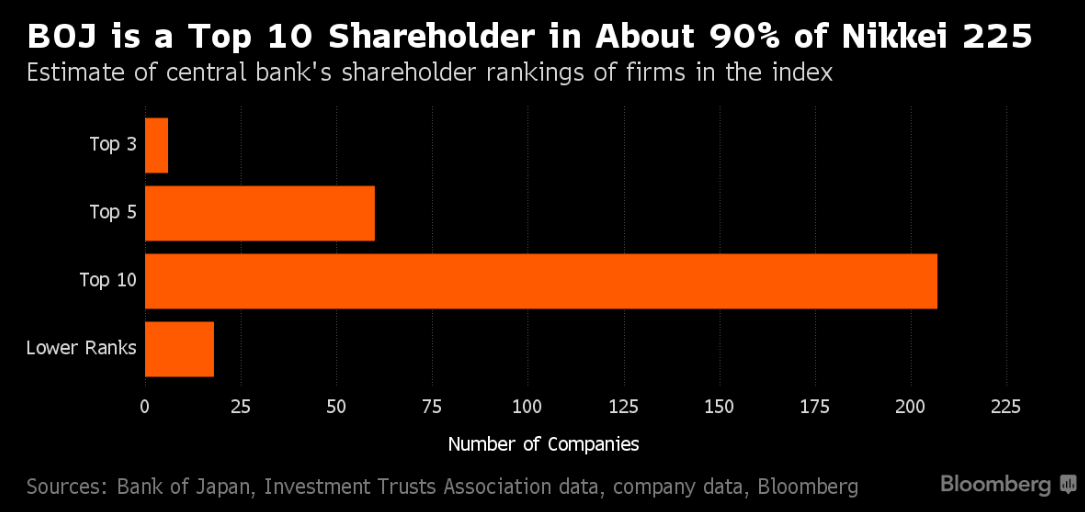

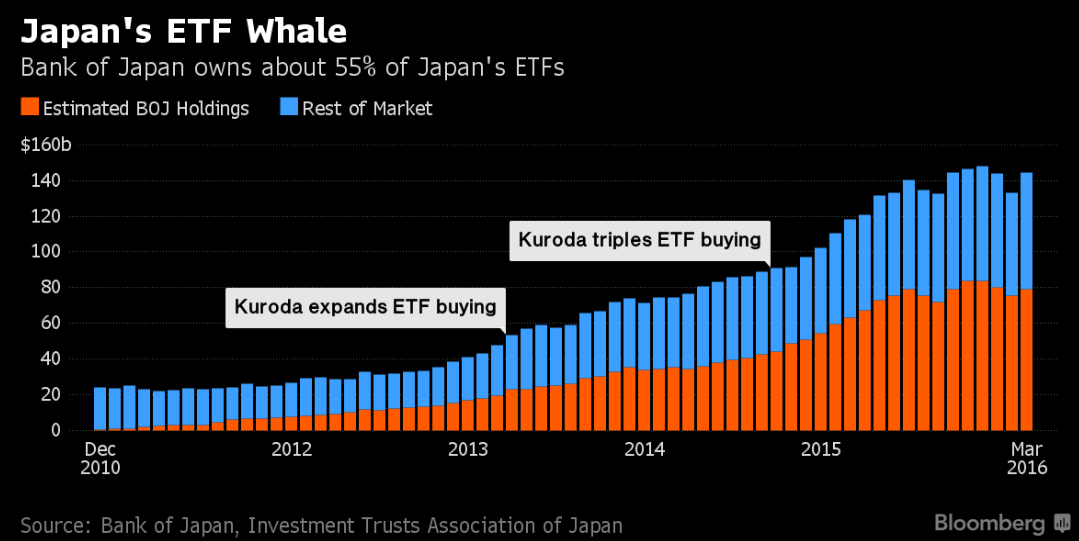

Japan has been doing this for the last couple of years and, according to Bloomberg, has now accumulated a majority of the Nikkei 225 and about 55% of Japan’s ETF’s.

“While the Bank of Japan’s name is nowhere to be found in regulatory filings on major stock investors, the monetary authority’s exchange-traded fund purchases have made it a top 10 shareholder in about 90 percent of the Nikkei 225 Stock Average, according to estimates compiled by Bloomberg from public data.”

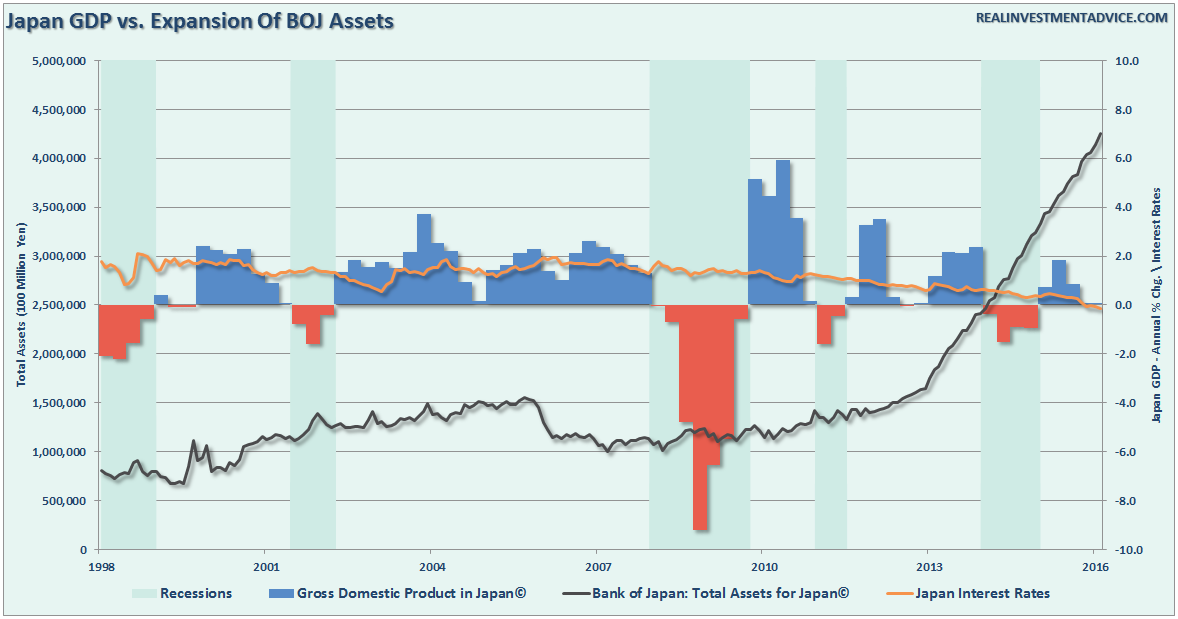

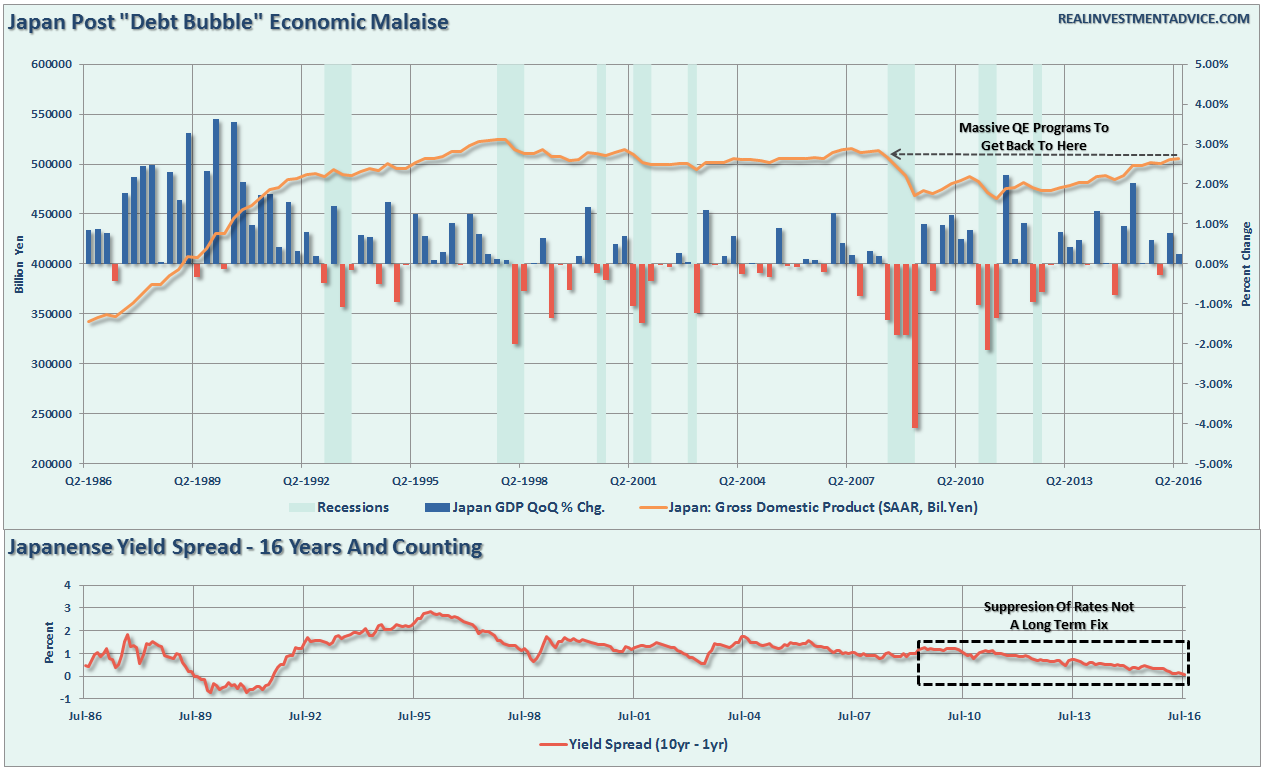

But, that spending has done little for the realization of success in Japan economically. Take a look at the chart below which shows the expansion of the BOJ assets versus growth of GDP and levels of interest rates.

With interest rates now pushing into negative territory and economic growth near zero, there is little evidence to support the idea that inflating asset prices by buying assets leads to stronger economic outcomes.

Yellen has become caught in the same liquidity trap as Japan. With the current economic recovery already pushing the long end of the economic cycle, the risk is rising that the next economic downturn is closer than not. The danger is that the Federal Reserve is now potentially trapped with an inability to use monetary policy tools to offset the next economic decline when it occurs.

This is the same problem that Japan has wrestled with for the last 20 years. While Japan has entered into an unprecedented stimulus program (on a relative basis twice as large as the U.S. on an economy 1/3 the size) there is no guarantee that such a program will result in the desired effect of pulling the Japanese economy out of its 30-year deflationary cycle. The problems that face Japan are similar to what we are currently witnessing in the U.S.:

A decline in savings rates to extremely low levels which depletes productive investments

An aging demographic that is top heavy and drawing on social benefits at an advancing rate.

A heavily indebted economy with debt/GDP ratios above 100%.

A decline in exports due to a weak global economic environment.

Slowing domestic economic growth rates.

An underemployed younger demographic.

An inelastic supply-demand curve

Weak industrial production

Dependence on productivity increases to offset reduced employment

The lynchpin to Japan, and the U.S., remains interest rates. If interest rates rise sharply it is effectively “game over” as borrowing costs surge, deficits balloon, housing falls, revenues weaken and consumer demand wanes. It is the worst thing that can happen to an economy that is currently remaining on life support.

Japan, like the U.S., is caught in an on-going “liquidity trap” where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the ongoing battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments and risk begins to outweigh the potential return.

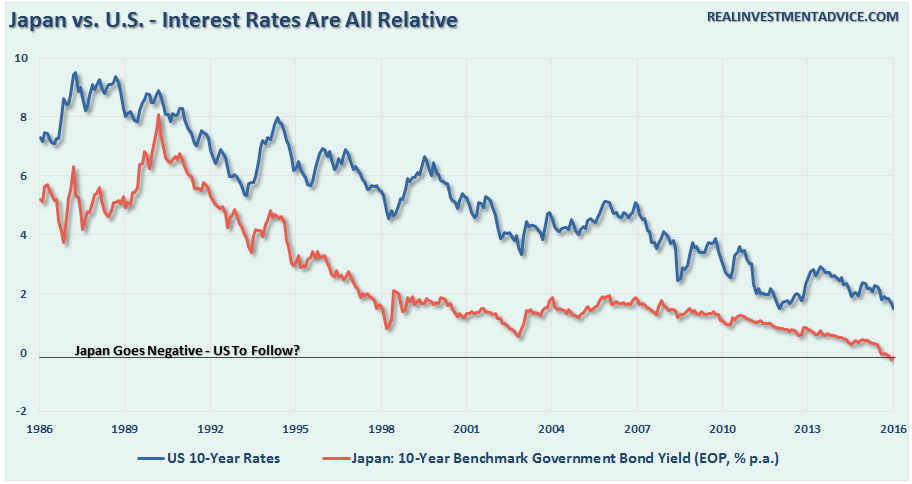

More importantly, while there are many calling for an end of the “Great Bond Bull Market,” this is unlikely the case. As shown in the chart below, interest rates are relative globally. Rates can’t rise in one country while a majority of economies are pushing negative rates. As has been the case over the last 30-years, so goes Japan, so goes the U.S.

Unfortunately, for Ms. Yellen, the reality is MORE spending is unlikely to change the outcome in the U.S. just as it has failed in Japan. The reason is that monetary interventions and government spending don’t create organic, and sustainable, economic growth. Simply pulling forward future consumption through monetary policy continues to leave an ever growing void in the future that must be filled. Eventually, the void will be too great to fill.

But hey, let’s just keep doing the same thing over and over again, which hasn’t worked for anyone as of yet, hoping for a different result.

What’s the worst that could happen?