by Lance Roberts, Clarity Financial

Another week grinds with market action remaining muted as the “dogs days of summer” finally come to a close. But it is next week, as global Central Bankers converge on Jackson Hole, Wyoming, which may give the market some direction before the final push into the November elections.

As Tyler Durden noted on Zerohedge:

“Fed Chair Yellen is scheduled to talk on Friday, the 26th (the timing of her speech has not yet been released). She is likely to spend time discussing the latest star at the Fed – R*, which is the equilibrium Fed funds rate. The short-term R*, which represents the equilibrium rate impacted by current headwinds, is believed to be about 0% in real terms. With the real Fed Funds rate running below, Yellen will likely argue that policy is still accommodative. We expect Yellen to reiterate the desire to keep policy stimulative, given a ‘risk-management’ approach. There is asymmetry to policy when so close to the zero bound – hiking too quickly could derail the economy, but going slowly will simply mean a risk of having to play catchup. In this context, Yellen might argue that conditions are increasingly being met to further normalize rates before the end of the year, consistent with the latest communication from the FOMC. However, we do not expect guidance on the exact timing of the next hike.”

The more in-depth conversation is likely to be over how policymakers should calibrate policy going forward, assuming that R* is permanently lower and central bank balance sheets are permanently larger. This goes back to the topic of the conference – designing resilient frameworks. We think this will include debates about financial stability concerns, global central bank policy coordination, benefits/costs of negative rates and the effectiveness of forward guidance. “

Here is the point. Given economic growth remains nascent and real interest rates, ie LIBOR, are rising, the risk of a monetary policy error for the Fed has grown markedly. As I addressed previously:

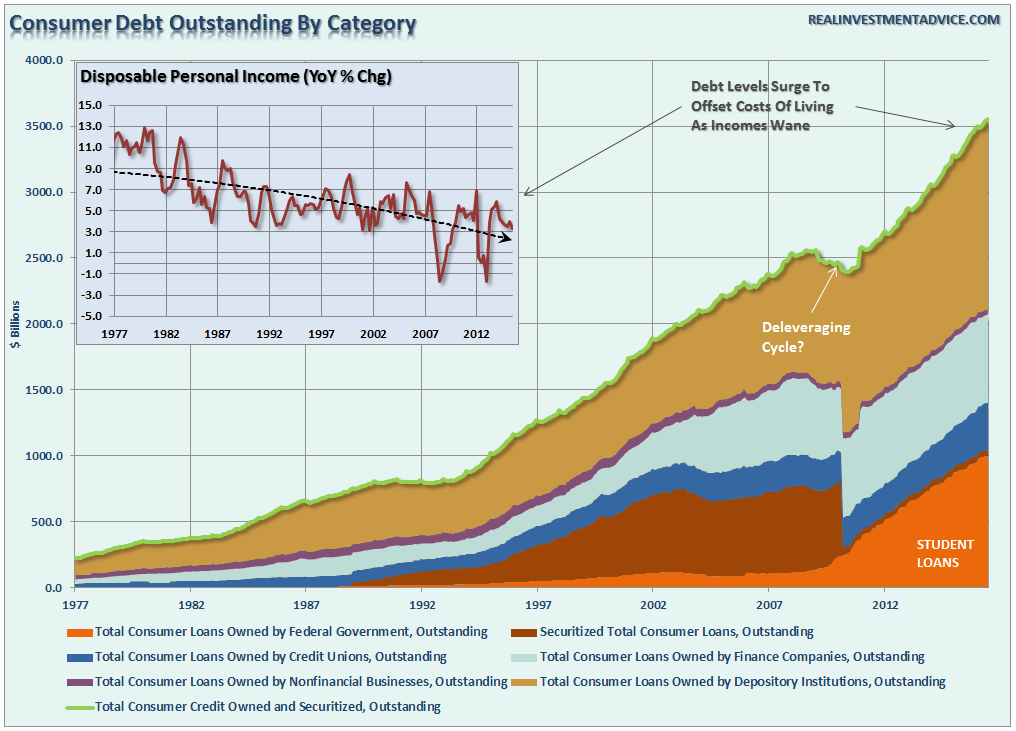

“In other words, increases in LIBOR tightens the flow of liquidity in many of the debt markets that directly affect the average consumer and small business by increasing costs. This is particularly burdensome when annual rates disposable income growth is on the decline.

Danielle DiMartino-Booth pointed out this problem in her latest post:

“Disposable personal income growth, adjusted for inflation, grew by 2.2 percent over last year, a full percentage point below March’s 3.2-percent pace. That downshift helps explain two things. For starters, the saving rate fell in June to 5.3 percent, the lowest since last October. Meanwhile, revolving credit growth, aka credit card spending, galloped ahead at a 9.7-percent annual rate.”

“In other words, consumers are turning to credit consumption to support their current standard of living rather than the expansion of consumption. This is why economic growth continues to wane.

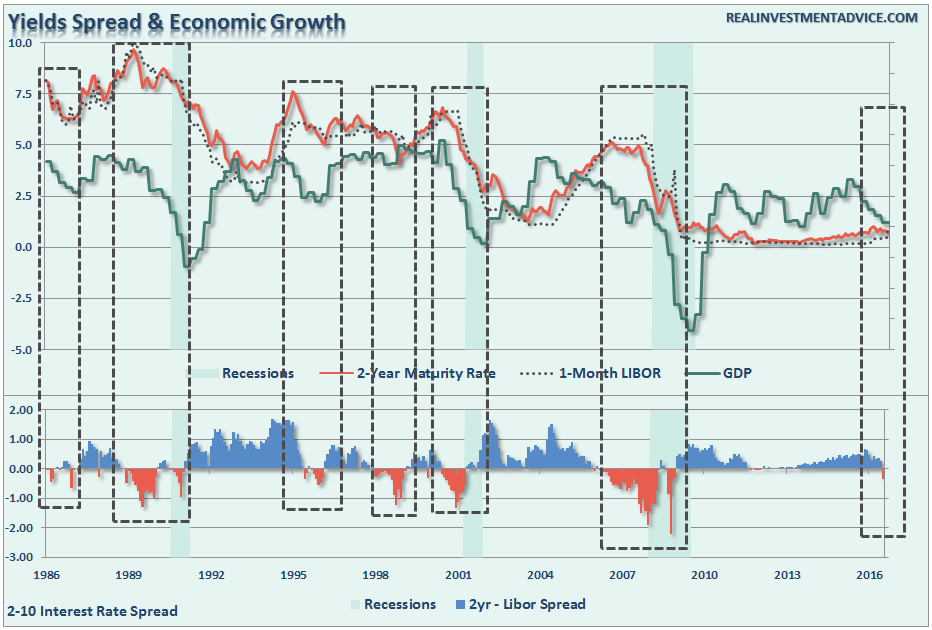

This brings me to my point. If it is LIBOR that affects the consumer, and ultimately economic growth given the 70%ish contribution of consumption to it, then we should be looking at the rates that directly impact the consumer. Whether it is auto loans, mortgages, variable rate debt, credit cards, etc., those interest rate costs are directly impacted by changes in LIBOR.

We can see this more clearly by looking at the very short-end of the yield curve and the spread between the 2-year Treasury rate and the 1-month LIBOR.”

As shown, there is a very high correlation between negative spreads and future economic growth. In every instance where there has been a negative spread on rates, the economy has either slowed markedly or was in a recession.

The problem for the Fed is now trying to play catch up with LIBOR without pushing a 1%-growth economy into recession.

With interest rates near their lowest levels in history, and roughly 500-million people globally under NEGATIVE rates, there is little evidence of a resurgence of economic growth on the horizon. As Simon Black correctly stated:

“Remember that money is essentially nothing more than a measurement of economic value, in the same way that a meter or a mile is a measure of distance.

Just imagine the chaos if there were some unelected committee of bureaucrats who got together from time to time to change the value of the mile. Or imagine if, tomorrow morning, they decided that the mile would be shortened by 20%.

Some people would benefit from that arrangement (taxi drivers). Others would be worse off (taxi passengers). There are always winners and losers.

Similarly, there are always winners and losers with monetary policy.

And these unelected central bankers have made a series of very deliberate decisions to forsake one segment of the population (anyone trying to save money) for the benefit of another (those who are heavily in debt, like, ummmm, governments).”

Bingo!

Unfortunately, however, the problem of forsaking savers over debtors is simply “savings” is what drives economic growth. Surging debt levels is a detractor to savings and ultimately diverts money from productive investments into debt service.

As John Hussman noted this past week:

“I can’t emphasize strongly enough that there is no economic evidence that activist monetary intervention has materially improved economic performance in recent years. Specifically, the trajectory of the economy in recent years has followed a largely mean-reverting course that one could have anticipated simply on the basis of lagged economic data, and there is no economically meaningful difference in the projected trajectories of GDP, industrial production, and employment using purely non-monetary variables, compared with projections that include measures of recent extraordinary monetary policy.”

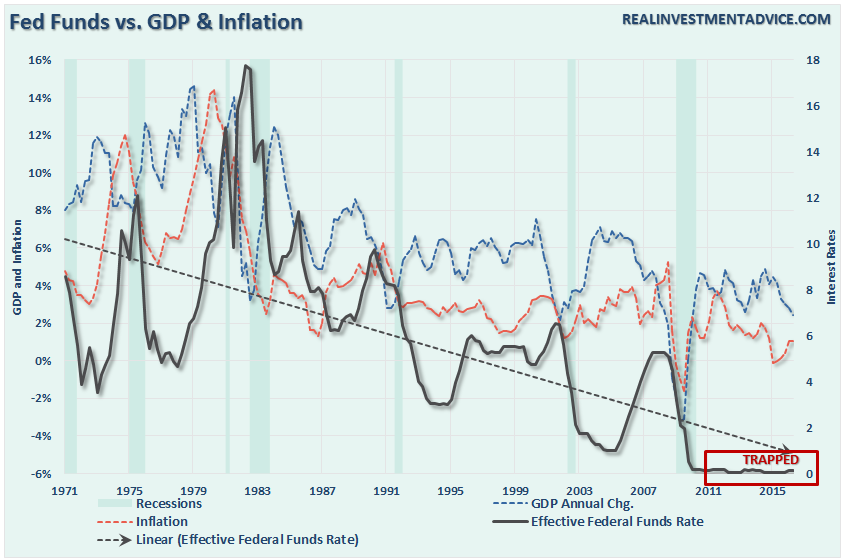

This is, of course, absolutely correct. The problem for Global Central Bankers is they are attacking the problem with a blunt instrument that has already been proved to “fail” over long periods of time. As discussed earlier this week, the Fed has become caught in the same “liquidity trap” that has plagued Japan for the last 30-years.

“The signature characteristic of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

As the chart below shows, the Fed has actually been trapped for a very long time but has failed to realize it. This has kept the Fed inflating asset prices and suppressing yields for far too long which, as discussed below, has led to “euphoric market conditions with poor outcomes.”

What was that definition of insanity again?

Euphoria Already Upon Us

As I noted last week:

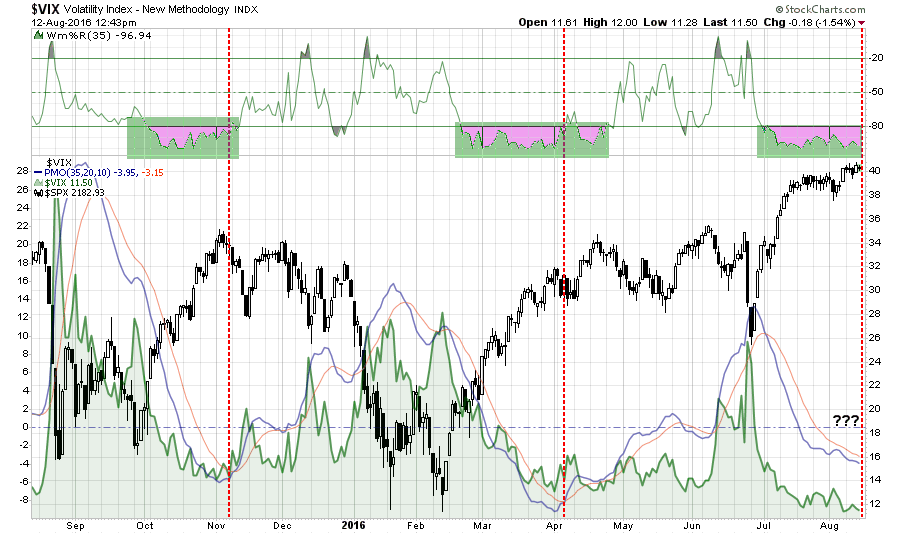

“The level of “complacency” in the market has simply gotten to an extreme that rarely last’s long. The chart below is the comparison of the S&P 500 to the Volatility Index. As you will note, when the momentum of the VIX has reached current levels, the market has generally stalled out, as we are witnessing now, followed by a more corrective action as volatility increases.”

Disclosure: I am currently long the volatility index as of this past Monday.

The bet on a sharp rise in volatility is a hedge against a sharp reversion in asset prices as the high level of “complacency” unwinds. As Eric Parnell recently wrote:

“So if its not in the broader market as measured by the S&P 500 Index where exactly does the euphoria lie today? It does not lie in stock prices themselves, but instead in how much investors are willing to pay for each dollar of earnings from owning stocks, or more simply the price-to-earnings ratio. For while the S&P 500 Index has effectively gone nowhere since the end of 2014 on a price basis, the price that investors have been willing to pay for each dollar of earnings provided by stocks has soared by more than +30% over this same time period.”

“Such rapid multiple expansion is certainly not necessarily unheard of throughout market history. But it typically takes place either in the immediate aftermath of a bear market or when absolute valuations are well below the historical average in the 5 to 12 times earnings range, not at the later stages of a bull market when valuations were already relatively high.

We have seen only three other instances over the past century where a comparable degree of multiple expansion from already high absolute valuations took place. These were 1928-29, 1986-87, and 1998-99. Two of these instances ended notoriously badly, the third resulted in the worst one-day decline in market history from which it took two years to recover despite the dawn of the Fed “put” era. Given that we are similar multiple expansion territory today that has led us to the second highest market valuations in history, it will be interesting to see how this fourth episode plays out.”

As I stated above, it is the repeated Central Bank interventions that have led to this extreme level of complacency combined with over euphoric valuations as the “chase for yield” has ensued. Back to Eric:

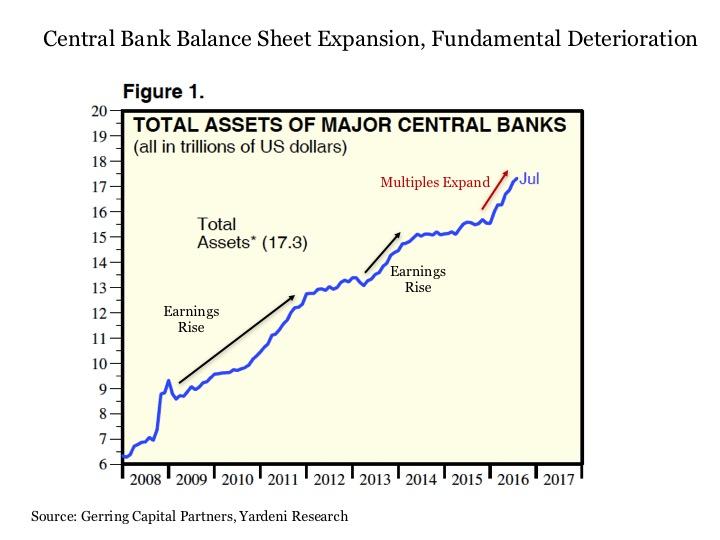

“But what is the driving force behind today’s multiple expansion euphoria? The most likely culprit is the relentless expansion of global central bank balance sheets since the outbreak of the financial crisis nearly a decade ago. Overall, global central bank balance sheets have expanded from just over $5 trillion prior to the crisis in 2007 to nearly $18 trillion today.”

There is little doubt we are currently in a bull market. But as with all things, despite hopes from the mainstream media to the contrary, they do come to an end. This should be of no real surprise to anyone that has managed money for any length of time. As John’s concludes:

“The outcome of years of yield-seeking speculation induced by central banks is that investors across the globe have now locked in zero prospective total returns in virtually in every asset class for the coming decade.

Near term, the single most likely outcome in any given week is a small gain, but that likelihood is also offset by the small probability of a wicked loss that can easily wipe out weeks or months of upside progress in one fell-swoop. Those plunges are random in the sense that we have no idea when they will occur, but they are also predictable in the sense that the underlying probability distribution of returns, during overextended conditions similar to the present, has been fairly stable across decades of market history.

Looking beyond the near-term, my view is that a ‘permanently high plateau’ is unlikely, and we will instead see a violent unwinding of recent speculative extremes over the completion of the current market cycle, even if central banks ease aggressively, as they did throughout the 2000-2002 and 2007-2009 collapses. Corporate income growth and profit margins have already begun to narrow from their extremes, and the default cycle has already turned higher. The completion of this cycle won’t arrive because central banks suddenly become enlightened enough to abandon their recklessness. It will arrive precisely because they have sustained yield-seeking speculation for too long already; because they have amplified the vulnerability of the debt and equity markets to normal economic fluctuations; and because the consequences of this fragility are now fully baked in the cake.”

While you may, or may not, agree with John’s position it can be proved both mathematically and historically.

As I have noted repeatedly in the past, maintaining your portfolio through a disciplined investment process will reduce risk and increase long-term profitability. With markets currently hovering near all-time highs, despite a continuing erosion of underlying fundamental and technical strength, the risk/reward ratio remains out of favor.

Tighten up stop-loss levels to current support levels for each position.

Hedge portfolios against major market declines.

Take profits in positions that have been big winners

Sell laggards and losers

Raise cash and rebalance portfolios to target weightings.