by Lance Roberts, Clarity Financial

Yesterday, media headlines rang out:

“The Markets Just Did Something It Hasn’t Done Since 1999.”

It’s pretty amazing when you think about it for a moment. All three indices hit simultaneous new highs at a time when earnings, profitability, and economic data are deteriorating.

While much of the media analysts continue to suggest there remains a bearish attitude towards stocks, price action of the markets as compared to fundamental data suggests quite the opposite.

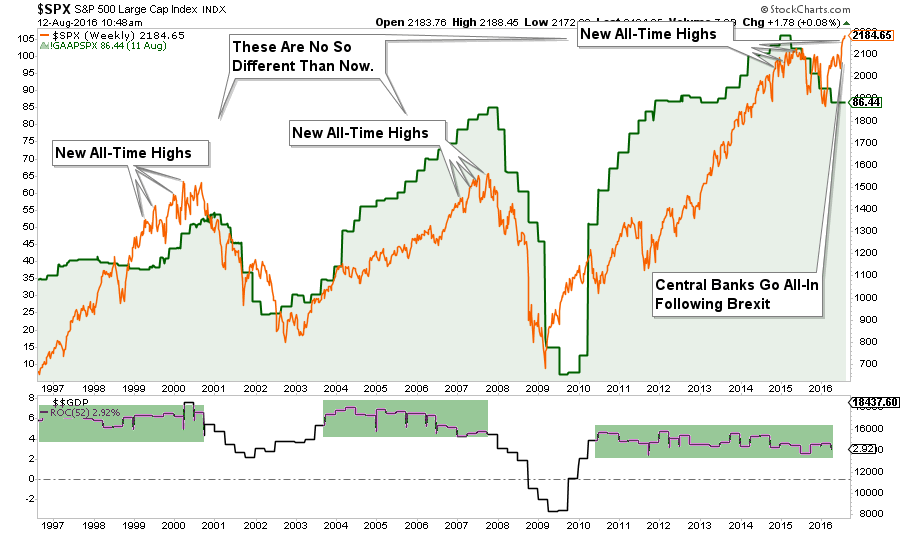

The chart below compares the current S&P 500 to both earnings and the annual ROC in GDP.

Notice any similarities?

Despite a “belief” that “This Time Is Different (TTID)” due to Central Bank interventions, the reality is that it probably isn’t. The only difference is the interventions have elongated the current cycle, and has created a greater deviation, than what would have normally existed. What is “not different this time” is the eventual reversion of that extreme will likely be just as damaging as every other previous bear market in history.

But, of course, “TTID” is the old Central Bank driven mantra, today it is “There Is No Alternative (TINA).” As stated, regardless of what you call it, the results will eventually be the same.

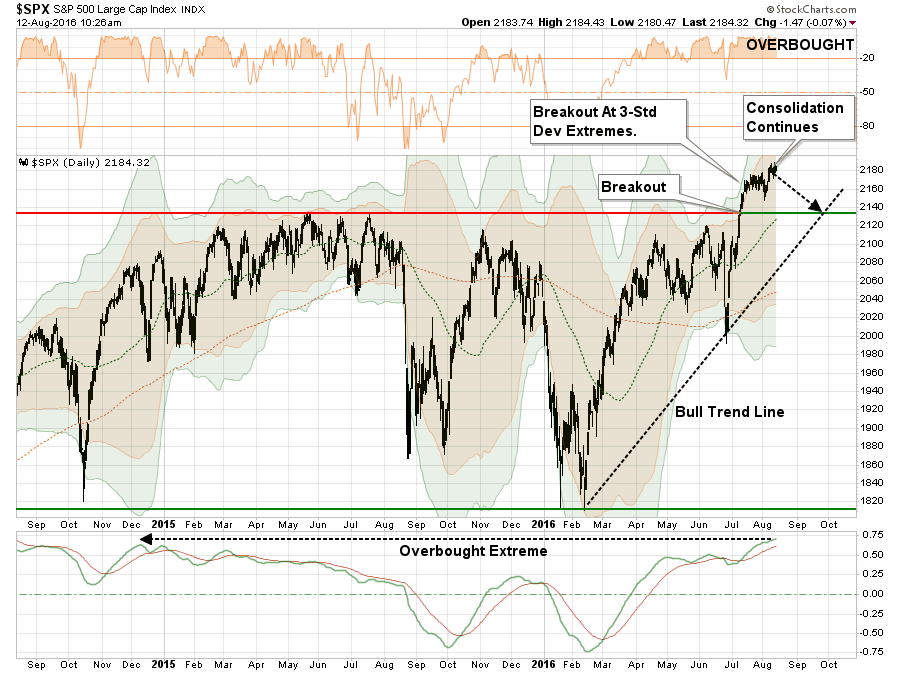

Let’s review where we stand currently.

Chart updated through Friday’s open.

While the market has continued to consolidate gains over the last few weeks, the overbought conditions still remain. As I stated earlier this week:

“The market, on a short-term basis, remains in extreme overbought territory. This needs to be relaxed somewhat before additional equity exposure is added to portfolios. As shown, a reversion to the current bullish trend line, which coincides with the market’s recent breakout levels, is a likely target in the short-term.

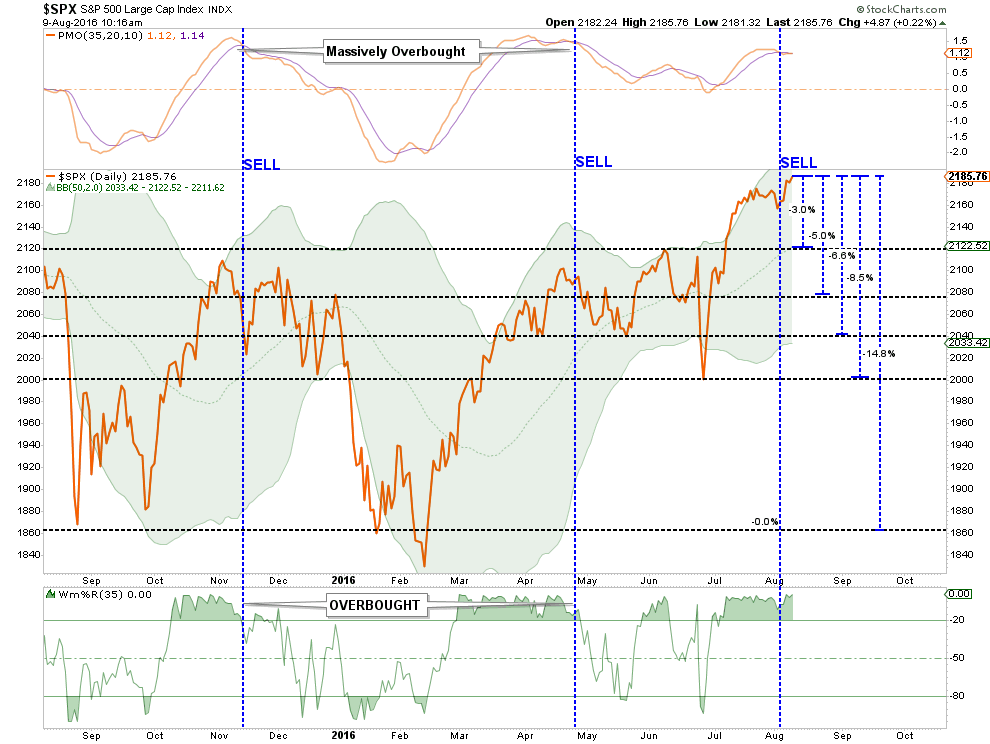

However, there is a more than reasonable chance, as I laid out two weeks ago for a deeper correction in the next 60-days. The chart below shows the potential drawdowns from current levels.”

“Here is the point. It would take a correction from current levels to break 2000, which is very important support for the markets currently, to even register a 10% correction.

Given the current bullish exuberance for the market, this is probably unlikely between now and the election. Therefore, even a “worst case” correction currently would likely be an 8.5% drawdown back to major support. Of course, for most individuals, even such a small correction would likely feel far more damaging.“

Let’s take a look at some of the issues that suggest a reversion in prices is likely coming sooner rather than later.

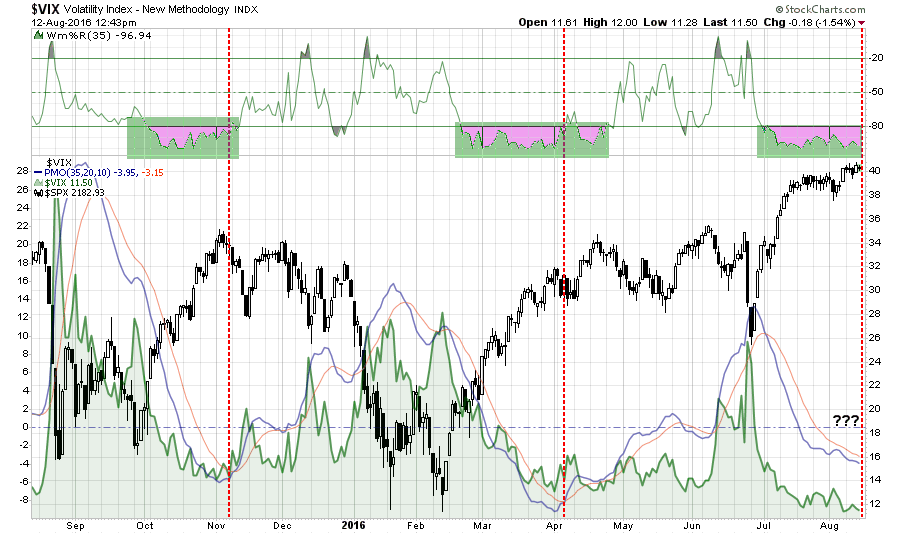

VIX & Junk Bond Spreads Out Of Whack

The level of “complacency” in the market has simply gotten to an extreme that rarely last’s long.

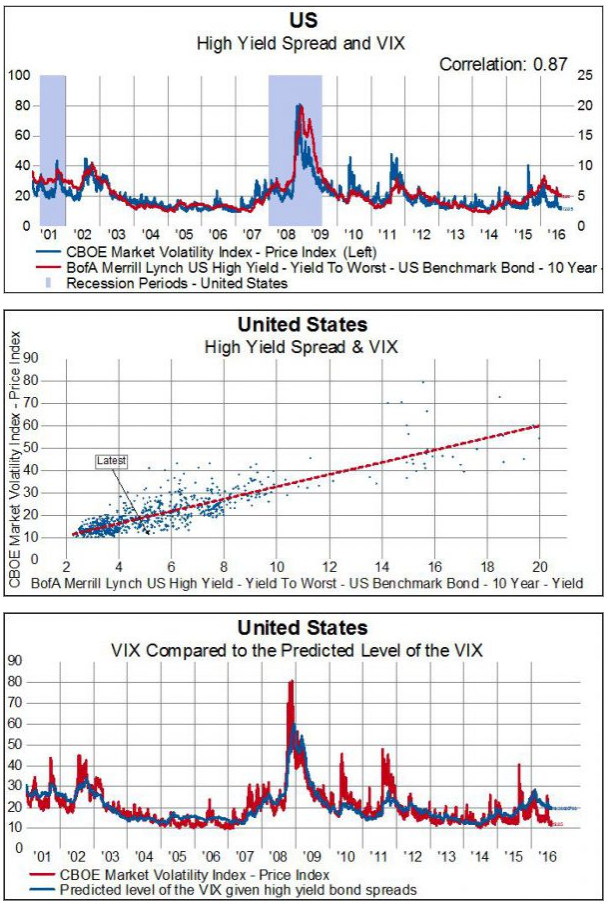

The chart below is the comparison of the S&P 500 to the Volatility Index. As you will note, when the momentum of the VIX has reached current levels, the market has generally stalled out, as we are witnessing now, followed by a more corrective action as volatility increases.

Eric Bush, CFA from GaveKal Research had an excellent piece this week discussing this same idea but also looking at junk bond spreads.

“The relationship between the VIX and the spread between high yield bonds over 10-year treasuries is highly correlated (87% over the past 15 years). This, of course, makes intuitive sense. The VIX tends to spike when confidence in stocks or the economy is shaky. Which is also true for high yield bonds. When investors begin to worry that high yield issuers won’t be able to make debt payments because of, for example, slowing growth, high yield bonds usually sell off against treasury bonds.

This occurred earlier this year in February when the VIX spiked to over 28 and the spreads widened to 850 bps. Since then as investors climb the wall of worry the level of the VIX and high yield spreads have fallen in tandem. However, the level of the VIX has fallen much further and signifies that fears in the equity market are much lower than fears in the bond market. At no point over the past 15 years has this level of the VIX occurred when high yield bond spreads are this elevated. A simple regression model suggests that the VIX should be around 19 rather than the current level of 12. Or looked at from the other angle, high yield spreads are usually 185 bps lower than they currently are when the VIX is at 12. Presumably, this relationship will begin to normalize. The question that needs to be answered is will it normalize because investors ]bid up high yield bonds or because the complacency in the stock market erodes away?”

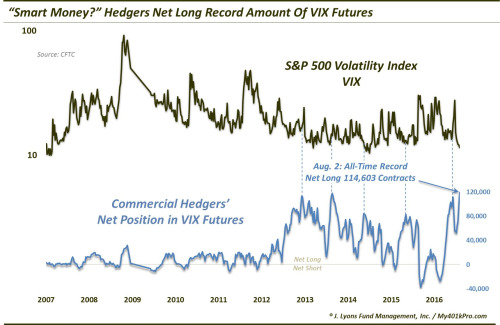

Taking this one step further, Dana Lyons took note of the “Smart Money” hedging against exactly the kind of volatility increase I am discussing. To wit:

“As we have discussed on many occasion, these hedgers are often considered ‘smart money’. This is a bit of a misnomer which causes some confusion every time we use the term. It is not that these hedgers (e.g., banks and large financial institutions) are always right. In fact, they can be wrong for long stretches at a time in a strong trending market. However, we know what typically occurs when the speculators’ positioning becomes too one-sided or extreme – the market reverses on them. And as they are on the other side of the position, these commercial hedgers are typically correctly positioned at major market turns. Thus, the ‘smart money’ moniker.

This is relevant now due to the aforementioned speculator position. As such, commercial hedgers currently own their largest net long position in the 10-year history of the VIX futures contract.”

As always, timing is everything.

The point here is simply the “risk to reward” dynamic for either adding to current long-positions or maintaining overweight equity positions in portfolios will not likely pay well.

As I have noted repeatedly in the past, maintaining your portfolio through a disciplined investment process will reduce risk and increase long-term profitability.

Tighten up stop-loss levels to current support levels for each position.

Hedge portfolios against major market declines.

Take profits in positions that have been big winners

Sell laggards and losers

Raise cash and rebalance portfolios to target weightings.