Written by Lance Roberts, Clarity Financial

From last week:

“So, am I buying equities to move portfolios to the current target allocation?

Not yet.”

I know. Boring.

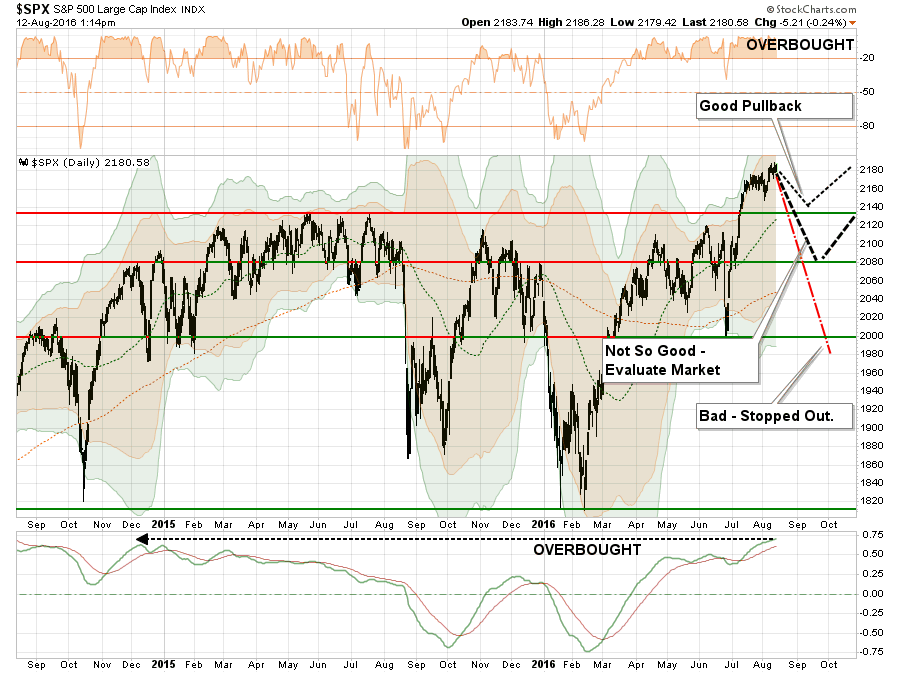

It has now been FIVE weeks since the market broke out of its 18-month consolidation process at which time I laid out the case to increase equity exposure in portfolios. I have been repeating that case here each week, primarily for new readers, with not opportunity to adjust exposures as of yet.

“But Lance, you just laid out a very bearish case for stocks. Why are you talking about increasing exposure?”

That is a fair question.

Managing money is about managing the risk of loss. Notice that I did not say “creating returns.”

If I manage portfolios against the potential of long-term impairment of capital, the creation of returns becomes a byproduct of that effort.

Currently, while there is a very bearish case to be made from the deterioration of economic and fundamental variables relative to the market, the current technical price dynamics are both bullish and positively trending. Therefore, as a money manager, I want to maintain exposure to the equity markets until such time as the technical price dynamics change from bullish to bearish.

I have stated repeatedly over the last couple of weeks that the breakout of the market above the 18-month consolidation range was bullish and demands an increase in equity exposure. However, such an increase must be done when the risk-to-reward ratio is favorable which is what I am currently patiently waiting for. I have laid out the potential price corrections needed to both warrant, and negate, such an equity exposure increase.

As Doug Kass noted this past week, there is a trio of factors pushing stocks higher.

“Central-bank policies are succeeding in encouraging risk takers to take more risks in long-duration financial assets, while central-bank purchases have sent financial-asset prices spiraling upward and reduced volatility (as measured by the VIX). This has created what I call the Bull Market in Complacency – an almost universal view that any drawdown in market prices will be limited.

Many U.S. corporations that face lackluster top-line growth are repurchasing stock in record amounts at record prices rather than doing capital spending to bolster their physical plant. This boosts stock prices, satisfying large shareholders and feathering insiders’ portfolios.

While many retail investors are long gone from the stock market, volatility-trending strategies, risk-parity trading systems and other quant programs keep pushing stock prices to new all-time highs.

All this feeds on itself, but what’s surprising is that few question how the above factors contribute to higher asset prices. They fail to recognize that if there were no adverse consequences low or negative interest rates, massive liquidity injections and central banks buying stocks, these would have become permanent and continuous monetary-policy strategies decades ago.“

Bingo.

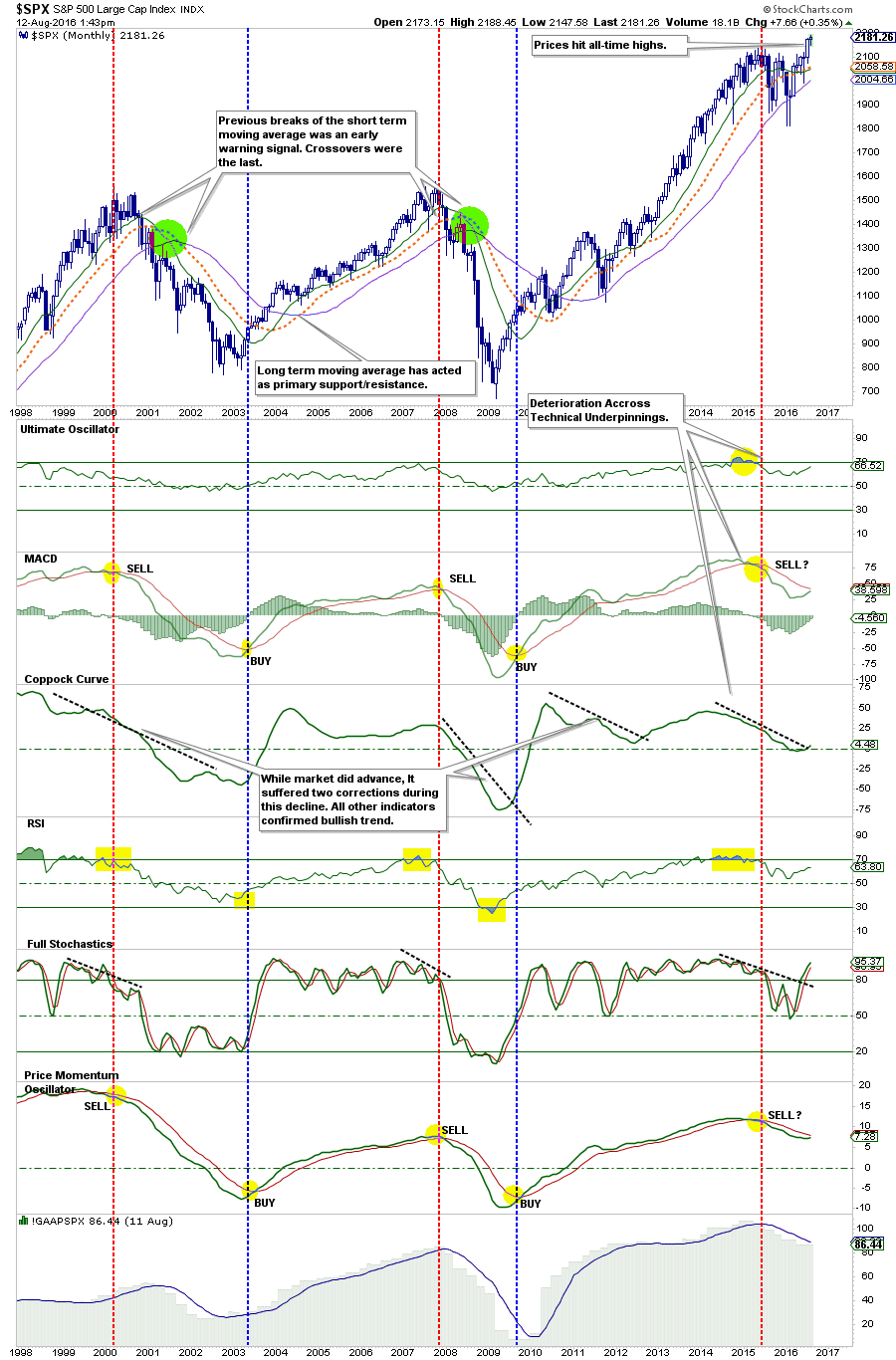

The “big chart” of technical underpinnings clearly suggest that while prices are bullish, the underlying “health” of the market remains weak.

What Can Go Wrong? A Lot!

Unfortunately, several factors could cause an unceremonious change in the market’s direction at any moment. As Doug notes:

“An Abrupt Growth Slowdown. Low U.S. interest rates have pulled forward demand, and from my perch, we’re already seeing ‘Peak Autos’ and ‘Peak Housing.’ I wonder whether U.S. consumer spending’s recent strength is sustainable … or just the last gasp of growth?

A Possible Deeper ‘Earnings Recession.’ Will corporate profit margins get squeezed even further going forward?

An Abrupt Reversal for Stocks. This could ‘just happen’ out of the blue, or it could stem from an exogenous political or geopolitical shock. Or it could follow something else that investors aren’t even thinking about. My concern is that an abrupt change in sentiment or stock prices could ignite a selling stampede from the influential quant community, just as ‘portfolio insurance’ precipitated the October 1987 Wall Street crash.

A Quick Climb in Interest Rates. This could, among other things, curtail mergers and acquisitions and/or stock-repurchase programs.

An Abrupt Rise in Inflation or Inflationary Expectations. This could spark higher interest rates.

A Federal Reserve Policy Mistake. We can never rule this out.

A European Banking Crisis. This could have a “contagion effect” around the world.

Policies that Destabilize Currencies. Again, this is always a possibility.

A Zika Virus Outbreak or Other Health Event. Few investors are even thinking about this.

A Monumental Hacking. A major computer hack of the U.S. banking and investing complex could disrupt everything.

Something Else. We face all sorts of other risks that no one is even considering.”

The Bottom Line

I agree with Doug. The view of “TTID” or “TINA” will likely end very badly for investors over the longer-term time frame. Distortions of price from reality are short-term, emotionally driven, cycles.

With the S&P 500 trading at more than 25x GAAP earnings, 18x non-GAAP profits (one of the largest differentials between GAAP and non-GAAP in history), risk vs. reward is simply not present in the long-term.

However, in the short-term, we must recognize the potential for the markets to remain “irrational” longer than logic would currently dictate. This is why I am cautiously managing portfolio risk and allowing the markets to “tell me” what to do rather than guessing at it.

What happens over the next few days to weeks is really anyone’s guess. The data continues to suggest some sort of corrective action over the next two months (as discussed previously) which will provide a better risk/reward setup for increasing equity exposure in the short-term.

But, over the longer-term time horizon, I am unashamedly bearish as the current detachment between prices and fundamental reality can not last forever.

Eventually, something’s gotta give.

“A bull market lasts until it is over.” – Jim Dines