by Lance Roberts, Clarity Financial

This past week, the markets rallied sharply from last week’s lows sending the “bulls” stampeding into the market with claims the market is back.

“Hold on to your hats, folks.

According to Andrew Adams, a market strategist at Raymond James, there exists a perfect mix of conditions that could send stocks on a ride up, up, and up.

In a note out Thursday, Adams noted that there was a significant shift of investors from the stock market to ‘safer’ assets. Eventually, this move to the sidelines will have to change.“

The problem is that Adams is incorrect about the “cash on the sidelines” theory. As Cliff Asness penned previously:

“Every time someone says, ‘There is a lot of cash on the sidelines,’ a tiny part of my soul dies. There are no sidelines. Those saying this seem to envision a seller of stocks moving her money to cash and awaiting a chance to return. But they always ignore that this seller sold to somebody, who presumably moved a precisely equal amount of cash off the sidelines.

Even though I’ve thrown people who use this phrase a lifeline, I believe that they really do think there are sidelines.

There aren’t. Like any equilibrium concept (a powerful way of thinking that is amazingly underused), there can be a sideline for any subset of investors, but someone else has to be doing the opposite.

Add us all up and there are no sidelines.”

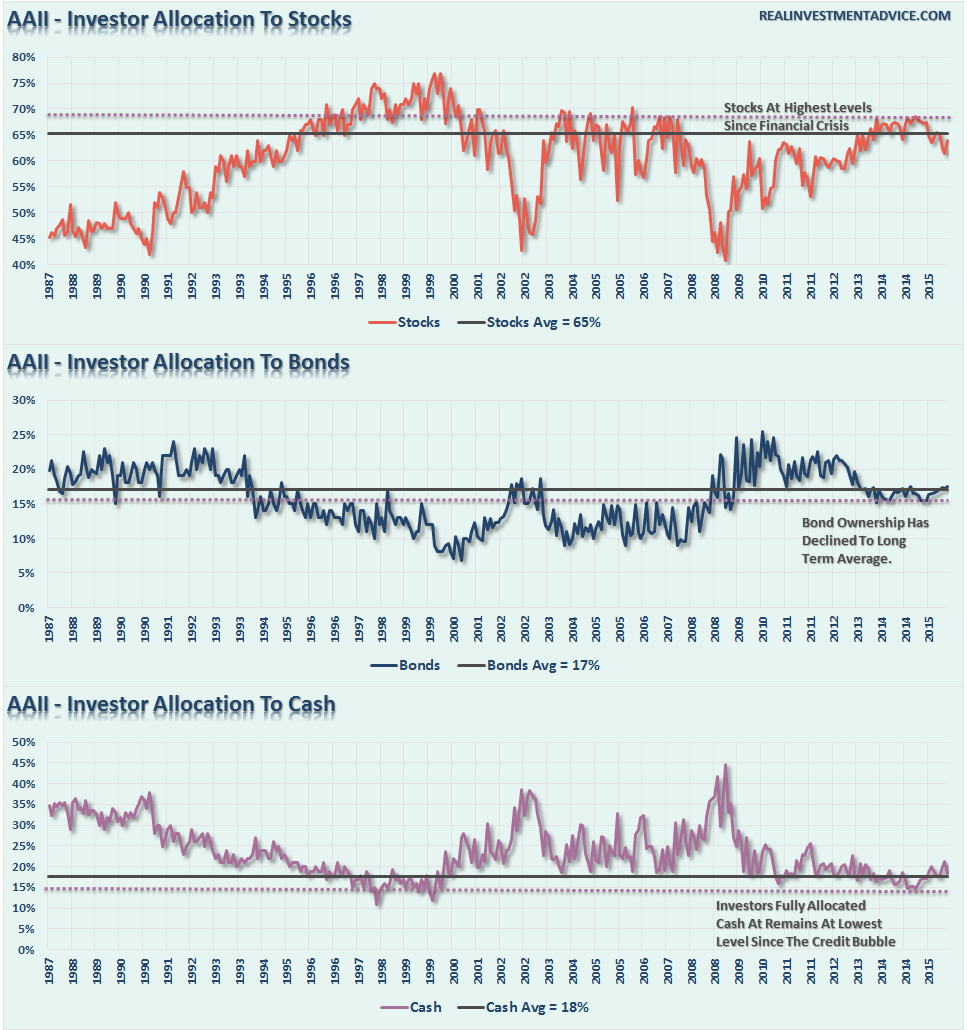

Adams comment would also suggest that investors are sitting primarily in cash and bonds rather than equities. Again, they aren’t.

Jesse Felder also drove home this point last week as well stating:

“Jeremy Siegel, of Stocks For The Long Run fame, was on CNBC this morning:

“I think we’re in the first inning of shifting to dividend-paying stocks,” the finance professor at the University of Pennsylvania’s Wharton School said Tuesday on CNBC’s “Trading Nation.” Even though the Fed may raises [sic] rates this year, “investors are becoming convinced they’re not going to be able to rely on CDs, their bank accounts, or even bonds as a source of income,” and may thus determine that “maybe they’d better turn to stocks,” he said.

Let me get this straight: The professor claims that investors are only just beginning to realize that bonds and cash have no yield thus there is no alternative to putting their money into dividend-paying stocks? In other words, we are only in the “first inning” of TINA (there is no alternative – to stocks)?

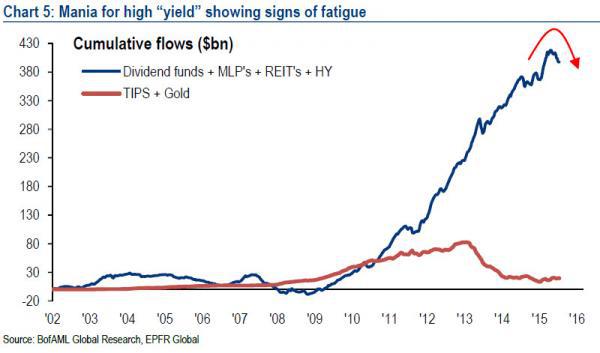

Can someone please do me a favor and show Prof. Siegel the charts below? Because it seems to me investors have been reaching for yield for several years now as a direct response to 7 years of ZIRP (zero interest rate policy).”

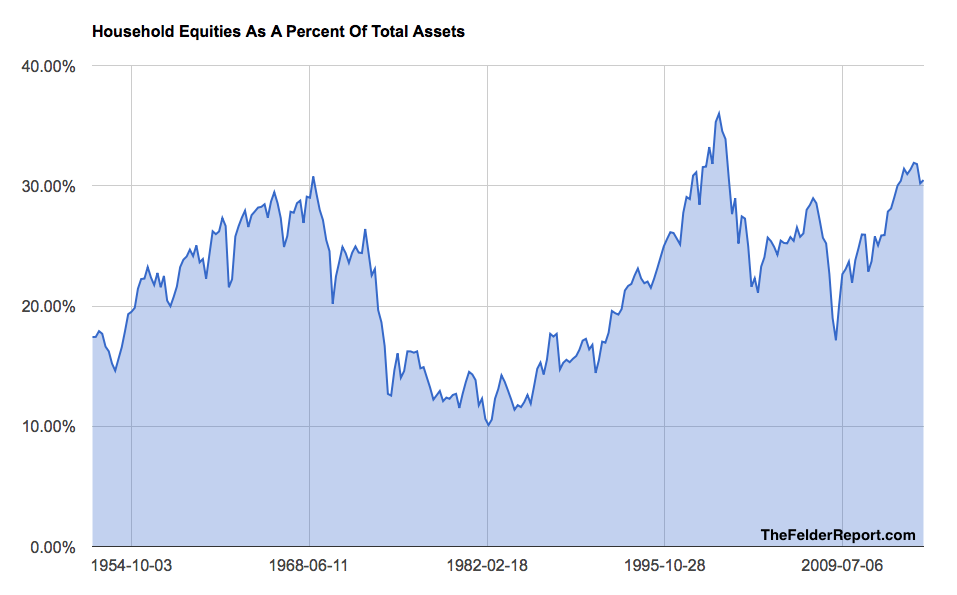

“And after 7 years of reaching for yield, investors now have one of their largest allocations to stocks in history. Only at the height of the dotcom bubble did households have a greater portion of their total financial assets tied up in equities than they did recently.”

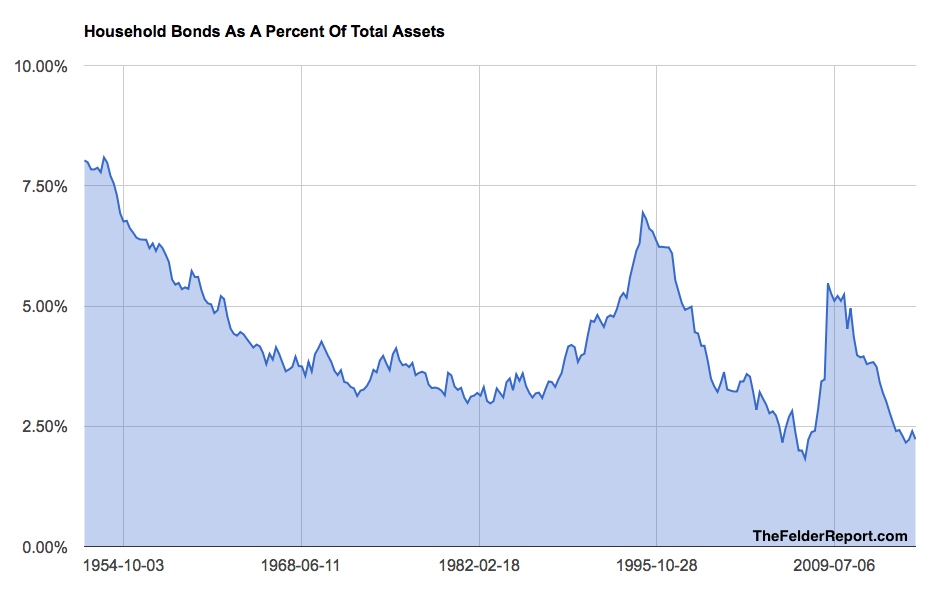

“The difference between today and back then is their allocation to bonds. While investors have ramped up their exposure to stocks, they have shifted almost entirely out of bonds. Even during the dotcom mania investors maintained nearly twice the current allocation to fixed income.”

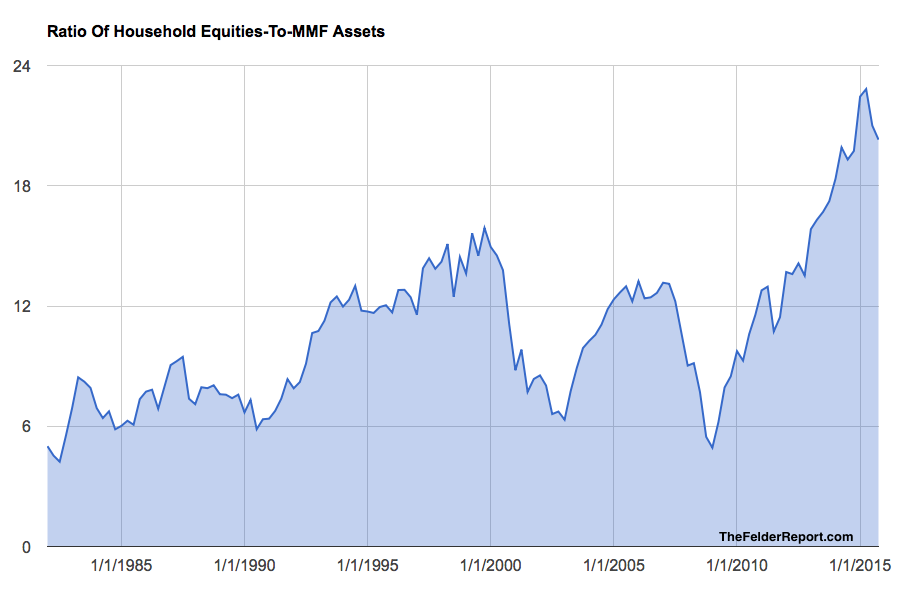

“Finally, when you look at the ratio of equities to money market fund assets it becomes instantly obvious that investors have been embracing the concept of TINA for quite a long time now and to a degree never seen before.”

“So my question for Prof. Siegel is this: If investors have already shifted entirely out of bonds and money market funds, where the hell is this new, massive shift into stocks going to come from? Perchance, you’re just feeling a bit too bullish once again?

On a final note, this large-scale embracing of TINA could very well be the greatest sign of confidence in the stock market we have ever seen. And isn’t that precisely the psychological definition of a mania?”

The problem is that “chasing yield” has become the “defacto” investment by individuals with little concern about the valuation being paid for those dividends. As Warren Buffett once quipped:

“Price is what you pay. Value is what you get.”

Michael Lebowitz of 720 Global Research, addressed this issue this past week stating:

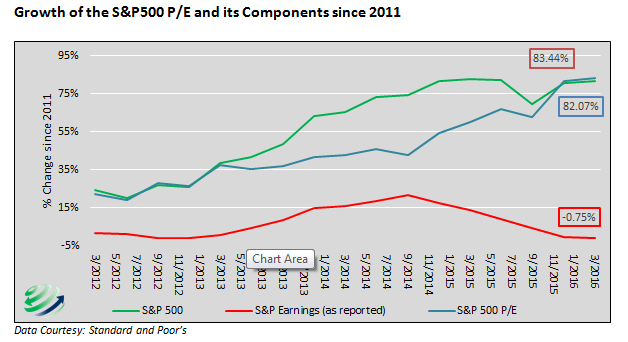

“Since October 1, 2011, the S&P 500 has risen 82% on the heels of strong earnings growth.

Let’s start over. Since October 1, 2011, the S&P 500 has risen 82% on the heels of a 0.75% decline in earnings. The price to earnings ratio over that time period has risen 83%, with price gains contributing 99% to the increase. Prices have risen substantially, while earnings have actually fallen. The chart below highlights the growing gap between earnings and the S&P 500.”

“This chart illustrates that sentiment and momentum, and not fundamental rationale are the factors driving equity markets higher. To justify even a neutral position in equities we would need to see signs of stronger economic growth and revived corporate earnings growth. Unfortunately, the current outlook does not support either of those prerequisites.

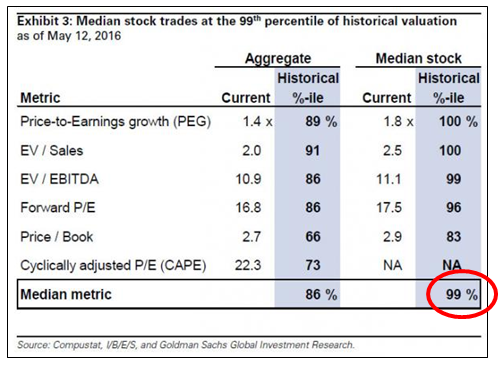

With the information provided above as a backdrop, the following table from Goldman Sachs offers further context on current U.S. equity valuations.”

“We are sympathetic to the idea that there are few alternatives for investors in desperate search of returns, but the risk-reward imbalance in the U.S. equity markets is severe. Stay long patience!”

Are the bulls back?

Based on all the information above – it is quite apparent they never left.

Gray Rhinos & Black Swans

The commentary above is interesting as it relates to the behavioral biases of individual investors. As I wrote previously:

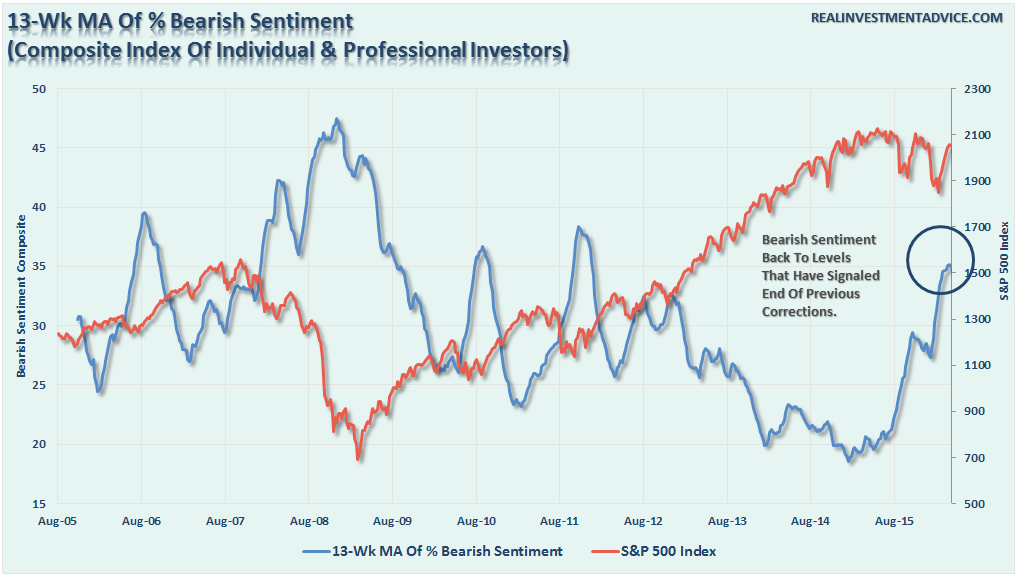

“Investor sentiment (both individual and professional) is currently at levels that are more normally associated with bigger corrections in the market.”

“As noted, the 13-week moving average of bearish sentiment has reached levels currently that are more normally associated with bottoms to corrective processes as seen in 2010 and 2011 when the Federal Reserve intervened with QE2 and Operation Twist.

However, while this surge in bearish sentiment has occurred, which normally denotes a substantial level of fear by investors, there has been no substantial change to actual allocations. (See AAII allocations above)

While stock allocations have fallen modestly, cash and bond allocations have barely budged. This is a far different story than was seen during previous major and intermediate-term corrections in the market.

This suggests, is that while investors are worried about the markets and their investments, they are too afraid to actually make changes to their portfolio as long as Central Banks continue to bail out the markets.”

“Are you afraid of a market crash? Yes. Are you doing anything about it? No.”

Again, it’s back to fundamentals versus expectations. Someone is going to be very wrong.

I remind you of this because Michele Wucker penned an interesting bit of commentary about “Why We Ignore Obvious Dangers.”

“Why do we neglect impending threats? Recent behavioral science from a number of esteemed researchers, including psychologist Daniel Kahneman, behavioral economist Dan Ariely and neuroscientist Tali Sharot, shows that that we are vulnerable to cognitive biases that make us likely to downplay unwelcome information and to be over-optimistic.

Groups of people from similar backgrounds are particularly susceptible to these mind games. Political and financial incentives throw more obstacles in the way. Sometimes we feel powerless to fix a problem, so we don’t even try. Too often, it takes the very real possibility of a calamity – or worse, its aftermath – to prompt us to act.

The consequences of underestimating the danger of a gray rhino can be catastrophic. If there ever was a sign that America needs to rethink the costs and benefits of acting instead of muddling, this is the time.

The zoological term for a group of rhinos is a “crash” – wholly fitting since things are most likely to spin out of control when several gray rhinos come together. Such a crash is exactly what we face. It’s up to us whether we get trampled or get out of the way.“

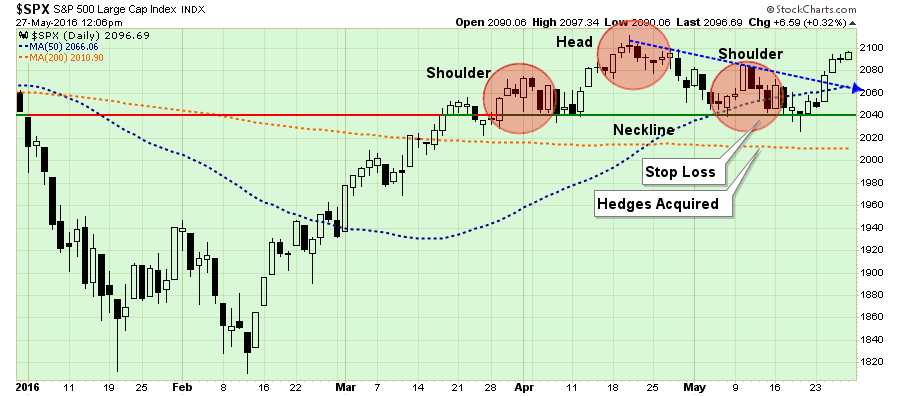

Head & Shoulders Put To Rest…For Now

A couple of week’s ago I discussed the rather clear “head and shoulders” technical pattern that we developing in the market. These patterns often suggest deeper corrections if they complete by breaking neckline support. A “gray rhino” if there ever was one.

The good news is the rally this past week terminated that formation by breaking the very short-term downtrend line as shown below.

While the market did nullify the more bearish short-term pattern, it is important to note that the market has not done much more than that.

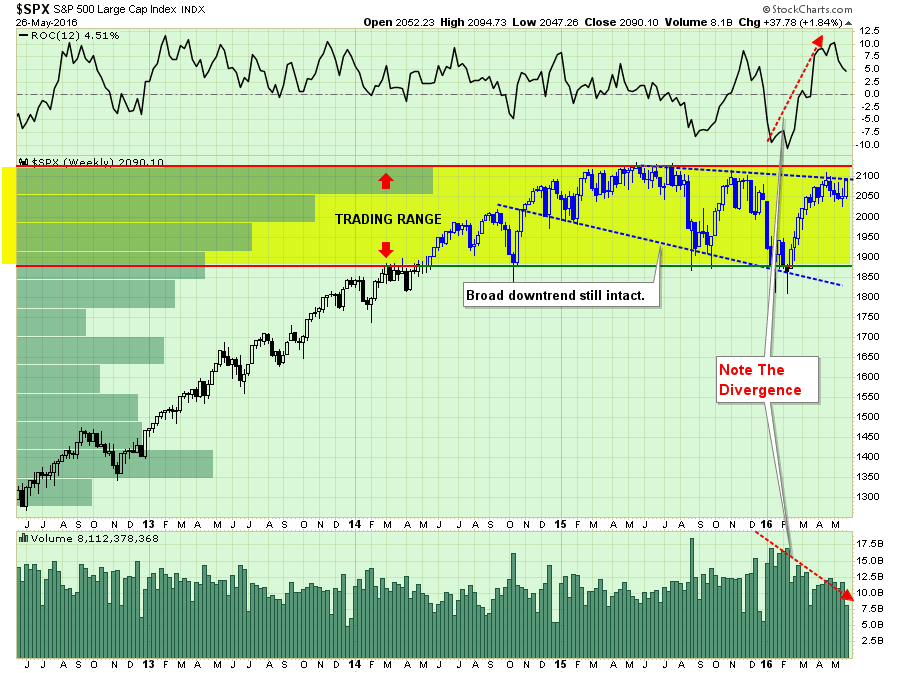

All that really happened last week, as shown in the chart below was an oversold bounce on deteriorating volume confined to an overall market downtrend.

This isn’t a rally that should embolden investors to take on more risk, but rather considering “selling into it” as we head into the seasonally weak period of the year.

But that’s just me.

One note though. The markets have not made a new high within the past year. What does history suggest happens next? 77% of the time it has evolved into a bear market.

On second thought, maybe that should be you too.

“In the short run, the market is a voting machine, but in the long run it is a weighing machine.” – Benjamin Graham