from the St Louis Fed

— this post authored by Miguel Faria-e-Castro, Economist, and Asha Bharadwaj, Research Associate

Policymakers around the world undertook large monetary and fiscal interventions to help stabilize economies in the wake of COVID-19. The main component of the U.S. fiscal policy response was the CARES Act, a $2 trillion package that included many support programs for households and firms.

One of its main components was an additional $600 per week for individuals collecting regular unemployment compensation. This provision expired at the end of July, and its renewal has been a controversial political issue:

- On one hand, many people argue that this measure was essential to prevent a collapse in household spending.

- On the other hand, people have also argued that it has created significant distortions and disincentives to work that may have been hampering the recovery.

In this post, we look at a less-studied effect of this policy: its effect on household delinquency rates. A large increase in household delinquencies can deplete bank capital and cause financial sector disruptions that propagate to the rest of the economy, as we saw in the 2007-08 financial crisis.

Household Delinquencies and Disposable Income

Most economic models posit that household defaults and delinquencies can be attributed to one of two motives:

- Liquidity motives, such as when income is insufficient to cover current interest and principal payments

- Strategic motives, such as when the value of their debt exceeds that of the associated collateral (for example, a house being worth less than the mortgage).

Some recent research argues that liquidity motives are more important than strategic ones (PDF). If liquidity motives are important in determining delinquency rates, then the weekly $600 supplement may have played a large role in stemming or preventing delinquencies and defaults during the last quarter.

To study this, we estimated a simple econometric model for the relationship between bank delinquencies[1] and household disposable income, using data from the first quarter of 2001 to the fourth quarter of 2019. Commercial bank call reports provided information on consumer debt delinquencies at the bank level, which we regressed on aggregate disposable income. A variety of controls – such as debt levels and collateral values (through an index of house prices) – allow us to control for strategic default, and variables such as the cyclical component of gross domestic product (GDP) and the unemployment rate allow us to control for the business cycle. This method provides us with estimates for the elasticity between the average delinquency rate and the cyclical component of disposable income.

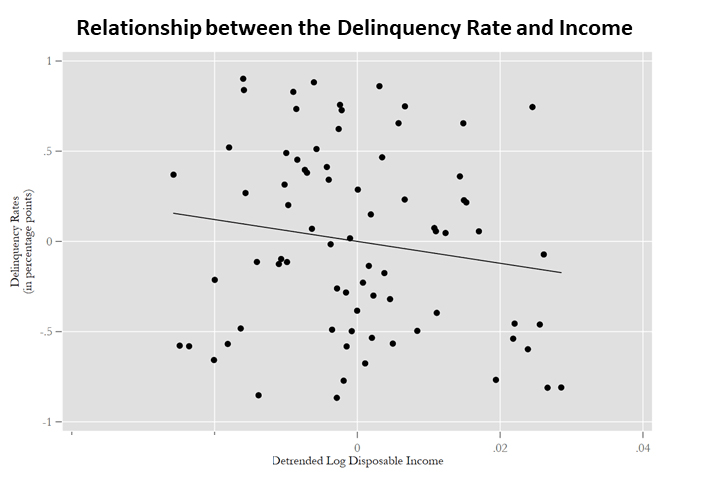

The figure below shows the relationship between average delinquency rates and changes in aggregate disposable income, after controlling for the aforementioned effects. Each point represents a quarter, and it is clear that there is a negative relationship between the two variables.

NOTES: Aggregate disposable income has been detrended using the Hamilton filter. Delinquency rates are reported as averages across all banks in a given quarter, after partialling out the effects of other controls. Data are from the first quarter of 2001 to the fourth quarter of 2019.

SOURCES: Commercial bank call reports, FRED and authors’ calculations.

We found that this elasticity ranged between -0.17 and -0.15. This implies that a 1% increase in disposable income resulted in a decrease in delinquencies of 0.15 to 0.17 percentage points.

The Effects of the CARES Act

As part of the unemployment insurance supplement stipulated by the CARES Act, the federal government spent nearly $171.5 billion on additional unemployment compensation in the second quarter of 2020. We estimated that this increase in unemployment benefits represented a 5% increase in disposable income.

The estimated elasticity between the delinquency rate and disposable income then implies that this increase in disposable income led to an estimated reduction of delinquencies of between 0.71 and 0.76 percentage points. For reference, the average delinquency rate over our sample is 1.6%. To put things in perspective, this is equivalent to a reduction of about $10.7 billion to $11.5 billion in delinquent loans.

It is important to note that this is a simple exercise to measure the association between additional unemployment assistance and delinquencies. It does not consider factors like the labor supply response of individuals to unemployment compensation, which could also have an impact on delinquencies.

In conclusion, the additional unemployment benefits provided by the CARES act has implications not only for the labor market but also for household delinquencies. We found that delinquencies could have been significantly higher in the absence of this relief plan, which could have consequences in terms of financial stability.

Notes and References

- Delinquent loans are defined as loans past due thirty days or more and still accruing interest as well as those in nonaccrual status. They are measured as a percentage of total loans in any given quarter, for a given bank.

Additional Resources

- St. Louis Fed’s COVID-19 resource page

- On the Economy: Housing Distress in the Time of COVID-19

- On the Economy: Three Reasons Why Millennials May Face Devastating Setback from COVID-19

Source

Disclaimer

Views expressed are not necessarily those of the Federal Reserve Bank of St. Louis or of the Federal Reserve System.