Written by rjs, MarketWatch 666

Here are some selected news articles from the week ended 18 July 2020. Part 2 is available here.

Here are some selected news articles from the week ended 18 July 2020. Part 2 is available here.

This is a feature at Global Economic Intersection every Monday evening.

Please share this article – Go to very top of page, right hand side, for social media buttons.

4,340,000 barrels per day of unwanted oil produced in June; drilling of new wells and completions of drilled wells lowest on record

oil prices again ended little changed this week after trading in a fairly narrow range, as a big drop in US crude supplies was offset by an OPEC announcement that they’d begin increasing production in August…after slipping 0.3% to $40.55 a barrel as improving economic data was offset by rising coronavirus cases last week, the contract price of US light sweet crude for August delivery opened 20 cents lower on Monday on a Sunday WHO report of a record daily increase in global coronavirus cases and drifted lower to end down 45 cents at $40.10 a barrel as traders awaited an OPEC meeting that was expected to recommend an increase in oil output…oil prices were down another 2% in early trading on Tuesday on worries that new clampdowns on businesses to stem surging coronavirus cases would threaten the nascent recovery in fuel demand, but recovered to end 19 cents higher at $40.29 a barrel as a report showed that OPEC and its allies had cut production by more than they had agreed to in June…oil prices were expected to plunge on Wednesday as the OPEC+ alliance was poised to boost their oil output by 2 million barrels per day, but instead rose more than 2% on a surprise draw from U.S. crude and product inventories, and then jumped to a four-month high after Trump moved to diffuse building tensions with China, ending 91 cents higher at $41.20 a barrel…but the finalization of the OPEC+ agreement to begin unwinding their deep production cuts hit prices on Thursday, as they fell 45 cents to $40.75 a barrel as the Saudi energy minister said the kingdom was fed up of volunteering and taking on others’ burdens…oil prices slipped another 16 cents to settle at $40.59 per barrel on Friday, as the US had reported a new daily record of new COVID-19 cases on Thursday and as Spain and Australia reported their steepest daily jumps in months, but still managed to hang on to a gain of 4 cents, or barely 0.1% for the week….

natural gas prices, on the other hand, moved lower this week on moderating temperature forecasts and rising natural gas output…after riising 4.1% to $1.805 per mmBTU last week on forecasts for much warmer than normal weather through the end of July, the contract price of natural gas for August delivery fell 6.6 cents, or 3.7% on Monday on rising natural gas output and forecasts for lower air conditioning demand over the next two weeks than had been previously expected…but prices recovered seven-tenths of a cent on a return of hot weather on Tuesday, and then rose 3.2 cents to $1.778 per mmBTU on wednesday as an increase in pipeline exports to Canada and Mexico and increased AC demand kept the amount of gas going into storage lower than usual for this time of year….but natural gas prices still fell 5.5 cents or over 3% to a two-week low despite a bullish storage report on Thursday as gas output rose slowly while LNG exports held near the lowest level since early 2018…gas prices slipped another half-cent on Friday to end the week at $1.718 per mmBTU on forecasts for less hot weather over the next two weeks than had been expected and thus ended the week 4.8% lower than the prior Friday’s close..

the natural gas storage report from the EIA for the week ending July 10th indicated that the quantity of natural gas held in underground storage in the US rose by 45 billion cubic feet to 3,178 billion cubic feet by the end of the week, which left our gas supplies 663 billion cubic feet, or 26.4% greater than the 2,515 billion cubic feet that were in storage on July 10th of last year, and 436 billion cubic feet, or 15.9% above the five-year average of 2,742 billion cubic feet of natural gas that has been in storage as of the 10th of July in recent years….the 45 billion cubic feet that were added to US natural gas storage this week was less than the average 50 billion cubic feet increase that was forecast by analysts polled by S&P Global Platts, and it was well less than the 67 billion cubic feet addition of natural gas to storage during the corresponding week of 2019, and it was also less than the average of 63 billion cubic feet of natural gas that has been added to natural gas storage during the same week over the past 5 years…

The Latest US Oil Supply and Disposition Data from the EIA

US oil data from the US Energy Information Administration for the week ending July 10th indicated that because of a near record drop in our oil imports, we had to pull oil out of our stored commercial supplies of crude oil for the 2nd time in six weeks, and for the 13th time in the past forty-four weeks….our imports of crude oil fell by an average of 1,827,000 barrels per day to an average of 5,567,000 barrels per day, after rising by an average of 1,425,000 barrels per day during the prior week, while our exports of crude oil rose by an average of 156,000 barrels per day to an average of 2,543,000 barrels per day during the week, which meant that our effective trade in oil worked out to a net import average of 3,024,000 barrels of per day during the week ending July 10th, 1,983,000 fewer barrels per day than the net of our imports minus our exports during the prior week…over the same period, the production of crude oil from US wells was reportedly unchanged at 11,000,000 barrels per day, and hence our daily supply of oil from the net of our trade in oil and from well production totaled an average of 14,024,000 barrels per day during this reporting week..

meanwhile, US oil refineries reported they were processing 14,309,000 barrels of crude per day during the week ending July 10th, 36,000 fewer barrels per day than the amount of oil they used during the prior week, while over the same period the EIA’s surveys indicated that a net of 1,052,000 barrels of oil per day were being pulled out of the supplies of oil stored in the US…..so based on that reported & estimated data, this week’s crude oil figures from the EIA appear to indicate that our total working supply of oil from net imports, from storage, and from oilfield production was 768,000 barrels per day more than what our oil refineries reported they used during the week….to account for that disparity between the apparent supply of oil and the apparent disposition of it, the EIA just inserted a (-768,000) barrel per day figure onto line 13 of the weekly U.S. Petroleum Balance Sheet to make the reported data for the average daily supply of oil and the data for the average daily consumption of it balance out, essentially a fudge factor that they label in their footnotes as “unaccounted for crude oil”, thus suggesting an error or errors of that magnitude in the oil supply & demand figures we have just transcribed…however, since the media usually treats these weekly EIA figures as gospel and since these numbers often drive oil pricing and hence decisions to drill for oil, we’ll continue to report them, just as they’re watched & believed as accurate by most everyone in the industry….(for more on how this weekly oil data is gathered, and the possible reasons for that “unaccounted for” oil, see this EIA explainer)….

further details from the weekly Petroleum Status Report (pdf) indicate that the 4 week average of our oil imports fell to an average of 6,368,000 barrels per day last week, which was 10.2% less than the 7,094,000 barrel per day average that we were importing over the same four-week period last year….the 1,052,000 barrel per day net reduction of our total crude inventories came as 1,070,000 barrels per day were being pulled out of our commercially available stocks of crude oil while 18,000 barrels per day were being added to our Strategic Petroleum Reserve….this week’s crude oil production was reported to be unchanged at 11,000,000 barrels per day even though the rounded estimate of the output from wells in the lower 48 states fell by 100,000 barrels per day to 10,500,000 barrels per day because a 59,000 barrel per day increase in Alaska’s oil production to 457,000 barrels per day was enough to add 100,000 barrels per day to the rounded national total….last year’s US crude oil production for the week ending July 12th was rounded to 12,000,000 barrels per day, so this reporting week’s rounded oil production figure was about 8.3% below that of a year ago, yet still 30.5% more than the interim low of 8,428,000 barrels per day that US oil production fell to during the last week of June of 2016…

meanwhile, US oil refineries were operating at 78.1% of their capacity while using 14,309,000 barrels of crude per day during the week ending July 10th, up from 77.5% of capacity during the prior week, but excluding the 2005, 2008, and 2017 hurricane-related refinery interruptions, still one of the lowest refinery utilization rates of the last thirty years…hence, the 14,309,000 barrels per day of oil that were refined this week were still 17.1% fewer barrels than the 17,267,000 barrels of crude that were being processed daily during the week ending July 12th, 2019, when US refineries were operating at 94.4% of capacity….

even with the small decrease in the amount of oil being refined, gasoline output from our refineries was still higher, increasing by 50,000 barrels per day to 8,095,000 barrels per day during the week ending July 10th, after our refineries’ gasoline output had increased by 140,000 barrels per day over the prior week… however, since our gasoline production is still recovering from a multi-year low, this week’s gasoline output was still 7.7% lower than the 9,855,000 barrels of gasoline that were being produced daily over the same week of last year….at the same time, our refineries’ production of distillate fuels (diesel fuel and heat oil) increased by 104,000 barrels per day to 4,860,000 barrels per day, after our distillates output had increased by 122,000 barrels per day over the prior week…but even after this week’s increase in distillates output, our distillates’ production was still 9.3% less than the 5,361,000 barrels of distillates per day that were being produced during the week ending July 12th, 2019….

even with the increase in our gasoline production, our supply of gasoline in storage at the end of the week decreased for the 8th time in 12 weeks and for the 16th time in 24 weeks, falling by 3,147,000 barrels to 248,535,000 barrels during the week ending July 10th, after our gasoline supplies had decreased by 4,839,000 barrels over the prior week…our gasoline supplies decreased this week even though the amount of gasoline supplied to US markets decreased by 118,000 barrels per day to 8,648,000 barrels per day because our imports of gasoline fell by 236,000 barrels per day to 493,000 barrels per day and because our exports of gasoline rose by 77,000 barrels per day to 601,000 barrels per day….but even after this week’s inventory decrease, our gasoline supplies were still 6.8% higher than last July 12th’s gasoline inventories of 232,752,000 barrels, and roughly 7% above the five year average of our gasoline supplies for this time of the year…

likewise, even with the increase in our distillates production, our supplies of distillate fuels decreased for the fourteenth time in 26 weeks and for the 24th time in 41 weeks, falling by 453,000 barrels to 176,809,000 barrels during the week ending July 10th, after our distillates supplies had increased by 3,135,000 barrels over the prior week….our distillates supplies fell this week because the amount of distillates supplied to US markets, an indicator of our domestic demand, rose by 673,000 barrels per day to 3,692,000 barrels per day, even as our exports of distillates fell by 28,000 barrels per day to 1,332,000 barrels per day and our imports of distillates rose by 27,000 barrels per day to 99,000 barrels per day….but even after this week’s inventory decrease, our distillate supplies at the end of the week were still 29.8% above the 136,203,000 barrels of distillates that we had in storage on July 12th, 2019, and about 26% above the five year average of distillates stocks for this time of the year…

finally, with the big drop in our oil imports, our commercial supplies of crude oil in storage fell for the 5th time in twenty-five weeks and for the 17th time in the past year, decreasing by 7,493,000 barrels, from 539,181,000 barrels on July 3rd to 531,688,000 barrels on July 10th….but even after that decrease, our our commercial crude oil inventories were around 17% above the five-year average of crude oil supplies for this time of year, and more than 57% above the prior 5 year (2010 – 2014) average of our crude oil stocks for the second weekend of July, with the disparity between those comparisons arising because it wasn’t until early 2015 that our oil inventories first topped 400 million barrels….since our crude oil inventories have generally been rising since September of 2018, except for during last summer, after generally falling until then through most of the prior year and a half, our crude oil supplies as of July 10th were 16.6% above the 455,876,000 barrels of oil we had in commercial storage on July 12th of 2019, 29.3% more than the 411,084,000 barrels of oil that we had in storage on July 13th of 2018, and 8.4% above the 490,623,000 barrels of oil we had in commercial storage on July 14th of 2017…

OPEC’s Monthly Oil Market Report

Tuesday of this past week saw the release of OPEC’s July Oil Market Report, which covers OPEC & global oil data for June, and hence it gives us a picture of the global oil supply & demand situation during the second month of the two month agreement between OEC, the Russians, and other oil producers to cut production by 9.7 million barrels a day from an elevated October 2018 baseline….again, we should caution that estimating oil demand while many countries were just restarting their economies after a month or two of lockdown is pretty speculative, and hence the demand figures we’ll be reporting this month should again be considered as having a much larger margin of error than we’d normally expect from this report..

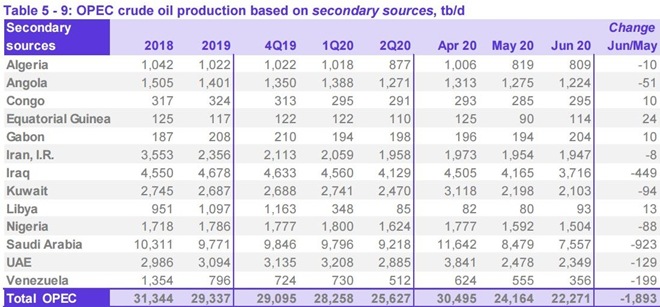

the first table from this monthly report that we’ll review is from the page numbered 49 of this month’s report (pdf page 58), and it shows oil production in thousands of barrels per day for each of the current OPEC members over the recent years, quarters and months, as the column headings indicate…for all their official production measurements, OPEC uses an average of estimates from six “secondary sources”, namely the International Energy Agency (IEA), the oil-pricing agencies Platts and Argus, the U.S. Energy Information Administration (EIA), the oil consultancy Cambridge Energy Research Associates (CERA) and the industry newsletter Petroleum Intelligence Weekly, as a means of impartially adjudicating whether their output quotas and production cuts are being met, to thus avert any potential disputes that could arise if each member reported their own figures…

as we can see from the above table of oil production data, OPEC’s oil output was cut by 1,893,000 barrels per day to 22,271,000 barrels per day during June, from their revised May production total of 24,164,000 barrels per day…however that May output figure was originally reported as 24,195,000 barrels per day, which means that OPEC’s May production was revised 31,000 barrels per day lower with this report, and hence June’s production was, in effect, a 1,924,000 barrel per day decrease from the previously reported OPEC production figures (for your reference, here is the table of the official May OPEC output figures as reported a month ago, before this month’s revisions)…

from the above table, we can also see that production decreases of 923,000 barrels per day from the Saudis, 449,000 barrels per day from Iraq, 199,000 barrels per day from Venezuela, and 129,000 barrels per day from the Emirates accounted for the lion’s share of the May decrease, even as several other OPEC producers also made further production cuts…to facilitate understanding how each of the OPEC members have been adhering to their latest production cut agreement, we’ll next include a table which shows the October 2018 reference production for each of the OPEC members (as well as other producers party to the mid-April agreement), as well as the production level each of those producers was expected to cut their output to….

the above table was taken from an article at Zero Hedge, and it shows the oil production baseline in thousands of barrel per day off of which each of the oil producers will cut from in the first column, a number which is based on each of the producer’s October 2018 output, ie., a date before the past year’s and last quarter’s output cuts took effect; the second column shows how much each participant has committed to cut in thousands of barrel per day, which is 23% of the October 2018 baseline for all participants except for Mexico, while the last column shows the production level each participant has agreed to after that 23% cut…note that sanctioned OPEC members Iran and Venezuela and war-torn Libya are exempt from these cuts…

with a net 8,224,000 barrels per day decrease in their production since April, it appears that OPEC has far exceeded the 6,084,000 barrels per day they had committed to cut…however, the baseline for the agreed to May and June cuts is OPEC’s production of October 2018, and the 6,300,000 barrels per day drop in their production represents the output change since April, so we can’t really compare the two…moreover, production of some of the OPEC members is still above their target level…for instance, Iraq had committed to cut their production by 1,061,000 barrels per day from their October 2018 level and only produce 3,592,000 barrels per day in June, but they’ve only cut their production by 789,000 barrels per day over May and June, and thus produced 3,716,000 barrels per day, 124,000 barrels per day more than they were supposed to…

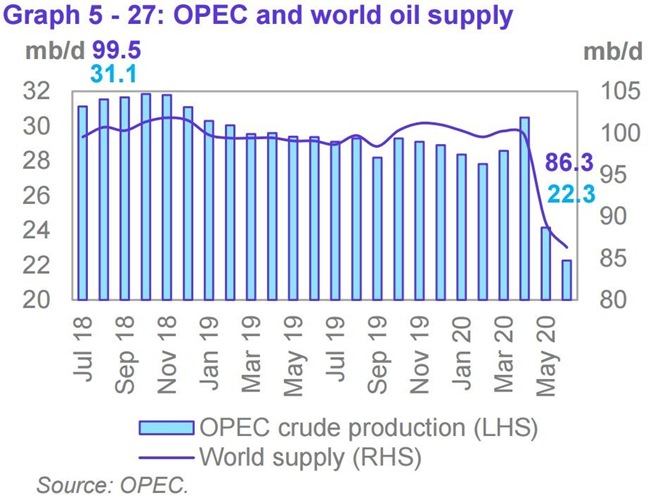

the next graphic from this month’s report that we’ll include shows us both OPEC and world oil production monthly on the same graph, over the period from July 2018 to June 2020, and it comes from page 50 (pdf page 59) of the July OPEC Monthly Oil Market Report….on this graph, the cerulean blue bars represent monthly OPEC oil production in millions of barrels per day as shown on the left scale, while the purple graph represents global oil production in millions of barrels per day, with the metrics for global output shown on the right scale….

including the 1,893,000 barrel per day cut in OPEC’s production from what they produced a month earlier, OPEC’s preliminary estimate indicates that total global oil production decreased by a rounded 2.95 million barrels per day to average 86.29 million barrels per day in June, a reported decrease which apparently came after May’s total global output figure was revised higher by 350,000 barrels per day from the 89.89 million barrels per day of global oil output that was reported a month ago, as non-OPEC oil production fell by a rounded 1,060,000 barrels per day in June after that revision, with lower oil production from the OECD oil producers accounting for 880,000 barrels per day of the non-OPEC output decrease in June…with the decrease in June’s global output, the 86.29 million barrels of oil per day produced globally in June were 12.19 million barrels per day, or 12.4% less than the revised 98.48 million barrels of oil per day that were being produced globally in May a year ago, the 6th month of OPECs first round of production cuts (see the July 2019 OPEC report (online pdf) for the originally reported May 2019 details)…with this month’s drop in OPEC’s output, their June oil production of 22,271,000 barrels per day fell to 25.8% of what was produced globally during the month, down from their 27.1% share in May, and the 30.5% share they contributed in April…OPEC’s June 2019 production, which included 515,000 barrels per day from former OPEC member Ecuador, was reported at 29,855,000 barrels per day, which means that the 13 OPEC members who were part of OPEC last year produced 7,069,000, or 24.1% fewer barrels per day of oil in June than what they produced a year ago, when they accounted for 30.4% of global output…

Even with the big drop in OPEC’s and global oil output that we’ve seen in this report, there was still a big surplus in the amount of oil being produced globally during the month, as this next table from the OPEC report will show us…

the above table came from page 26 of the June OPEC Monthly Oil Market Report (pdf page 35), and it shows regional and total oil demand estimates in millions of barrels per day for 2019 in the first column, and OPEC’s estimate of oil demand by region and globally quarterly over 2020 over the rest of the table…on the “Total world” line in the third column, we’ve circled in blue the figure that’s relevant for June, which is their estimate of global oil demand during the second quarter of 2020…

OPEC is estimating that during the 2nd quarter of this year, all oil consuming regions of the globe have been using an average of 81.95 million barrels of oil per day, which is a 650,000 barrels per day upward revision from the 81.30 million barrels of oil per day they were estimating for the 2nd quarter a month ago (circled in green), largely reflecting coronavirus related demand destruction….meanwhile, as OPEC showed us in the oil supply section of this report and the summary supply graph above, OPEC and the rest of the world’s oil producers were still producing 86.29 million barrels per day during June, which would imply that there was a surplus of around 4,340,000 barrels per day in global oil production in June, still 5.3% greater than the demand estimated for the month…

in addition to figuring the June surplus, the upward revision of 350,000 barrels per day to May’s global output that’s implied in this report, combined with the 650,000 barrels per day upward revision to 2nd quarter demand that we’ve circled in green means that the 8,590,000 barrels per day global oil output surplus we had figured for May would now have to be revised to a surplus of 8,290,000 barrels per day….at the same time, the surplus of 17,690,000 barrels per day that we had previously figured for April, in light of that 650,000 barrels per day upward revision to 2nd quarter demand, would have to be revised to a surplus of 17,040,000 barrels per day…

Also note that in green we’ve also circled an upward revision of 20,000 barrels per day to first quarter demand….that means that the record global oil surplus of 18,068,000 barrels per day we had previously figured for March would have to be revised to a global oil surplus of 18,048,000 barrels per day…similarly, the 2,180,000 barrel per day global oil production surplus we had for February would now be a 2,160,000 barrel per day global oil output surplus, and the 1,210,000 barrel per day global oil output surplus we had for January would be revised to a 1,190,000 barrel per day oil output surplus.. but even after those revisions, it’s obvious the world’s oil producers have produced a lot of oil this year that no one wanted..

This Week’s Rig Count

the US rig count fell for the 19th week in a row during the week ending July 17th, and is now down by 68.1% over that nineteen week period….Baker Hughes reported that the total count of rotary rigs running in the US decreased by 5 rigs to 253 rigs this past week, which again was the fewest active rigs in Baker Hughes records going back to 1940 and 151 fewer rigs than the all time low prior to this year, and was also down by 701 rigs from the 954 rigs that were in use as of the July 19th report of 2019, and 1,676 fewer rigs than the shale era high of 1,929 drilling rigs that were deployed on November 21st of 2014, the week before OPEC began to flood the global oil market in their first attempt to put US shale out of business….

the number of rigs drilling for oil decreased by 1 rig to 180 oil rigs this week, after falling by 4 oil rigs the prior week, leaving oil rig activity at its lowest since June 5th, 2009, which was also 599 fewer oil rigs than were running a year ago, and less than an eighth of the recent high of 1609 rigs that were drilling for oil on October 10th, 2014….at the same time, the number of drilling rigs targeting natural gas bearing formations fell by 4 rig to 71 natural gas rigs, which was the least natural gas rigs running in at least 80 years, and down by 103 natural gas rigs from the 174 natural gas rigs that were drilling a year ago, and was less than a twentieth of the modern era high of 1,606 rigs targeting natural gas that were deployed on September 7th, 2008…in addition to those rigs drilling for oil & gas, two rigs classified as ‘miscellaneous’ continued to drill this week; one on the big island of Hawaii, and one in Sonoma County, California… a year ago, there was just one such “miscellaneous” rigs deployed…

the Gulf of Mexico rig count was unchanged at 12 rigs this week, with 10 of those rigs drilling for oil in Louisiana’s offshore waters and two of them drilling for oil offshore from Texas…that was 13 fewer rigs than the 25 rigs drilling in the Gulf a year ago, when 24 rigs were drilling offshore from Louisiana and one rig was operating in Texas waters…while there are no rigs operating off other US shores at this time, a year ago there was also a rig deployed in the Cook Inlet offshore from Alaska, so this week’s national offshore count is down by 14 from the national offshore rig count of 26 a year ago

the count of active horizontal drilling rigs decreased by 5 rigs to 215 horizontal rigs this week, which was the fewest horizontal rigs drilling in the US since November 18th, 2005, and hence is a new 14 1/2 year low for horizontal drilling…it was also 614 fewer horizontal rigs than the 829 horizontal rigs that were in use in the US on July 19th of last year, and less than a sixth of the record of 1372 horizontal rigs that were deployed on November 21st of 2014…in addition, the vertical rig count was down by four to 15 vertical rigs this week, and those were also down by 41 from the 56 vertical rigs that were operating during the same week of last year…on the other hand, the directional rig count rose by 4 rigs to 23 directional rigs this week, but those were also still down by 46 from the 69 directional rigs that were in use on July 19th of 2019….

the details on this week’s changes in drilling activity by state and by major shale basin are shown in our screenshot below of that part of the rig count summary pdf from Baker Hughes that gives us those changes…the first table below shows weekly and year over year rig count changes for the major oil & gas producing states, and the table below that shows the weekly and year over year rig count changes for the major US geological oil and gas basins…in both tables, the first column shows the active rig count as of July 17th, the second column shows the change in the number of working rigs between last week’s count (July 10th) and this week’s (July 17th) count, the third column shows last week’s July 10th active rig count, the 4th column shows the change between the number of rigs running on Friday and the number running before the same weekend of a year ago, and the 5th column shows the number of rigs that were drilling at the end of that reporting week a year ago, which in this week’s case was the 19th of July, 2019…

there were a few more changes in drilling activity this week when compared with the near stagnation of recent weeks, but wtih just three additions, it continues to suggest that prices are still not high enough to encourage the addition of many new rigs to the field…checking the rig counts in the Texas part of Permian basin, we find that one rig was shut down in Texas Oil District 8, or the core Permian Delaware, and another rig was shut down in Texas Oil District 7C or the southern Permian Midland…since the overall Permian basin rig count was down by just 1 rig nationally, that means that the rig that was added in New Mexico would have been set up to drill in the western Permian Delaware, offsetting the Texas decrease…elsewhere in Texas, there was a rig added in Texas Oil District 1, but there was also a rig shut down in Texas Oil District 3, which are both part of the region we associate with activity in the Eagle Ford shale, which stretches in a relatively narrow band through the southeastern part of the state and touches on four Oil Districts…since the Eagle Ford shows an increase of two rigs, that means that at least one more Eagle Ford rig was added in one of those districts, while a rig that wasn’t targetting the Eagle Ford was shut down at the same time…in addition, a rig was also shut down in Texas Oil District 7B, which would account for the rig rpulled out of the Barnett shale in the area south of Dallas-Ft Worth….that rig stacked in the Barnett shale had been targeting natural gas, as was the rig that was shut down in Louisiana’s Haynesville, and the two rigs that were stacked in Ohio’s Utica shale, thus accounting for the decrease of four natural gas rigs nationally…at the same time, the shutdown of a natural rig that had been drilling in Pennsylvania’s Marcellus was offset by the addition of a natural rig in West Virginia’s Marcellus, leaving the total Marcellus shale count unchanged…

DUC well report for June

Monday of this past week saw the release of the EIA’s Drilling Productivity Report for July, which includes the EIA’s June data for drilled but uncompleted oil and gas wells in the 7 most productive shale regions….for the 2nd time in the past sixteen months, this report showed an increase in uncompleted wells nationally in June, as both the drilling of new wells and completions of drilled wells decreased, but completions decreased by almost twice as much…..for the 7 sedimentary regions covered by this report, the total count of DUC wells increased by 35 wells, rising from 7,624 DUC wells in May to 7,659 DUC wells in June, which was still 10.2% fewer DUCs than the 8,530 wells that had been drilled but remained uncompleted as of the end of June of a year ago…this month’s DUC decrease occurred as 326 wells were drilled in the 7 regions that this report covers (representing 87% of all U.S. onshore drilling operations) during June, down by 89 from the 417 wells that were drilled in May and the lowest number of wells drilled in the history of this report, while 291 wells were completed and brought into production by fracking, a decrease of 170 well completions from the 461 completions seen in May, and down by 78.2% from the 1,346 completions seen in June of last year, and also the lowest number of completions in one month since completions have been reported by the EIA….at the June completion rate, the 7,659 drilled but uncompleted wells left at the end of the month represents a 26.3 month backlog of wells that have been drilled but are not yet fracked, up from the 16.5 month DUC well backlog of a month ago, with a recognition that this normally indicative backlog ratio is being skewed by record low completions…

oil producing regions saw a net DUC well increase in June, while natural gas producing regions still saw a modest net DUC well decrease, even as some basins went against that trend….the number of uncompleted wells remaining in the Permian basin of west Texas and New Mexico increased by 49, from 3,439 DUC wells at the end of May to 3,488 DUCs at the end of June, as 150 new wells were drilled into the Permian, while 101 wells in the region were being fracked….at the same time, DUC wells in the Bakken of North Dakota increased by 7, from 875 DUC wells at the end of May to 882 DUCs at the end of June, as 20 wells were drilled into the Bakken in June, while 13 of the drilled wells in that basin were being fracked…in addition, the drilled but uncompleted well count in the Niobrara chalk of the Rockies’ front range increased by 2 to 452, as 23 Niobrara wells were drilled in June while 21 Niobrara wells were completed… on the other hand, there was a decrease of 6 DUC wells in the Eagle Ford of south Texas, from 1,301 DUC wells at the end of May to 1,295 DUCs at the end of June, as 35 wells were drilled in the Eagle Ford during June, while 41 already drilled Eagle Ford wells were completed…similarly, DUCs in the Oklahoma Anadarko decreased by 7, falling from 717 at the end of May to 710 DUC wells at the end of June, as 10 wells were drilled into the Anadarko basin during June, while 17 Anadarko wells were being fracked….

among the natural gas producing regions, the drilled but uncompleted well count in the Appalachian region, which includes the Utica shale, fell by 11 wells, from 579 DUCs at the end of May to 568 DUCs at the end of June, as 59 wells were drilled into the Marcellus and Utica shales during the month, while 70 of the already drilled wells in the region were fracked….on the other hand, the natural gas producing Haynesville shale of the northern Louisiana-Texas border region saw their uncompleted well inventory increase by 1 to 264, as 29 wells were drilled into the Haynesville during June, while 28 of the already drilled Haynesville wells were fracked during the same period….thus, for the month of June, DUCs in the five major oil-producing basins tracked by in this report (ie., the Anadarko, Bakken, Niobrara, Permian, and Eagle Ford) increased by a net of 45 wells to 6,827 wells, while the uncompleted well count in the natural gas basins (the Marcellus, Utica, and the Haynesville) decreased by 10 wells to 832 wells, although as this report notes, once into production, more than half the wells drilled nationally will produce both oil and gas…

UTICA SHALE WELL ACTIVITY AS OF JULY 11 –

- DRILLED: 143 (143 as of July 4)

- DRILLING: 110 (111)

- PERMITTED: 501 (500)

- PRODUCING: 2,518 (2,518)

- TOTAL: 3,272 (3,272)

No horizontal permits were issued during the week that ended July 11, and 6 rigs were operating in the Utica Shale. TOP COUNTIES BY NUMBER OF PERMITS:

- 1. BELMONT: 691 (691 as of July 4)

- 2. CARROLL: 530 (530)

- 3. HARRISON: 524 (524)

- 4. MONROE: 438 (438)

- 5. JEFFERSON: 283 (283)

- 6. GUERNSEY: 280 (280)

Harvest Oil selling eastern Ohio wells – Harvest Oil has decided to sell its holding in Appalachian Basin, primarily on eastern Ohio. The company formed two years ago after the bankruptcy of EV Energy Partners. Harvest Oil & Gas, based in Houston, has struck a deal to sell its Appalachian Basin holdings and leave the region. The $20.5 million deal is set to close in August and the buyer hasn’t been identified. The buyer is set to pay $14.5 million in cash and use a $6 million note to cover the balance. All of the assets are in the Utica Shale in eastern Ohio, the company said. Harvest said it intends to evaluate the process of winding-up and of returning capital to its shareholders in the event the sale and other contemplated asset divestitures are completed. This evaluation depends on an analysis of net cash available for distribution to stockholders and the amount of net cash needed to satisfy ongoing liabilities during the process. Harvest was previously EV Energy Partners, which filed bankruptcy and reorganized in April 2018. Two months later it emerged as Harvest Oil & Gas.

Daelim Cites Covid-19 in Dropping Stake in Ohio Ethane Cracker – PTT Global Chemical pcl has lost its equity partner in a multi-billion dollar ethane cracker proposed for southeast Ohio. Daelim Chemical USA dropped its stake, citing the Covid-19 pandemic’s impact on the project timeline and the global economy’s impact on its investment plans. PTT affiliate PTTGC America LLC said it would move ahead with the cracker and look for another partner as Daelim aids in the transition. Earlier this year, the companies said a final investment decision (FID) would likely be delayed because of market volatility caused by the coronavirus. It wasn’t the first time an FID for the project has been postponed, but before the outbreak the companies expected to make a decision by the end of June. They said Tuesday a decision on sanctioning wasn’t likely for another six to nine months. PTT has been at work on the facility since 2015. It partnered with Daelim, a South Korean conglomerate, in 2018 to conduct a feasibility study and secure funding for the project, which would be located in the heart of the Utica Shale in Belmont County. “The Ohio petrochemical facility continues to be a top priority for PTTGC America,” said CEO Toasaporn Boonyapipat. “We are in the process of seeking a new partner whilst working toward a final investment decision. We look forward to making an announcement by the end of this year or early next year on this transformative project for the Ohio Valley region.” The first phase of site preparation and engineering work has been completed, with other demolition jobs remaining around the site on the Ohio River. All of the nearly 500 acres required for the plant have also been purchased, and Ohio has contributed more than $70 million in revitalization and economic development grants and loans. The plant, which has secured all major regulatory approvals, would use six ethane cracking furnaces and manufacture ethylene, high-density polyethylene and linear low-density polyethylene, which are used in plastics and chemical manufacturing. It would be similar in size to another cracker underway by Royal Dutch Shell plc in nearby western Pennsylvania that would consume about 100,000 b/d of ethane.

Chesapeake bankruptcy freezes royalty lawsuit – – A lawsuit over Chesapeake Energy’s royalty payments to Ohio landowners is on hold after the company’s recent bankruptcy filing. The class action lawsuit, filed in 2015 by a group of Columbiana County landowners, claimed damages of at least $30 million on behalf of 224 landowners. It is before a federal appeals court. With the bankruptcy filing, “the odds of getting any money out of Chesapeake are very long indeed,” said Dennis E. Murray Jr., an attorney for the landowners. But claims remain against other defendants in the case, and a favorable appeals court ruling could help the same landowners in their lawsuit against the company that purchased Chesapeake’s Ohio assets. Chesapeake pioneered the practice of drilling and fracking large horizontal wells in Ohio’s Utica and Marcellus shales. But the Oklahoma City-based company borrowed billions of dollars as it drilled hundreds of new oil and natural gas wells. The situation became untenable last month in the face of persistently low oil and natural gas prices, and Chesapeake filed June 28 for Chapter 11 bankruptcy. The company has said its restructuring plan will eliminate $7 billion in debt, but has not said how long the process will take. Chesapeake cut its Ohio ties in 2018 when it sold its assets, including a regional office building in Louisville, to Encino Acquisition Partners for $2 billion. EAP is a partnership between the Canada Pension Plan Investment Board and Encino Energy, a private oil and gas company based in Houston. But Chesapeake – along with French energy giant Total, and Jamestown Resources and Pelican Energy, two companies connected to late Chesapeake founder Aubrey McClendon – were being sued in federal court by Ohio landowners who said the companies underpaid royalties.

Utica and Marcellus Shale condensate prices plunge – Pittsburgh Post-Gazette – Prices for Marcellus and Utica shale condensate fell below zero this week as collapsing demand for oil and gasoline pushed specialty grades out of the market. Ergon Oil Purchasing’s price for Marcellus and Utica condensate was a penny per barrel on Monday and Tuesday before dropping to -$0.69 on Wednesday. The price rebounded Thursday to $4.32, but it was still down 91% from the start of the year. Condensate is an ultra-light liquid hydrocarbon produced along with natural gas from some shale wells. It is not as valuable as oil, but prices for the two commodities tend to rise and fall together. Between 2012 and 2014 – when oil prices were high and gas prices were low – condensate and natural gas liquids buoyed producers focused on the liquids-rich areas of the Marcellus and Utica shales in Western Pennsylvania and Ohio, said Tony Scott, managing director of analytics at BTU Analytics.Condensate at $50 a barrel, as it was before the recent collapse, “goes a long way to making those wells economic at the type of gas prices we are seeing today,” he said. Now, regional natural gas prices are still “very weak” and the condensate premium has evaporated. Jesse Mercer, senior director of crude oil markets at Enverus, said it “makes sense that Utica condensate is pricing at next to nothing right now.”The condensate is mostly used in making gasoline. Demand for transportation fuels is down dramatically amid the global economic shutdown associated with COVID-19, as cars and airplanes sit parked.”Refiners are concerned about running out of storage capacity for all the unwanted gasoline, so they are shunning grades that make a lot of gasoline,” he said.”In this crisis, nobody wants a grade that makes none of the stuff you want and only the stuff you don’t have room to store.” In December 2019, the most recent month available, Pennsylvania, Ohio and West Virginia produced 150,000 barrels of oil and condensate per day, according to the U.S. Energy Information Administration. All oil and condensate produced in the three states is light, but Ergon defines Marcellus and Utica condensate as the lightest in that range.Nicholas Andreychek, manager of Appalachian crude and condensate for Mississippi-based Ergon Oil Purchasing, said he has never seen condensate prices like this. On Thursday, the credit rating agencies Moody’s and Fitch Ratings both downgraded Denver-based Antero Resources, a Marcellus and Utica-focused operator and the nation’s second-largest producer of natural gas liquids.

Williams Scores Approval for Leidy South Natural Gas Project – FERC on Friday approved the Williams Leidy South natural gas pipeline project that would connect Marcellus/Utica shale supply to demand markets along the Atlantic Seaboard ahead of the 2021-2022 winter. The 582,400 Dth/d pipeline, an extension of the massive Transcontinental Gas Pipe Line system, aka Transco, would source gas produced by Cabot Oil & Gas Corp. and Seneca Resources Co. LLC. The project is to include six miles of large-diameter pipeline loop, two compressor stations and associated facilities in Pennsylvania’s Clinton, Columbia, Lycoming, Luzerne, Schuylkill and Wyoming counties.Williams CEO Alan Armstrong said the project represents one of many opportunities to further reduce greenhouse gas emissions, noting that “there remain more than 80 coal plants in the states Transco serves that can potentially be displaced” by gas.By maximizing the use of the existing Transco transmission corridor and expanding existing facilities in Pennsylvania, Leidy South would “substantially reduce” the amount of new infrastructure and land use required to meet these needs, minimizing community and environmental impact, Armstrong said.”With the growing urgency to transition to a low-carbon fuel future, Williams and its natural gas-focused strategy provide a practical and immediate path to reduce industry emissions, support the viability of renewables and grow a clean energy economy,” the CEO said. Approval by the Federal Energy Regulatory Commission for Leidy South comes at an uncertain time for oil and gas pipelines across the country.Earlier this month, Dominion Energy and Duke Energy canceled the proposed Atlantic Coast gas pipeline project, citing ongoing delays and increasing cost uncertainty. Meanwhile, the future of the Dakota Access crude pipeline, three years after entering service, is increasingly unclear amid an ongoing legal battle over key water-crossing permits.

Appalachian Basin Becoming Petrochemical Hub— It’s the third leg of a three-legged stool proponents, experts, consultants – even the federal government — agree is key to the Appalachian Basin once again becoming a U.S. petrochemical hub.Appalachia certainly has the natural gas liquids production (Leg No. 1), as it leads the U.S. in natural gas production, with more than 20% of Marcellus and Utica Shale play production in the form of natural gas liquids (NGLs).Within 18 months, Shell’s massive $6 billion cracker (Leg No. 2) northwest of Pittsburgh should be online, tapping the free-flowing NGLs in Appalachia. And more crackers are expected going forward.But as the petrochemical industry expands in Appalachia, NGL storage (the third leg) becomes an increasingly vital component of NGL infrastructure. The largest announced NGL storage hub proposed for the Appalachian Basin is the Appalachian Storage Hub, a $10 billion, public-private project that would be located along the Ohio River in the basin.What is envisioned in the hub is a system of underground caverns, salt caves and areas where natural gas was extracted. Roughly 100 million barrels of NGLs would be stored, plus the project includes 3,000 miles of pipelines to move the chemicals to industries along a 454-mile corridor in the states of Pennsylvania, Ohio, West Virginia and Kentucky.To keep you up-to-date on Appalachian hub progress, along with other, planned storage facilities in the basin, join industry brethren, including competitors in the Upstream, Midstream and Downstream sectors, at the Fourth Annual Appalachian Hub Conference, presented by ShaleDirectories.com and TopLine Analytics.The one-day conference on Aug. 27, at the Hilton Garden Inn, in the Southpointe Office Park just off Interstate 79 South, south of Pittsburgh, in deference to the ongoing Coronavirus pandemic, for the first time will be a hybrid production: The audience can attend in person, or attend – interact, with speakers – via LIVE streaming. The price is $495.

More common sense needed on fossil fuels – Randi Pokladnik – Last week’s Times Leader (July 5, 2020) carried an op-ed by Greg Kozera, the director of marketing and sales for Shale Crescent USA. In the op-ed Mr. Kozera talked a lot about common sense and our need for fossil fuels: specifically, plastics.In a world drowning in plastic, common sense would dictate that we need to significantly cut down on our production of single-use plastics. According to the Ocean Conservancy, which monitors litter on beaches worldwide, the 10 most common items of litter picked up by volunteers were made of plastic. This included cigarette butts, food wrappers, drink bottles, caps and grocery bags. Not surprising, as plastic packaging makes up about 40 percent of all the plastics produced today.One of the major issues with plastics is that they do what they are intended to do very well; they last forever. Plastics are long-chain carbon polymers that are synthesized from petroleum or natural gas feedstocks. Unlike other naturally occurring long-chain carbon compounds, such as carbohydrates found in plants, plastics will not degrade when exposed to enzymes or bacteria in the environment. Common sense would ask is it wise to expand the production of something that never degrades? According to a study published in 2017 in Science Advances, we have produced approximately 8,300 million metric tons of plastic since the 1950s. Plastic waste now blankets our planet. More than 8 million tons of plastic is dumped into our oceans every year. Peer reviewed studies show that water from the Great Lakes contains a substantial amount of microplastics. Research published in the Public Library of Science disclosed microplastics were in 12 American beers. A study published in ORB Media determined that of 159 tap water samples taken from around the world, 83 percent contained plastic particles. Mr. Kozera points to recycling as a solution to our plastic wastes. In 2017, there were 6.3 billion tons of plastic waste. Only 9 percent was recycled, 12 percent was incinerated and 79 percent ended up in landfills or the environment. I am old enough to remember the Keep America Beautiful anti-litter campaign of the 1970s. Backed by the beverage industry, it was a slick attempt to continue the production of plastic beverage bottles by passing off the responsibility for litter to consumers. Common sense would ask how successful has recycling been if after nearly 50 years, we only recycle 9 percent of our plastic waste.

Wolf, legislature draw closer to more tax breaks for the natural gas industry – State lawmakers voted this week on a bill that would benefit the state’s natural gas industry by providing an incentive for manufacturers that use the gas.The legislation would give tax credits to fertilizer and petrochemical manufacturers that create jobs. The state Senate voted 40-9 Monday to approve the measure. The state House of Representatives agreed Tuesday with a vote of 163-38. At an unrelated news conference earlier Tuesday, Gov. Tom Wolf said he supports the legislation.The measure is similar to a bill the governor vetoed in March. Wolf’s veto message cited the economic hardship created by the coronavirus pandemic and the need for a “responsible use of the Commonwealth’s limited resources. At the Tuesday news conference, Wolf said he was concerned the first version of the bill didn’t have “adequate protections for prevailing wage for the workers” and that it was “fiscally irresponsible” for giving more than $1 billion in potential tax credits.”This has cut the … amount of money available over 25 years by a lot and it has placed a cap per year on the spending, which was not in the original bill, so this is a better bill,” he said.The original bill, HB 1100, passed both chambers of the General Assembly with veto-proof majorities. Backers have been calling for a veto-override vote, though the effort took a backseat as attention turned to COVID-19.The new measure appears to be something of a compromise. It limits the credits to $26.7 million per fiscal year and caps recipients at four, making the maximum annual credit per company $6.7 million. The tax program would begin in 2024 and last until 2050, for a total of nearly $670 million in tax credits.A state Department of Revenue analysis of the previous bill found the annual credit per manufacturing facility could reach $26.5 million, which could have led to more than $1 billion in credits over the course of the program. The new legislation, HB 732, would lower the qualifying threshold a manufacturer needs to invest by $50 million to $400 million, but keeps the combined number of new and permanent jobs required for the incentive at 800.

As Pennsylvania Lawmakers Push Sneaky Petrochemical Corporate Subsidies, Investing in Renewables Would Be Jobs Bonanza | Food & Water Watch –Yesterday, the State Senate passed an amendment to an unrelated bill that will grant massive tax breaks to petrochemical corporations in Pennsylvania, a move that recalls legislation (HB 1100) that was vetoed by Governor Tom Wolf earlier this year.While these corporate handouts are promoted as a powerful tool to create desperately needed jobs, forthcoming research from the national organization Food & Water Watch reveals that the subsidies awarded to energy giant Shell to build a plant in Beaver County created far fewer jobs than supporters predicted, and that a similar level investment in renewable energy projects would create far more employment opportunities.The Food & Water Watch research determined that while the state granted Shell an astonishing $1.6 billion in tax incentives for a project that will create a total of 600 permanent jobs (a cost of $2.75 million for every long-term job), a similar level of investment in wind and solar would create 16,500 jobs, which would almost match the state’s total employment in the oil and gas industries.In response to the Senate vote, Food & Water Watch Executive Director Wenonah Hauter released the following statement: “In the midst of a deadly global pandemic, Pennsylvania lawmakers are creating a secret scheme to hand hundreds of millions of dollars to petrochemical corporations in order to rescue the ailing fracking industry and create more plastic junk. Our research shows that investing in wind and solar provides far more bang for the buck. Instead of giving money to corporate polluters like Shell, lawmakers should put a halt to these absurd petrochemical giveaways, and build a clean, renewable energy industry that will create far more safe and stable jobs.”

Pa. Legislature adopts $670 million tax credit bill for petrochemical plants – A bill aiming to lure petrochemical and fertilizer plants to Pennsylvania with more than $650 million in new tax credits is on the way to Gov. Tom Wolf after the House and Senate passed it by large margins this week. The Democratic governor vetoed a similar bill earlier this year, but his administration was involved in negotiating this one and he said he plans to sign it. Neither bill was the subject of public hearings. House Bill 732 creates a new “local resource manufacturing tax credit” for companies that invest at least $400 million and create at least 800 construction and permanent jobs to build petrochemical or fertilizer plants that use dry natural gas produced in Pennsylvania. A maximum of four companies can qualify for the credits each year and each company’s annual tax credit is capped at $6.7 million. The credit would amount to $667 million in foregone taxes over the 25 years that the credit program would run from 2025 to 2050. The credit is modeled after one used to entice Shell to build its petrochemical plant in Beaver County, but this one is exclusive to petrochemical and fertilizer manufacturers that use dry natural gas rather than ethane. Dry gas is produced abundantly from the Marcellus Shale in northeastern and north-central Pennsylvania and, to a lesser extent, from Pennsylvania’s Utica Shale. The dry gas requirement disqualifies most Marcellus Shale gas produced in southwestern Pennsylvania, which is considered “wet” because it contains natural gas liquids. The bill Mr. Wolf vetoed earlier this year would have incentivized the use of natural gas more broadly, but it contained no limits on how many plants could qualify for the credits and lacked enforcement provisions to ensure companies pay construction workers prevailing wage rates. Pennsylvania’s Department of Revenue estimated the vetoed proposal would have cost $22 million per year per plant in foregone taxes until the end of 2050.

Shell forced by Covid-19 case increases to slow down addition of workers in Beaver County – Royal Dutch Shell has temporarily halted the steady addition of workers returning to the massive Beaver County petrochemical plant construction site after an increase in Covid-19 cases that are apparently tied not to the site but sharp rises of the novel coronavirus in the community. There have been 17 workers at the Shell plant that have tested positive for Covid-19, up from the six cases that had been confirmed between mid-March and the end of June. Shell had, with the first cases of Covid-19 in the early days of the pandemic, shut down construction on the $6 billion plant and sent all but 300 of its 8,000 construction workers home as the site was deep cleaned and mitigation measures put into place. It has been adding back employees in a measured way, increasing to about 3,500 to 3,700 employees on site now. “Based on contact tracing and what we see going on in the broader community, in increased cases in Beaver and Allegheny counties, we believe that’s not reflective of the additional risks occurring at the site but people being in the community,” Shell spokesman Michael Marr said during the Petrochemical Development USA conference Thursday afternoon. “We believe we have a good exposure control on site that we’ve implemented.” Further details weren’t immediately available about the new cases, but Marr said as the number of cases have grown, Shell has taken steps to prevent more Covid on its site. “We’ve decided to at least temporarily halt the addition of workers,” Marr said. It’s a week-by-week decision that is made every Thursday afternoon for the week ahead whether to keep adding workers. “We only will do so when we are comfortable we have sufficient levels of mitigation procedures in place to manage Covid spread,” Marr said.

Damning report on Pa.’s failure to protect residents from fracking unlikely to result in major reform – The recent findings of a massive grand jury investigation into the state’s failure to protect communities from unconventional oil and gas development, known as fracking, were damning, and lent official credence to problems many residents have decried for years. The long-anticipated report outlined explicit ways in which the Department of Environmental Protection and the Department of Health turned a blind eye to the snowballing effects of fracking on Pennsylvania’s residents and skirted constitutional obligations to protect the environment. State officials testified about directives to ignore health concerns and practices that glossed over the harm the public experienced, effectively gaslighting residents whose tap water appeared brown or experienced rashes when they showered, but were told nothing was wrong. The testimony also revealed how officials deferred to the industry and poorly tracked complaints, and how state workers failed to properly test potentially tainted air and water. “More than anything, it is the government’s willingness to use the tools at its disposal to protect people,” Alex Bomstein, an attorney for Clean Air Council, said. “That’s what needs to change.” Despite the two-year effort to bring these findings to light – encompassing 287 hours of testimony before the grand jury, resulting in a 243-page report – it’s unclear if the grand jury’s report will bring about actual, meaningful reforms sought by those who say they’ve been harmed.Several of the report’s recommendations address problems previously raised by advocates in legal cases and unsuccessful pushes for new legislation to better account for the health and environmental impacts of fracking. Some lawmakers said the proposals overreach and are an ineffective way to change policy.State agencies, meanwhile, dismissed the report outright, calling the recommendations unnecessary and crafted by a group of people unqualified to understand environmental law. Many of the issues raised were outdated, they said, and already addressed.

Q&A: Terry Engelder, Penn State scientist whose work led to the shale gas boom, talks about grand jury report on fracking – – interview – In 2007, Terry Engelder, then a professor of geosciences at Penn State, estimated how much natural gas could be accessed in the Marcellus Shale formation using hydrofracking. That calculation led to a drilling boom across the Marcellus region in Pennsylvania.Widely recognized for his work, Engelder has advised state agencies, including the Pennsylvania Department of Environmental Protection. And, his research has received funding from a number of companies in the industry. Now retired and a professor emeritus, Engelder is working on a book called “A Frackademic from Appalachia.” Along with economic benefits, the surge in gas exploration in Pennsylvania led to environmental and health concerns. On June 25, state Attorney General Josh Shapiro announced the findings of a Pennsylvania grand jury condemning the DEP and state Department of Health for inadequate oversight of the natural gas industry.The report outlines problems from brown water caused by fracking to the state dismissing residents’ complaints without investigation. The report also makes recommendations from additional pipeline regulation to increasing the setback of oil gas wells. StateImpact Pennsylvania spoke with Engelder about the grand jury’s findings.

Marcellus Shale region project, others scrapped after increased regulatory requirements and environmental opposition – – The push to bring more economic development to western Pennsylvania, West Virginia and Ohio – referred to as the shale crescent region – has encountered a major glitch after an $8 billion Atlantic Coast Pipeline plan was cancelled in Appalachia and other projects have been slowed or halted. Cancellations come after state regulations and environmental opposition increased. Production from the Marcellus Shale was expected to rebound after some states reopened after coronavirus shutdowns. Fracking in the region has driven down natural gas prices and helped to make the U.S. a net exporter of the fuel for the first time, Bloomberg News reports. In June, the U.S. Department of Energy announced a major initiative in response to President Donald Trump’s Executive Order 13868, “Promoting Energy Infrastructure and Economic Growth” to assess opportunities to promote economic and energy growth in the Appalachian region. “The energy-rich Appalachian region is now the single largest natural gas producing region of the country and increasingly is becoming a major producer of natural gas liquids, including ethane, propane, and butane,” Secretary of Energy Dan Brouillette said in a statement. “These resources can serve as feedstocks for new opportunities in low-cost power generation, petrochemicals, and the manufacturing industry. Harnessing these opportunities will decrease our reliance on foreign-sourced supply-chains, as showcased by the COVID-19 pandemic, and bring back U.S. jobs to this important region of the country.” Richmond-based Dominion Energy Inc. and Charlotte-based Duke Energy Corp. abandoned plans to construct a major pipeline from the region to southern states. Canceling the Atlantic Coast Pipeline project, the companies said in a statement, was due to “ongoing delays and increasing cost uncertainty which threaten the economic viability of the project.” Dominion was also impacted by the Virginia Legislature enacting a law in April requiring it to be 100 percent carbon free by 2045. Both companies sold their natural gas assets to billionaire investor Warren Buffett’s Berkshire Hathaway Inc. – the largest deal announced in 2020 to buy U.S. energy assets, according to Bloomberg data.

The Atlantic Coast Pipeline Is Cancelled, But Here’s Why That’s Not Enough | Food & Water Watch – With many still grieving a recent Supreme Court ruling allowing the Atlantic Coast Pipeline to cut through the Appalachian Trail, big news hit last Sunday that Dominion and Duke Energy are canceling the pipeline altogether, with Dominion also selling off its remaining fracked gas holdings. The shutdown announcement from Dominion and Duke Energy comes after six years of entrenched legal battles, public protest and direct action to disrupt construction, and a price tag that grew to 8 billion dollars. Duke and Dominion didn’t make their decision out of goodwill – they made it with an eye to their bottom line. Dominion made the right decision for the wrong reasons. While a thriving clean energy economy does have the potential to bring well-paying jobs and increased investments to Virginia, profit isn’t the driving motivation for humanity’s move toward renewable energy. The transition to renewables is non-negotiable, and it needs to be funded by the companies that have wrecked our environment and exploited both people and resources for centuries – whether they want to make that payout or not. We have to move towards renewable energy because refusing to implement change will result in mass death, ecological crisis, and a hugely diminished quality of life. Virginia has the capacity to lead nationally in this transition, and the cancellation of the ACP should be an opening to speed ahead with the hard work of greening our state. Recent changes in the state’s legislative makeup made us hopeful for aggressive environmental legislation. But the last session brought disappointment when the pro-industry Virginia Clean Economy Act railroaded the more ambitious Green New Deal, and passed into law with Northam’s signature. The Virginia Clean Economy Act failed to demand more from Virginia’s fossil fuel corporations than what these companies had already agreed to, making it clear the legislation bent to the whims of industry rather than pushing past its comfort zone. The VCEA also set the deadline for a renewable energy transition at 2050, deemed a dangerously inadequate timeline by the world’s leading climate scientists. And it didn’t require any action to stop the fossil fuel infrastructure already underway in Virginia, projects that will ravage public health and clean air and water in the near term.

Senators hope Berkshire Hathaway invests in West Virginia natural gas projects – – A week after Berkshire Hathaway Inc. announced its purchase of Dominion Energy Inc.’s natural gas transmission and storage assets, a group of West Virginia senators are asking the company to consider investing in natural gas projects in West Virginia.Ten Democratic lawmakers sent a letter to Chairman and CEO Warren Buffett on Monday regarding a possible investment and the impact of the Atlantic Coast Pipeline project’s cancellation.”We think your wager is a wise one and share your belief that natural gas will be a mainstay in the production of American power for decades to come,” the legislators said. “The gas that sits beneath our feet is rich and plentiful, and our people are ready to go to work.”Duke Energy Corp. and Dominion Energy announced July 5 the cancellation of the Atlantic Coast Pipeline because of delays and legal uncertainties. The 600-mile pipeline would have gone from Harrison County, West Virginia into Virginia and North Carolina.Berkshire Hathway’s $9.7 billion deal with Dominion Energy was announced the same day. The agreement includes more than 7,700 miles of pipelines and around 900 billion cubic feet of natural gas storage. “That gave us reason for hope,” Sen. William Ihlenfeld, D-Ohio, said on Tuesday’s “MetroNews Talkline.”

US natgas output rises after W.Va. Mountaineer pipe returns (Reuters) – U.S. natural gas production rose over the weekend after TC Energy Corp’s Mountaineer Xpress pipeline in West Virginia returned to service following unplanned work, according to the company and data from Refinitiv.Pipeline data showed U.S. output climbed to 88.2 billion cubic feet per day (bcfd) on Sunday, up from a low of 87.0 bcfd last week due mostly to the Mountaineer shutdown. One billion cubic feet is enough gas to supply about 5 million U.S. homes for a day. TC Energy’s Columbia Gas Transmission (TCO) unit, which operates Mountaineer, said it returned the 2.6-bcfd pipe to service over the weekend after lifting a force majeure on July 11 that it imposed on July 7 due to unplanned maintenance. “The hard work of our crews and better than forecasted weather conditions led to the early lifting of the Force Majeure and return to service,” TCO said in a notice to customers. Most of the U.S. output increases came from Marcellus and Utica shale with West Virginia up about 0.3 bcfd from last week’s low to 6.9 bcfd and Pennsylvania up about 0.7 bcfd to 19.5 bcfd, according to Refinitiv. Despite last week’s decline in output, Refinitiv said production in the Lower 48 U.S. states has averaged 88.1 bcfd so far in July. That is up from a 20-month low of 87.0 bcfd in June after energy firms shut wells following the collapse in energy prices due to coronavirus demand destruction. Monthly output peaked at 95.4 bcfd in November.

Appalachia gas production edges back toward annual highs as EQT restores output – – Gas production in the Appalachian Basin has recently edged its way back toward highs not seen since early May as output previously curtailed by the region’s largest producer, EQT, now appears to be fully restored. In the past week, combined production from the Marcellus and Utica shales has averaged nearly 32.2 Bcf/d – up 1.2 Bcf/d, or about 4% from its mid-May average, S&P Global Platts Analytics data shows. At Appalachia’s benchmark supply hub, Dominion South, cash prices have remained near $1.30/MMBtu recently – comparable to levels seen after EQT’s production curtailments – as record gas-fired power burns this summer help to balance the additional supply length. On July 16, the cash market at Dominion South was nearly flat to its prior-day settlement, trading down just a half-cent to $1.285/MMBtu, preliminary trade data from S&P Global Platts showed. Roughly half of the recent gain in output has come from just five production meters used by EQT on Equitrans, Rockies Express Pipeline, Columbia Gas Transmission and Texas Eastern Transmission. Over the past five days, upstream receipts from those points have averaged a combined total of 2.7 Bcf/d, which compares to an average 2 Bcf/d in the five days after EQT announced its curtailments. Within the Appalachian Basin, the largest production gains have accrued in the South Pennsylvania dry window, with smaller gains from West Virginia and the Ohio dry – the same three sub-basins that saw steep declines following EQT’s mid-May production cuts.Over the balance of this year, Appalachian gas production is likely to remain below previous record-high levels at over 33 Bcf/d as growth is constrained by slower drilling and completion activity, limited midstream capacity and low gas prices.

U.S. natgas futures fall over 3% on rising output, less hot weather (Reuters) – U.S. natural gas futures fell over 3% on Monday on rising output and forecasts for less hot weather and lower air conditioning demand over the next two weeks than previously expected. Traders noted that prices declined despite a drop in liquefied natural gas (LNG) exports this month to their lowest since early 2018 due to global coronavirus demand destruction. Front-month gas futures fell 6.6 cents, or 3.7%, to settle at $1.739 per million British thermal units. Refinitiv said production in the Lower 48 U.S. states averaged 88.1 billion cubic feet per day (bcfd) so far in July, up from a 20-month low of 87.0 bcfd in June but still well below the all-time monthly high of 95.4 bcfd in November. Refinitiv forecast U.S. demand, including exports, will rise from 90.4 bcfd this week to 92.2 bcfd next week. That, however, was lower than Refinitiv’s outlook on Friday. Pipeline gas flowing to U.S. LNG export plants averaged just 3.2 bcfd (33% utilization) so far in July, down from a 20-month low of 4.1 bcfd in June and a record high of 8.7 bcfd in February. Utilization was about 90% in 2019. Flows to Freeport in Texas held at zero for a seventh day for the first time since July 2019 when the first of its three liquefaction trains was in test mode. U.S. pipeline exports, meanwhile, rose as consumers in neighboring countries cranked up their air conditioners. Refinitiv said pipeline exports to Canada averaged 2.5 bcfd so far in July, up from 2.3 bcfd in June, but still below the all-time monthly high of 3.5 bcfd in December. Pipeline exports to Mexico averaged 5.5 bcfd this month, up from 5.4 bcfd in June, but below the record 5.6 bcfd in March.

U.S. natgas futures edge up on hot weather forecasts, rising pipeline exports (Reuters) – U.S. natural gas futures edged higher on Tuesday on forecasts for more hot weather and higher cooling demand over the next two weeks and an increase in pipeline exports to Canada and Mexico. Traders noted prices were up even though output continued to rise slowly and liquefied natural gas exports (LNG) remained at their lowest since early 2018 due to a global hit to demand from the coronavirus pandemic. Front-month gas futures rose 0.7 cents, or 0.4%, to settle at $1.746 per million British thermal units. Refinitiv said production in the Lower 48 U.S. states averaged 88.1 billion cubic feet per day (bcfd) so far in July, up from a 20-month low of 87.0 bcfd in June but still well below the all-time monthly high of 95.4 bcfd in November. Refinitiv forecast U.S. demand, including exports, will rise from 90.4 bcfd this week to 92.9 bcfd next week. That was higher than Refinitiv’s outlook on Monday. Pipeline gas flowing to U.S. LNG export plants averaged just 3.2 bcfd (33% utilization) so far in July, down from a 20-month low of 4.1 bcfd in June and a record high of 8.7 bcfd in February. Utilization was about 90% in 2019. Flows to Freeport in Texas held at zero for an eighth straight day for the first time since July 2019 when the first of its three liquefaction trains was in test mode. U.S. pipeline exports, meanwhile, rose as consumers in neighboring countries cranked up their air conditioners.

U.S. natgas futures up 2% on rising pipe exports, cooling demand – (Reuters) – U.S. natural gas futures gained almost 2% on Wednesday due to an increase in pipeline exports and as rising air conditioning demand over the next two weeks keeps the amount of gas going into storage lower than usual for this time of year. Prices rose despite a slow output increase and decline in liquefied natural gas exports to their lowest since early 2018. Front-month gas futures rose 3.2 cents, or 1.8%, to settle at $1.778 per million British thermal units. Refinitiv said production in the Lower 48 U.S. states averaged 88.1 billion cubic feet per day (bcfd) so far in July, up from a 20-month low of 87.0 bcfd in June but still well below the all-time monthly high of 95.4 bcfd in November. Refinitiv forecast U.S. demand, including exports, will rise from 90.8 bcfd this week to 93.6 bcfd next week. That was higher than Refinitiv’s outlook on Tuesday. Pipeline gas flowing to U.S. LNG export plants averaged 3.2 bcfd (33% utilization) so far in July, down from a 20-month low of 4.1 bcfd in June and a record 8.7 bcfd in February. Utilization was about 90% in 2019. Flows to Freeport in Texas held at zero for an ninth straight day for the first time since July 2019 when the first of its three liquefaction trains was in test mode. Refinitiv said pipeline exports to Canada averaged 2.5 bcfd so far in July, up from 2.3 bcfd in June, but still below the all-time monthly high of 3.5 bcfd in December. Pipeline exports to Mexico averaged 5.5 bcfd this month, up from 5.4 bcfd in June, but below the record 5.6 bcfd in

US working natural gas volumes in underground storage rise by 45 Bcf: EIA – US natural gas stocks increased nearly 20 Bcf less than the five-year average due to year-to-date high gas-fired power demand, but the NYMEX Henry Hub balance-of-summer strip remained relatively static despite even smaller builds likely in the weeks ahead. Storage inventories rose 45 Bcf to 3.178 Tcf for the week ended July 10, the US Energy Information Administration reported July 16. The injection was below an S&P Global Platts’ survey of analysts consensus that called for a 50 Bcf build. Wider responses to the survey ranged from injections of 42 Bcf to 65 Bcf. The build was also less than the 67 Bcf injection reported during the same week last year and the five-year average injection of 63 Bcf, according to EIA data. It was the third consecutive weekly build that was below the five-year average. Storage volumes now stand at 663 Bcf, or 26.4%, more than the year-ago level of 2.515 Tcf and 436 Bcf, or 16%, more than the five-year average of 2.742 Tcf. Total demand rose by 1.4 Bcf/d during the week after 2.6 Bcf/d of power burn increases were reduced by a 1 Bcf/d drop in LNG feedgas demand and another 500 MMcf/d of declines from the residential and commercial sector, according to S&P Global Platts Analytics. Upstream, supplies rose slightly on an increase in onshore production and an increase in net Canadian imports, pushing total supplies higher by 400 MMcf/d and leaving US supply-demand balances tighter by 1 Bcf/d week on week. The NYMEX Henry Hub balance-of-summer contract, August through October, remained relatively static to average $1.846/MMBtu in trading following the release of the EIA’s weekly storage report. Spreads to next winter have remained stable as well. The November-through-March contract strip is priced at $2.71/MMBtu, leaving spreads from balance of summer to next winter in the high 80 cents/MMBtu range. Platts Analytics’ supply-and-demand model currently expects a 36 Bcf injection for the week ending July 17, which would be 1 Bcf below the five-year average.

U.S. natgas futures fall to two-week low as output rises, low LNG exports – (Reuters) – U.S. natural gas futures fell over 3% to a two-week low on Thursday as output slowly rises and liquefied natural gas exports hold near their lowest since early 2018. That price decline came despite a smaller-than-usual storage build that was in line with estimates and forecasts hot weather expected to keep air conditioning demand high over the next two weeks. The U.S. Energy Information Administration (EIA) said U.S. utilities injected 45 billion cubic feet (bcf) of gas into storage during the week ended July 10. That was close to the 47-bcf build analysts forecast in a Reuters poll and compares with an increase of 67 bcf during the same week last year and a five-year (2015-19) average build of 63 bcf for the period. The increase boosts stockpiles to 3.178 trillion cubic feet (tcf), 15.9% above the five-year average of 2.742 tcf for this time of year. By the end of the injection season in October, analysts expect U.S. inventories will reach a record high near 4.1 tcf. Front-month gas futures fell 5.5 cents, or 3.1%, to settle at $1.723 per million British thermal units, their lowest close since July 1. Refinitiv said production in the Lower 48 U.S. states averaged 88.1 billion cubic feet per day (bcfd) so far in July, up from a 20-month low of 87.0 bcfd in June but still well below the all-time monthly high of 95.4 bcfd in November. As consumers crank up their air conditioners, Refinitiv forecast U.S. demand, including exports, will rise from 90.8 bcfd this week to 93.5 bcfd next week.