Written by Steven Hansen

There was one significant improvement in the final GOP income tax plan which shifted my negative opinion to neutral.

Please share this article – Go to very top of page, right hand side, for social media buttons.

From my 17 November post The GOP Tax Plan Has The Wrong Real Winners And Losers:

The USA has a growing problem of income distribution where there is a increasing disparity between the rich and the poor.

This was and is my main issue with the GOP tax plan. I guess I am not a good Republican as I do not believe that making the rich richer will trickle down to the average Jane and Joe – and my belief is it will exasperate the existing negative trends on wealth distribution. But being a realist, I also said in this post:

Even if the Democrats and Republicans worked together, I doubt a reasonable tax plan could be created as the vested interests, who believe they win from loopholes, will not roll over.

There is little question that the GOP tax plan favored the rich with the greatest benefit. From VOX [note this is an interesting post to visit as it includes many tables to understand the impact of the new tax legislation]:

Overall, 53.4 percent of American households would see a tax increase and 25.2 percent would see a tax cut in 2027. But the shares depend substantially on what income group you’re in. Most Americans in the bottom fifth of the distribution – those in poverty, or near poverty – wouldn’t see their taxes change either way, as they typically don’t earn enough money to pay income taxes. The different inflation measure can reduce the tax refund they receive from the earned income tax credit and child tax credit, but the effect is fairly small.

By contrast, nearly 70 percent of Americans in the middle fifth of the income distribution – earning $54,700 to $93,200 a year in 2017 dollars – would see their taxes go up, with an average tax hike of $150. That’s not a huge change, but the direction is certainly not favorable.

Republicans advocating for the bill have focused less on 2027, when much of the bill’s changes will have expired, than on 2018 through 2025, when all its cuts, including for individuals, will be in effect. In 2018, the bill is an across-the-board cut for all income groups, but the biggest cuts are reserved for the upper middle class.

Still there remains much confusion on what will happen to Jane and Joe’s taxes. From CBS:

Tax experts are combing through the legislation to get a handle on how its new tax brackets and treatments of everything from bonds to charitable donations will impact their clients. Meanwhile, Republican leaders say the tax bill will put more money in the pockets of average Americans.

The bill will lower taxes for the middle-fifth of taxpayers by $800 per year on average, but people in the top 1 percent of the income distribution will enjoy an average cut of $55,000, the Institute on Taxation and Economic Policy estimates.

It still may be too early to say for sure how the new GOP taxes will affect Jane and Joe. I have consistently worried about Jane and Joe. In my 04 February 2017 post I stated:

I have seen little yet that President Trump has done anything to affect the economy – either positively or negatively. The political path since the 1960s has been to favor the needs of the 0.1% and business over the general population. I am waiting for any economic action where it is obvious the median household is favored over the 0.1 %.

The realization is that there may never be a great tax plan for Jane and Joe – so the question becomes is whether the new GOP law is better than the old tax situation. A few weeks ago I believed it was worse than the current tax codes – but the final reconciled bill included the repeal of the Affordable Care Act’s individual mandate which required all to have health insurance – and penalized those who did not. In reality, Obamacare required young adults to subsidize the healthcare costs of the sick and relatively older cohorts. Before Obamacare, the young could buy health insurance at relatively low rates, or take the risk and not buy health insurance. The young have a relatively low risk of accruing significant health care costs.

Consideration when one should buy any kind of insurance?

- when the premiums are cheap compared to the potential loss. In the case of Obamacare, the Millennial making $30K per year paid $1500 to $4000 a year for a silver plan with a $5000 deductible.

- when the risk of loss is very low [this is why most Americans do not have flood insurance]

- when the potential loss would be so great it would significantly affect your life

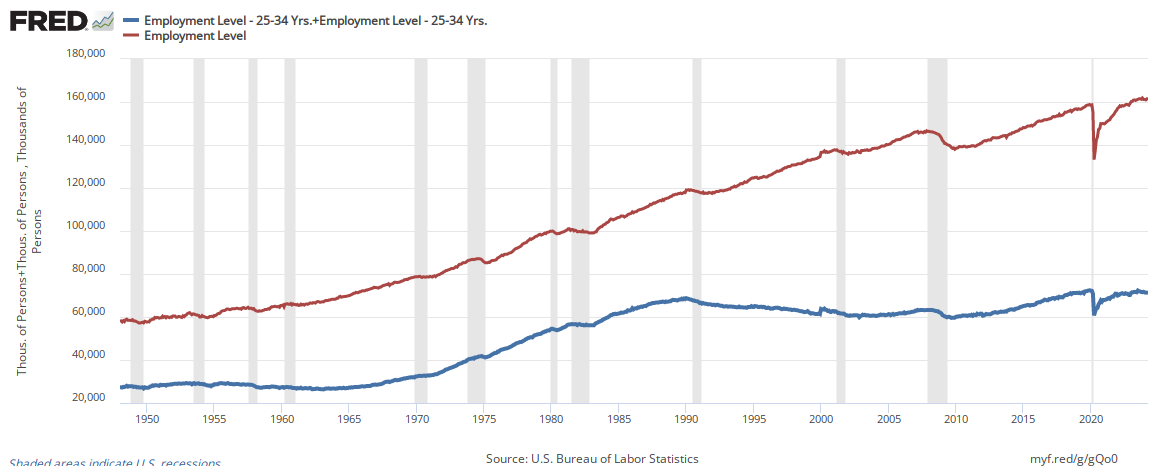

With the individual mandate gone, the Millennials will be able to decide if they want to buy health insurance. This money will now be free to spend for goods and services that will not flow into the insurance industry. To understand the size of this potential tax relief – 45% of working Americans are Millennials [see graph below].

To be clear – I am strongly in favor of universal health care. Obamacare was a step in that direction – but it failed to lower health care costs. And I strongly oppose that too much of the burden of paying for health care was placed on generation which is trying to get established in life.

Finally I will come back to my original objection which is unchanged: The new tax law provides too much benefit for the 0.1%.

The devil is in the details – not in the sweet words of the politicians who sold both Obamacare and the GOP tax plan.

Other Economic News this Week:

The Econintersect Economic Index for January 2018 significantly improved and now is in territory associated with stronger economic growth. Still the economic growth forecasts in 2017 remained in a very narrow band.

Bankruptcies this Week from bankruptcydata.com: none