Written by Steven Hansen

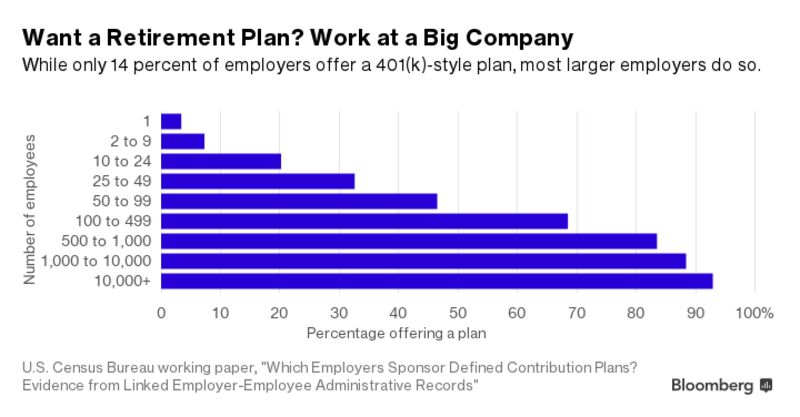

Approximately 55 million Americans contribute tax-free to a 401(k). The Republicans in Congress had looked at making this contribution taxable as a way to offset over $1.5 trillion in tax cuts (over a decade) under their new tax plan. The latest tax proposal did not change the 401(k) taxation – but would it have mattered?

Please share this article – Go to very top of page, right hand side, for social media buttons.

Under current law, an employee can contribute up to $18,000 per year tax free to these accounts ($18,500 beginning in 2018), and the employer can contribute to this account also up to a contribution limit of $54,000 per year (there are exceptions). At retirement, all withdrawals (including initial tax free contribution, dividends, interest and capital gains) are taxed.

Yes, President Trump has tweeted:

“There will be NO change to your 401(k). This has always been a great and popular middle class tax break that works, and it stays!

But the issue really is that the details of any change to 401(k) is sketchy. Would would happen to the owner contribution portion? Would this mean that the 401(k) program be changed to resemble the existing Roth 401(k) – contributions to Roth IRAs or Roth 401(k) plans are made with after-tax dollars – but the accumulation of dividends, interest, and capital gains is never taxed..

The CBO has stated reducing the tax-free element of 401(k) likely not a good thing to the lower and moderate income wage earner:

….. The main argument against this option is that it would reduce the retirement saving of some lower- and -moderate-income people. Eliminating the extra allowance for catch-up contributions in particular would adversely affect those ages 50 and over who might have failed to save enough for a comfortable retirement while raising their families. The amount that they could contribute to tax-preferred retirement accounts would be cut at precisely the time when reduced family obligations and impending retirement make them more likely to respond to tax incentives to save more.

Finally, further limiting total contributions to a defined contribution plan would create an incentive for some small businesses to terminate their plans if the tax benefits to the owners of providing such plans were outweighed by the cost of administering them. To the extent that such plans were terminated, employees would then have to rely on IRAs, which would lead some to save less because of the lower contribution limits.

And to add confusion on whether a Roth type taxed retirement account is worse than the traditional IRA – here is some graphics from the Bipartisan Policy Center:

It is not clear whether taxing 401(k) contributions hurts anyone – but it does not really change government revenue over the long haul.

For a good summary of the Trump tax plan – [click here]

Other Economic News this Week:

The Econintersect Economic Index for November 2017 returned to the range of normal growth after last months brief dip. Still, the economic fundamentals are somewhat chaoic. Six-month employment growth forecast is now indicating slowing growth.

Bankruptcies this Week from bankruptcydata.com: Privately-held M & G USA and 11 affiliated Debtors – including parent Luxembourg-based Mossi & Ghisolfi International S.a r.l., Armstrong Energy, Privately-held Bestwall