Written by Steven Hansen

Just before then President-elect Trump was entering office, I penned a post saying that he was lucky as leading indicators were showing there was a surging economic cycle underway.

Please share this article – Go to very top of page, right hand side, for social media buttons.

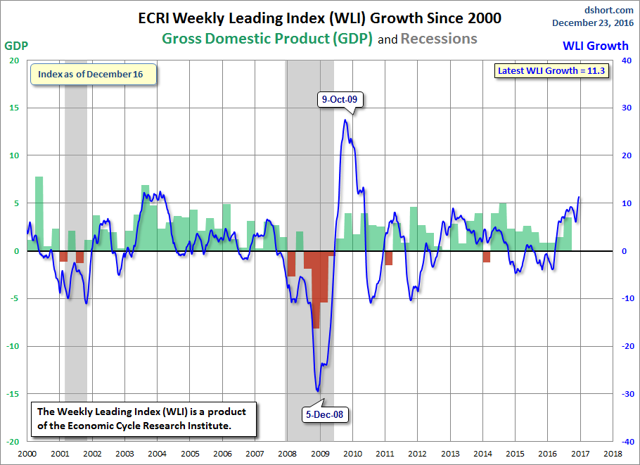

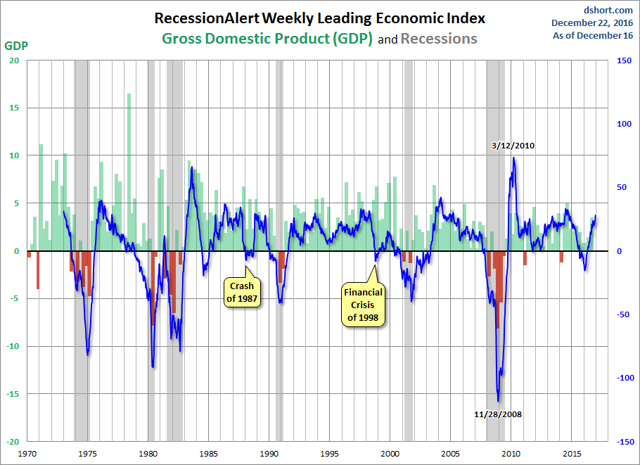

From that post, including the graphics:

President-elect Trump is more than likely to be handed an economy where the underlying dynamics are already accelerating. Two leading indicators ECRI Weekly Leading Index and RecessionAlert’s Weekly leading Index are both accelerating and their values are at levels consistent with strong economic growth.

Here we are 6 months later – and we should be witnessing an economic surge. Here is what the Chicago Fed National Activity Index (the super-coincident index) Is showing:

One does not need to see the above CFNAI graphic to realize there was no economic surge in the last 6 months. There is little a President can do (besides being a cheerleader) to stimulate the economy – and economic growth can be easily throttled by Congress (not only using fiscal policy, but also laws and rules on business and consumers) and the Federal Reserve (monetary policy). In any event, there is little Congress could do (short of dropping money into the pockets of consumers) which would significantly boost the economy within a six month period.

Is it possible that the Fed’s monetary tightening cycle can have a more immediate affect – and any potential economic improvement could have been suppressed. In the last 6 months, there has been a continuing increase in the Feds Funds rate.

There simply is no scientific evidence (lots of theory though) which correlates what the Fed’s monetary policy is currently doing to economic growth. And according to Yellen’s recent testimony to Congress, more monetary action is coming.

The Committee intends to gradually reduce the Federal Reserve’s securities holdings by decreasing its reinvestment of the principal payments it receives from the securities held in the System Open Market Account. Specifically, such payments will be reinvested only to the extent that they exceed gradually rising caps. Initially, these caps will be set at relatively low levels to limit the volume of securities that private investors will have to absorb. The Committee currently expects that, provided the economy evolves broadly as anticipated, it will likely begin to implement the program this year.

Once we start to reduce our reinvestments, our securities holdings will gradually decline, as will the supply of reserve balances in the banking system. The longer-run normal level of reserve balances will depend on a number of as-yet-unknown factors, including the banking system’s future demand for reserves and the Committee’s future decisions about how to implement monetary policy most efficiently and effectively. The Committee currently anticipates reducing the quantity of reserve balances to a level that is appreciably below recent levels but larger than before the financial crisis.

Finally, the Committee affirmed in June that changing the target range for the federal funds rate is our primary means of adjusting the stance of monetary policy. In other words, we do not intend to use the balance sheet as an active tool for monetary policy in normal times. However, the Committee would be prepared to resume reinvestments if a material deterioration in the economic outlook were to warrant a sizable reduction in the federal funds rate. More generally, the Committee would be prepared to use its full range of tools, including altering the size and composition of its balance sheet, if future economic conditions were to warrant a more accommodative monetary policy than can be achieved solely by reducing the federal funds rate.

I am not against gradually normalizing the Federal Funds Rate. Frankly, there is no trust that the Fed is smart enough to manipulate rates in the long term. In theory, this normalization should slow the economy but this pain could be offset by fiscal policy. The problem is that Congress is in an austerity mode. Tightening money and continuing fiscal austerity could be a 1-2 punch.

Other Economic News this Week:

The Econintersect Economic Index for July 2017 continues to forecast strengthening economic fundamentals – with the index showing normal growth for the third month in a row. Six-month employment growth forecast indicates modest improvement in the rate of growth.

Bankruptcies this Week from bankruptcydata.com: none