Written by Steven Hansen

It is hard to get worked up about velocity of money. Sometimes it is rising going into a recession, sometimes it is falling. One general truth is that it has been slowing since the early 1980s.

Please share this article – Go to very top of page, right hand side for social media buttons.

The velocity of money has become a metric with little predictability for other economic metrics. A relevant post from the St. Louis Fed stated in part:

… during the prerecession period, for every 1 percentage point decrease in 10-year Treasury note interest rates, the velocity of the monetary base decreased 0.17 points, based on a linear regression model of the velocity onto interest rates. Since 10-year interest rates declined by about 0.5 percentage points between 2008 and 2013, the velocity of the monetary base should have decreased by about 0.085 points. But the actual velocity has gone down by 5.85 points, 69 times larger than predicted. This happened because the nominal interest rate on short-term bonds has declined essentially to zero, and, in this case, the best form of risk-free liquid asset is no longer the short-term government bonds, but money.

Of course there are general correlations – such as its relationship to inflation.

Even considering inflation, the correlations are far from perfect. But it is interesting to me that the trillions of dollars of quantitative easing had little apparent affect on the rate of decline in the velocity of money.

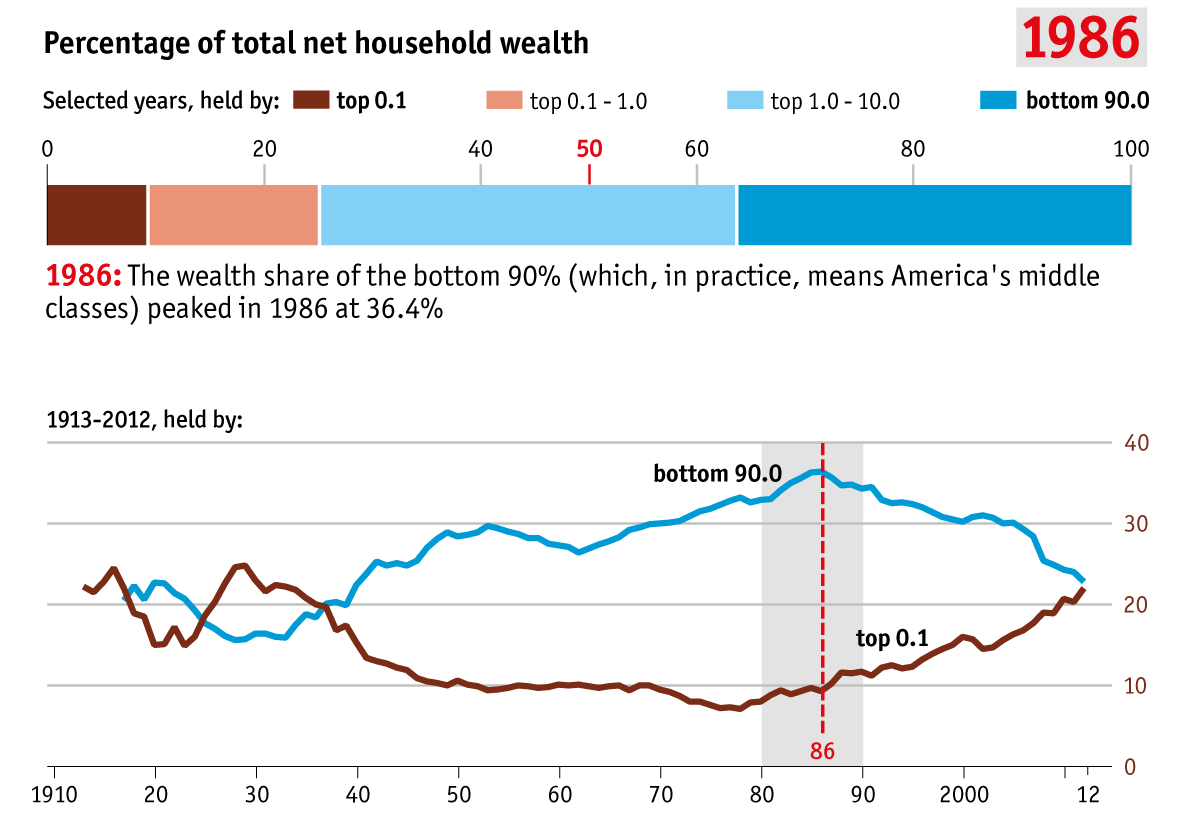

Is it possible that the distribution of wealth and income affect velocity of money? Logic dictates that the upper strata of wealth spends a far less percent of their income. And thus the more the inequality of wealth and income presents, the slower the velocity of money. From The Economist:

Is it just a coincidence the velocity of money slows at the same time wealth inequality is growing? And, at the same time, income inequality began growing. From the Center on Budget and Policy Priorities:

If wealth inequality is a major contributor to velocity of money, then we can add this to the list of detrimental affects of wealth inequality – as the wealthy are not consuming relative to the lower end of the economy.

Thinking this through

Economic systems should not be designed to punish those who succeed. I have seen no study which proves taking money from the rich and giving it to the poor reduces wealth inequality in the long term (the rich will always minimize loss even if it means relocating). Yet, it is obvious that for an economy to be healthy, the economic drag of wealth inequality is not helpful.

It is also obvious that wealth and income correlate. Some may say that the very rich derive a major share of their income from passive activities (such as capital gains).

Passive income does add to the inequality – and is one of the major drivers. In 2017 the highest USA tax rate for ordinary income is 39.6% whilst capital gains is taxed at 20%. This artificially causes the upper income sector of the economy to favor investments over income due to tax savings.

Should the USA change its tax laws to close this loophole (capital gains taxed at a lower level than employment income) which is adding to inequality? Is it not in the interest of the economy to reward investing? And if spending is so critical to economic growth – is it logical the USA taxes spending? There are complex factors involved when considering using taxation to reduce income and wealth inequality.

According to one study, the only historically effective mechanisms to reduce wealth inequality are:

mass-mobization wars (such as WWII)

transformative revolutions

major epidemics

abolition of slavery [not existing in advanced economies]

Wars, revolutions or epidemics do not sound good to me.

Other Economic News this Week:

The Econintersect Economic Index for April 2017 improvement trend continues although the value remains in the territory of weak growth. The index remains below the median levels seen since the end of the Great Recession. Six-month employment growth forecast indicates modest improvement in the rate of growth.

Bankruptcies this Week from bankruptcydata.com: Adeptus Health