from the Congressional Budget Office

If current laws remained generally unchanged, the United States would face steadily increasing federal budget deficits and debt over the next 30 years – reaching the highest level of debt relative to GDP ever experienced in this country.

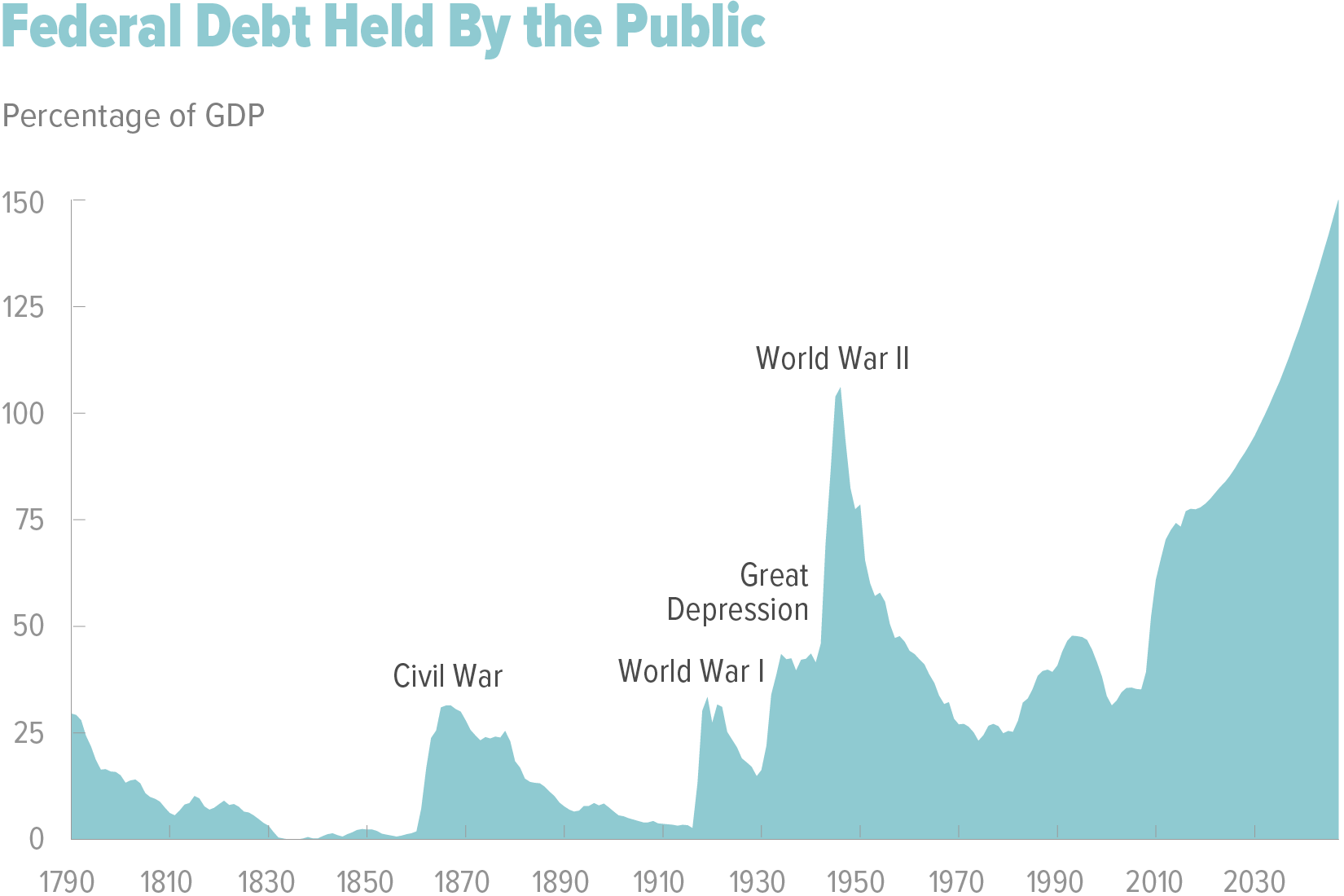

At 77 percent of gross domestic product (GDP), federal debt held by the public is now at its highest level since shortly after World War II. If current laws generally remained unchanged, the Congressional Budget Office projects, growing budget deficits would boost that debt sharply over the next 30 years; it would reach 150 percent of GDP in 2047. The prospect of such large and growing debt poses substantial risks for the nation and presents policymakers with significant challenges.

Why Are Projected Deficits Rising?

In CBO’s projections, deficits rise over the next three decades – from 2.9 percent of GDP in 2017 to 9.8 percent in 2047 – because spending growth is projected to outpace growth in revenues (see figure below). In particular, spending as a share of GDP increases for Social Security, the major health care programs (primarily Medicare), and interest on the government’s debt.

Much of the spending growth for Social Security and Medicare results from the aging of the population: As members of the baby-boom generation age and as life expectancy continues to increase, the percentage of the population age 65 or older will grow sharply, boosting the number of beneficiaries of those programs.

In addition, growth in spending on Medicare and the other major health care programs is driven by rising health care costs per person, which are projected to increase more quickly than GDP per capita (after the effects of aging and other demographic changes are removed). CBO projects that those health care costs will rise – although more slowly than they have in the past – in part because of the effects of new medical technologies and rising personal income.

The federal government’s net interest costs are projected to rise sharply as a percentage of GDP for two main reasons. The first and more important is that interest rates are expected to rise from their current low levels, making any given amount of debt more costly to finance. The second reason is the projected increase in deficits: The larger they are, the more the government will need to borrow.

Mandatory spending other than that for Social Security and the major health care programs – such as spending for federal employees’ pensions and for various income security programs – is projected to decline as a percentage of GDP, as is discretionary spending. (Mandatory spending is generally governed by provisions of permanent law, whereas discretionary spending is controlled by annual appropriation acts.) The projected decline in discretionary spending stems largely from the caps on discretionary funding that are set in law for the next several years.

The modest projected growth in revenues relative to GDP over the next three decades is attributable to increases in individual income tax receipts. Those receipts are projected to grow mainly because CBO anticipates that income will rise more quickly than the price indexes that are used to adjust tax brackets. As a result, more income will be pushed into higher tax brackets over time. Combined receipts from all other sources are projected to decline as a percentage of GDP.

What Might the Consequences Be If Current Laws Remained Unchanged?

Large and growing federal debt over the coming decades would hurt the economy and constrain future budget policy. The amount of debt that is projected under the extended baseline would reduce national saving and income in the long term; increase the government’s interest costs, putting more pressure on the rest of the budget; limit lawmakers’ ability to respond to unforeseen events; and increase the likelihood of a fiscal crisis, an occurrence in which investors become unwilling to finance a government’s borrowing unless they are compensated with very high interest rates.

How Does CBO Make Its Long-Term Budget Projections?

CBO’s long-term projections start with the agency’s 10‑year spending and revenue projections, which combine information about many spending programs and tax provisions with data about broader trends in the population and the economy. Those 10-year projections follow the assumptions that current laws governing taxes and spending will generally remain unchanged but that some mandatory programs will be extended after their authorizations lapse and spending for Medicare and Social Security will continue as scheduled even if their trust funds are exhausted. CBO makes those assumptions to conform to statutory requirements. Because current laws surely will change, CBO’s projections are not predictions of what the agency thinks will actually happen. Rather, they give lawmakers a point of comparison from which to measure the effects of proposed legislation. They are therefore referred to as the agency’s baseline projections.

CBO’s detailed long-term projections, produced once each year, follow those assumptions as well. Because they extend the 10-year baseline for two more decades, they are referred to as the extended baseline. Some projections, such as those for Social Security spending and collections of individual income taxes, incorporate detailed estimates of how people would be affected by particular elements of programs or the tax code. Other projections reflect past trends and CBO’s assessments of how those trends would evolve if current laws generally remained unchanged. Between the annual publications of the detailed analyses, CBO updates its long-term projections using simplified methods, as it did most recently in January 2017.

CBO’s budget projections are built on its economic projections, which incorporate the effects of the fiscal policy projected under current law. CBO anticipates that if current laws generally did not change, real GDP – that is, GDP with the effects of inflation excluded – would increase by 1.9 percent per year, on average, over the next 30 years. Over the past 50 years, the annual average growth rate of real GDP was roughly 1 percentage point higher. That slower economic growth in the future is attributable to several factors – notably, slower growth of the labor force, which is mainly a result of the aging of the population and the relative stability of women’s participation in the labor force after decades of increases. In addition, the productivity of labor is projected to grow more slowly than its historical average. Projected output growth also is held down by the effects of fiscal policy under current law – above all, by the reduction in private investment that is projected to result from rising federal debt.

How Uncertain Are Those Projections?

If current laws governing taxes and spending remained generally the same, debt would nearly double as a percentage of GDP over the next 30 years, according to CBO’s central estimate. That projection is very uncertain, however, so the agency examined in detail how debt would change if four key inputs – labor force participation, productivity in the economy, interest rates on federal debt, and health care costs per person – were higher or lower than their levels in the extended baseline. Other factors – such as an economic depression, a major war, or unexpected changes in fertility, immigration, or mortality rates – also could affect the trajectory of debt. Taking into account a range of uncertainty around CBO’s central projections of those four key inputs, CBO concludes that despite the considerable uncertainty of long-term projections, debt as a percentage of GDP would probably be greater – in all likelihood, much greater – than it is today if current laws remained generally unchanged.

How Large Would Changes in Spending or Revenues Need to Be to Reach Certain Goals for Federal Debt?

CBO estimated the magnitude of changes that would be needed to achieve a chosen goal for federal debt. For example, if lawmakers wanted to reduce the amount of debt in 2047 to 40 percent of GDP, its average over the past 50 years, they might cut noninterest spending, increase revenues, or take a combination of both approaches to make changes that equal 3.1 percent of GDP each year starting in 2018. That amount would total about $620 billion in 2018. If, instead, policy-makers wanted debt in 2047 to equal its current share of GDP (77 percent), the necessary measures would be smaller, totaling 1.9 percent of GDP per year (about $380 billion in 2018). The longer lawmakers waited to act, the larger the necessary policy changes would become.

How Have CBO’s Projections Changed Over the Past Year?

CBO’s long-term budget projections are generally similar to those the agency published in the past year. The previous edition of this volume, The 2016 Long-Term Budget Outlook, published in July 2016, showed projections through 2046. CBO now projects debt in 2046 that, measured as a share of GDP, is 5 percentage points higher than it projected last year. In addition, in January 2017 CBO released simplified long-term projections through 2047. The agency’s current projection of debt in 2047 is 5 percentage points higher than it was in January.

Data and Supplemental Information

Related Publications

The Budget and Economic Outlook: 2017 to 2027

January 24, 2017

CBO’s 2016 Long-Term Projections for Social Security: Additional Information

December 21, 2016

Options for Reducing the Deficit: 2017 to 2026

December 8, 2016

The 2016 Long-Term Budget Outlook

July 12, 2016