Written by Econintersect

Early Bird Headlines 26 February 2017

Econintersect: Here are some of the headlines we found to help you start your day. For more headlines see our afternoon feature for GEI members, What We Read Today, which has many more headlines and a number of article discussions to keep you abreast of what we have found interesting.

Global

Global Manufacturing 1970-2010 (Richard Baldwin, Twitter)

_icymi

Here are main slides of my book presentation

}https://t.co/7ws3AzdFjE

}

Please cite book if you use themhttps://t.co/RRlniYEk93 pic.twitter.com/32BW8sZTtB– Richard Baldwin (@BaldwinRE) February 26, 2017

U.S.

Since travel order lifted, more than 1,800 refugees from affected countries have entered U.S. (Pew Research Center) More than 1,800 refugees from Iran, Iraq, Libya, Somalia, Sudan, Syria and Yemen have resettled in the U.S. since a federal court judge suspended key parts of an executive order President Donald Trump signed on Jan. 27 that restricted travel from these seven nations, according to a Pew Research Center analysis of U.S. State Department data. Virtually all of these refugees were admitted after a federal court judge suspended the president’s executive order. Trump is expected to issue a revised executive order next week that would reinstate travel restrictions but will also change who will be affected in order to address the legal concerns surrounding the first order.

Leaked report suggests millions could lose coverage under GOP health proposal (Vox) Republican replacement plans for Obamacare would lead to significant declines in the number of Americans with health insurance coverage, according to an analysis presented Saturday at the National Governors Association and obtained by Vox. The analysis was conducted by the health research firm Avalere Health and the consulting firm McKinsey and Company.

The analysis includes graphs on what the Republican plan to overhaul Obamacare’s tax credits, generally making them less generous, would do. They are based on the recent 19-page proposal that Republican leadership released about their plan to repeal and replace Obamacare. In particular, they look at the effect of switching from income-based tax credits (which give poor people more help) to age-based tax credits, where everyone would get the same amount.

Click on either graphic for larger image.

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8045925/subsidy.png)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8046247/medicaid2.png)

Air Force Stumped by Trump’s Claim of $1 Billion Savings on Jet (Bloomberg) The Air Force can’t account for $1 billion in savings that President Donald Trump said he’s negotiated for the program to develop, purchase and operate two new Boeing Co. jets to serve as Air Force One. Colonel Pat Ryder, an Air Force spokesman, told reporters Wednesday when asked how Trump had managed to reduce the price for the new presidential plane. A White House spokesman didn’t respond to repeated inquiries about Trump’s comments. Trump has boasted that he’s personally intervened to cut costs of two military aircraft — the F-35, the fighter jet built by Lockheed Martin Corp., and Boeing’s Air Force One. Ryder said:

“To my knowledge I have not been told that we have that information. I refer you to the White House.”

GOP grapples with how to handle town halls (The Hill) Should congressional Republicans head for the bunkers, or continue to defend President Trump and the GOP agenda at raucous town hall events across the country? Republican leaders are grappling with that question as they try to contain the political fallout from the nonstop media coverage of anti-Trump constituents and activists disrupting and dominating GOP town halls.

There weren’t many, but the handful of House and Senate Republicans this recess week who chose to face their constituents at town hall events back home were booed, heckled, jeered, screamed at – and in some cases chased out of the room.

In some cases, constituents pleaded with lawmakers not to repeal ObamaCare, giving personal testimony about how they or their spouses could die without health care.

All of it was caught on video, and played on a seemingly endless loop on cable news networks and social media.

Trump lashes out at media for failing to report debt decrease (USA Today) President Trump took to Twitter on Saturday morning to claim the media ignored some good news about his administration. “The media has not reported that the National Debt in my first month went down by $12 billion vs a $200 billion increase in Obama first mo,” he tweeted. In a follow-up tweet, he added: “Great optimism for future of U.S. business, AND JOBS, with the DOW having an 11th straight record close. Big tax & regulation cuts coming!” Trump didn’t indicate where he got the numbers, but some of his supporters have been making the same argument. The Gateway Pundit, a far-right website, published an article Thursday citing figures from the Treasury Department that show the national debt stood at $19,947 billion the day Trump took office but fell to $19,935 billion by Feb. 21 – a drop of $12 billion. However, Business Insider reported the situations aren’t comparable. See also: Trump Wants Credit for Cutting the National Debt. Economists Say Not So Fast (Bloomberg) Econintersect: But the point made by BI is not the most important one missed by the president. We tweeted @realDonaldTrump:

France

Emmanuel Macron is edging closer to France’s presidency (The Economist) FRANCE’S most pro-European presidential candidate took his campaign to London this week to a rapturous welcome. Emmanuel Macron, a 39-year-old former Socialist economy minister, was there to court the French vote abroad, and is exactly the sort of upbeat, international-minded tech enthusiast that London’s latte-drinking French voters adore. Campaigning as an independent for votes on the left and the right, Mr Macron has pulled off the astonishing feat of hauling himself up from rank outsider to joint second place in the polls. But the closer he gets to a shot at the French presidency, the tougher his campaign is turning out to be. This article goes on to recount how Macron is not being very warmly received in traditionally more conservative districts.

Germany

How a Pillar of German Banking Lost Its Way (Spiegel Online) For most of its 146 years, Deutsche Bank was the embodiment of German values: reliable and safe. Now, the once-proud institution is facing the abyss. SPIEGEL tells the story of how Deutsche’s 1990s rush to join the world banking elite paved the way for its own downfall. Greed, provincialism, cowardice, unfocused aggression, mania, egoism, immaturity, mendacity, incompetence, weakness, pride, blundering, decadence, arrogance, a need for admiration, naiveté: If you are looking for words that explain the fall of Deutsche Bank, you can choose freely and justifiably from among the above list.

5 Reasons Germany Isn’t Suffering in the 21st Century (Vox) The five possible reasons:

The 1990s were so much better for the U.S. than for Germany. In the latter half of the decade the booming U.S. economy was the envy of the world. Germany, still recovering from some dubious economic decisions made when West and East were reunited in 1990, was the “sick man of Europe.” What goes up tends to go down, and vice versa. Or something.

Germany undertook a bunch of tough labor-market reforms in the early 2000s. A lot of those reforms just involved making the Germany labor market more like the U.S. labor market (that is, more flexible) — so that can’t explain the difference — but there were also improvements to the country’s retraining and job-placement institutions.

Germany doesn’t convict nearly as many people of crimes, relative to the overall population, as the U.S. does. I actually got this argument from Eberstadt, who wrote last year in his book “Men Without Work“:

A single variable — having a criminal record — is a key missing piece in explaining why work rates and LFPRs have collapsed much more dramatically in America than other affluent Western societies over the past two generations.

The euro. Somebody I talked to in Frankfurt called this the “Navarro argument,” after President Donald Trump’s trade adviser, Peter Navarro. The weakness of other European economies keeps Germany’s currency weaker than it would be if the country still used the deutsche mark. As a result, Germany runs bigger trade surpluses than it would otherwise and German manufacturing jobs are preserved. German experts tend to agree with this analysis, and agree that it’s not healthy for the rest of Europe and the world. They just don’t think Germany can do much about it.

Germany thinks differently about employment than the U.S. does. The lines in the above chart diverged between 2007 and 2010 — the years of the financial crisis and Great Recession. In the U.S., corporations (and state and local governments) fired millions of workers. In Germany, cooperation among employers, labor unions and the government kept job losses to a minimum. There were pay cuts, and furloughs, and shortened working hours. But when demand from overseas began to come back, German companies and workers were ready to meet it. In general, preserving jobs is a much bigger priority for German employers and politicians than it is in the U.S. At times in the past — the 1990s, for example — this focus has seemed misplaced. For the moment, though, it’s looking pretty smart.

Hong Kong

Hong Kong Existing Home Prices Rise to Record, Defying Curbs (Bloomberg) Hong Kong’s existing home prices have climbed to a record, fueled by a surge in demand from local buyers and investors despite taxes and mortgage curbs designed to rein in prices. The Centaline Property Centa-City Leading Index, which tracks sales in the secondary market, rose to 147.74 for the week ended Feb. 19, surpassing the previous high of 146.92 reached in September 2015. The index has rebounded 16% since home prices bottomed at the end of March. Mainland buyers have also been flocking to Hong Kong as a combination of surging prices and property curbs on the mainland make the city a more attractive alternative.

China

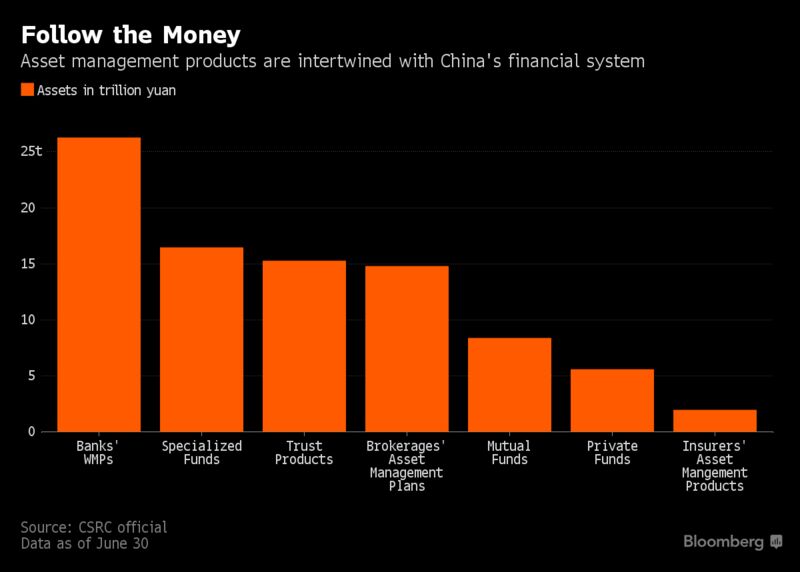

China’s $9 Trillion Moral Hazard Is Now Too Big to Ignore (Bloomberg) China may be about to embark on its most ambitious — and perilous — campaign to convince investors that they shouldn’t depend on a bailout when markets go south. In a rare show of cooperation, the nation’s main financial regulators are drafting new rules for asset-management products that aim to make clear the investments don’t have government guarantees, people familiar with the matter told Bloomberg News on Tuesday. The products, which promise higher returns than bank deposits but are viewed by many investors as a form of risk-free savings, have become an integral part of the Chinese financial system after swelling in recent years to almost $9 trillion as of June 30.

Australia

Australia and Indonesia Agree to Restore Full Military Ties (Bloomberg) Australian Prime Minister Malcolm Turnbull and Indonesian President Joko Widodo agreed to restore full military cooperation at a meeting between the two leaders in Sydney on Sunday. Indonesia moved to suspend all military partnerships between the two countries last month, citing technical issues. Australia’s Defense Minister Marise Payne said that concerns were raised in late 2016 by an Indonesian national armed forces officer over teaching materials and remarks at an Army language training facility in Australia.

Mexico

Most Americans continue to oppose U.S. border wall, doubt Mexico would pay for it (Pew Research Center)