from the Dirk Ehnts, Econoblog101

This is from the NY Fed’s FAQ:

Participation in the operations is open to the Federal Reserve’s primary dealers as well as its expanded RRP counterparties. Expanded RRP counterparties include a wide range of entities, including 2a-7 money market funds, banks, and government-sponsored enterprises. Additional details on the RRP counterparties are available on the New York Fed’s website.

The Fed is active in the money market, engaging with clients like money market funds, banks and GSEs. The target is to move the interest rate up to the new range of 1/4 to 1/2 percent:

The Committee judges that there has been considerable improvement in labor market conditions this year, and it is reasonably confident that inflation will rise, over the medium term, to its 2 percent objective. Given the economic outlook, and recognizing the time it takes for policy actions to affect future economic outcomes, the Committee decided to raise the target range for the federal funds rate to 1/4 to 1/2 percent. The stance of monetary policy remains accommodative after this increase, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

This excerpt is from the Press Release of last week. Obviously, to get the short-term interest rate in the money market up, the many, many reserves that have been put into have to be drained. This is what the reverse repo business is all about: take reserves out of the market and put into their place interest earning assets. These will be treasury securities, repoed in a way that the interest rate matches the target. For instance, if a $100 treasury security yields 1% nominally but the target range is 0.5%, then the security is sold at $100.5 and bought back at $101. Since this is done overnight we have talk about fractions.

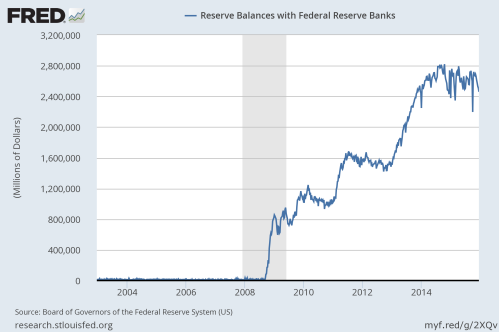

Here is a picture from FRED about the severity of the task the Fed faces:

As the Fed has explained: “the Desk anticipates that around $2 trillion of Treasury securities will be available for ON RRP operations to fulfill the FOMC’s domestic policy directive.” Given that there are also required reserves and other reasons not to go to zero, this is roughly a good fit. The Fed should have enough firepower to get where it wants to go. If not, they can always engineer more interest earning assets. Either this would be done through clever financial engineering, or by brute force: central bank bonds. Both are available without limit, so if the Fed wants to hit a target rate it can!