from the Congressional Budget Office

CBO analyzed 36 policy options commonly proposed by policymakers and analysts. Most of them would improve Social Security’s long-term finances, but only a few would significantly postpone the combined trust funds’ exhaustion date.

Social Security, which marked its 80th anniversary in 2015, is the largest single program in the federal government’s budget. The program has two parts: Old-Age and Survivors Insurance (OASI), which pays benefits to retired workers, to their dependents and survivors, and to some survivors of deceased workers; and Disability Insurance (DI), which makes payments to disabled workers and to their dependents until those workers reach the age at which they are eligible to receive full retired-worker benefits under OASI. Social Security currently has about 60 million beneficiaries. Outlays for Social Security totaled $888 billion in fiscal year 2015, accounting for nearly one-quarter of all federal spending. Although Social Security is part of the overall federal budget, its funding mechanism of dedicated revenues sets it apart from many other government programs. Benefits for OASI and DI alike are financed from trust funds (often identified collectively as the combined, or OASDI, trust funds), which are credited with tax revenues, mainly from payroll taxes, and interest on the funds’ balances.1 As long as a trust fund’s balance is sufficient to cover required payments, benefits can be paid without the need for any legislative action.

What Are the Prospects for Social Security’s Finances?

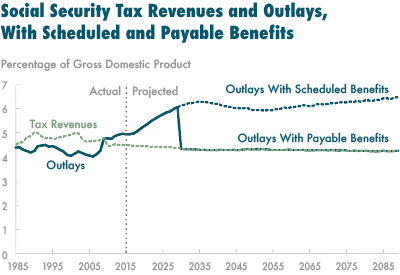

In 2010, for the first time since the enactment of the Social Security Amendments of 1983, annual outlays for the program exceeded annual revenues (excluding interest) credited to the combined trust funds. A gap between those amounts has persisted since then, and in fiscal year 2015 outlays exceeded tax revenues by almost 9 percent. As more people in the baby-boom generation retire over the next 10 years, the Congressional Budget Office projects, the gap will widen between amounts credited to the trust funds and payments to beneficiaries. If current laws governing Social Security taxes and benefits stay generally the same and if all benefits are paid in full – an assumption that underlies CBO’s extended baseline projections – outlays for the Social Security program will exceed noninterest revenues by almost 30 percent in 2025 and by more than 40 percent in 2040.

But the trust funds will not be able to sustain such spending. Under those circumstances, the DI trust fund will be exhausted in fiscal year 2021, the OASI trust fund will be exhausted in calendar year 2030, and, combined, the OASDI trust funds will be exhausted in calendar year 2029, CBO estimates.2 If a trust fund’s balance declined to zero and current revenues were insufficient to cover benefits specified in law, the Social Security Administration would no longer be permitted to pay full benefits when they were due.3 In the years after a trust fund’s exhaustion, therefore, annual outlays could not exceed annual revenues: Under those circumstances, all receipts to the trust fund would be used and the trust fund balance would remain essentially at zero.

What Effects Might Certain Changes to Social Security Have Over the Long Term?

This report considers 36 policy options that are among those commonly proposed by policymakers and analysts, divided into five groups according to the elements of the Social Security program that they would modify:

The taxation of earnings,

The benefit formula,

The full retirement age (FRA),

Cost-of-living adjustments (COLAs), and

Benefits for specific groups.

Many analysts and policymakers have suggested that Social Security could gain long-term financial stability if the gap between the system’s revenues and its outlays could be reduced through an increase in tax revenues, a reduction in benefits, or some combination of those two approaches. Although most of the options in this report would improve Social Security’s long-term finances, only a few would significantly postpone the combined trust funds’ exhaustion date because most would be phased in slowly.4 Some policymakers also advocate increasing benefit amounts, especially for people with low lifetime earnings, and a few options are designed to achieve that goal.

The effects of an option on the Social Security system’s finances are presented first, followed by a discussion of the distribution of those effects among people in various birth cohorts and according to lifetime household earnings. CBO did not analyze the macroeconomic feedback effects of the options on the federal debt, transfer payments, or payroll taxes because doing so would have involved analyses that were outside the scope of this report.

By itself, no individual option presented here could create long-term stability for the Social Security program. Some options would affect all workers or beneficiaries similarly; others would have widely disparate effects, depending on a beneficiary’s year of birth or lifetime earnings. If the goal was to achieve long-term solvency, it would be necessary to combine several options and possibly to change some of the details of various options. The combined effects of policy changes are not always additive, however, and the effects of modifying the options would not necessarily be proportional to the results presented in this report.

Source: https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/51011-SSOptions.pdf