by Zillow

Incredibly low mortgage interest rates have helped keep homes affordable for most buyers nationwide, even as home values themselves keep rising. But the days are numbered for these incredibly low rates, and while higher rates won’t necessarily be a national problem (at least, not for several years), they will definitely pose a problem in several local markets.

Currently, mortgage interest rates for a 30-year, fixed-rate loan on Zillow Mortgages hover around 4 percent, much lower than the typical interest rate of 10 percent or higher in the late 1980s. And while it is very unlikely that mortgage rates will climb back to double digits again any time soon, an increase of 100 or 200 basis points could have consequences in areas already feeling an affordability squeeze (namely, the San Francisco Bay area and Southern California).

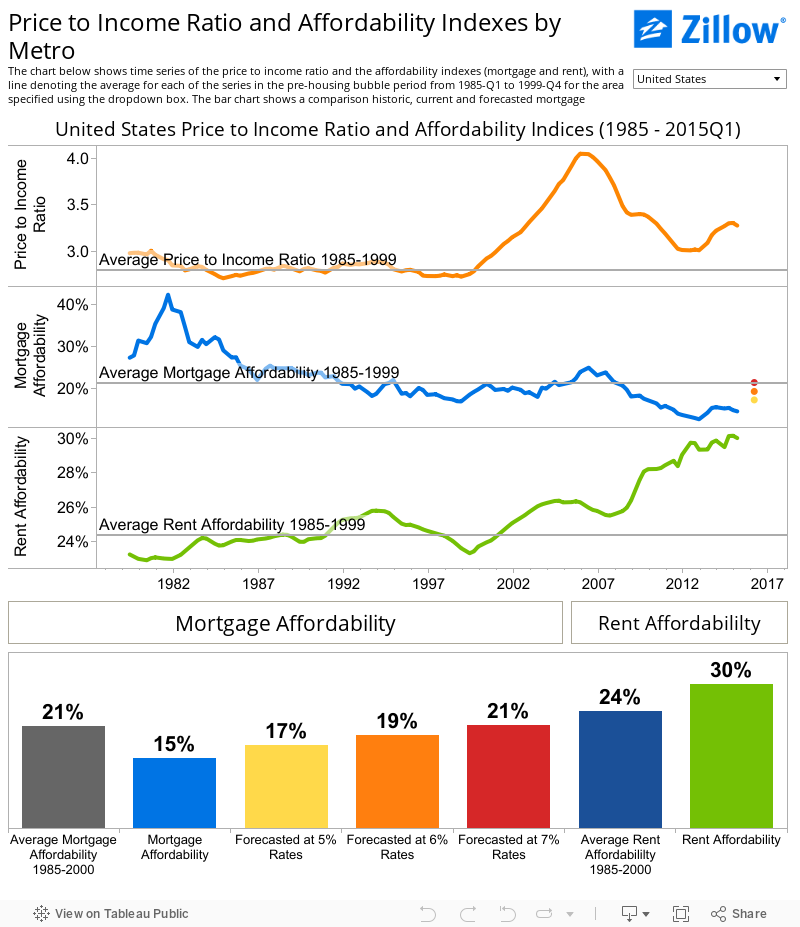

In the first quarter, potential homebuyers making the median income in the U.S. ($54,482) and purchasing the median-valued home ($178,400) would need to spend a little less than 15 percent of their income on mortgage payments, assuming prevailing rates on a 30-year, fixed loan and a 20 percent down payment. Historically, buyers could expect to spend about 21 percent of their income on a typical mortgage. Low mortgage interest rates help keep monthly payments low, and rates would need to rise to roughly 7 percent before buyers nationwide would be back to spending a comparable share of income on a mortgage as they have historically.

Nationwide and in most markets right now, there’s plenty of headroom for rates to grow without impacting affordability too much. But affordability is a story best told at the local level.

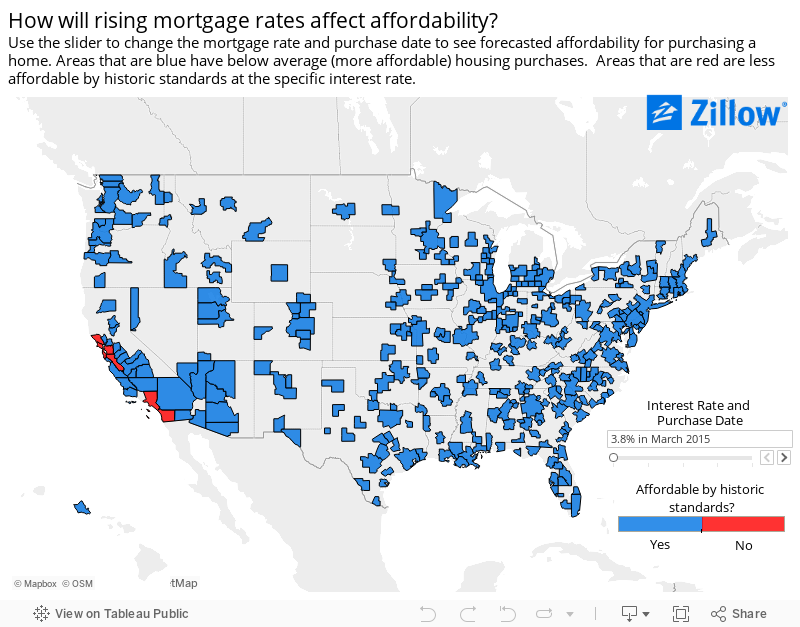

Of the 174 metro areas where both current and historic data is available, we found five where homebuyers in the first quarter of 2015 would already be paying higher percentages of their income towards their mortgage compared to historic standards. And all five – Los Angeles, San Francisco, San Diego, San Jose and Santa Rosa – are located in California. In these areas, any increase in mortgage rates – however modest – will only make home buying even more expensive relative to historic norms than it already is.

Rising home values and higher mortgage rates will make buying a home less affordable. If home values rise in each metro according to the March 2016 Zillow Home Value Forecast, and mortgage rates hit 5 percent, buyers in 25 metro areas would need to spend a higher percentage of their income on a typical mortgage compared to historic standards. If homes appreciate at that pace and mortgage interest rates rise to 6 percent, the number of markets that will be less affordable than their historic norms suggest rises to 52. At 7 percent interest rates and assuming the same home value growth, 91 markets will become less affordable than their historic standards.

Something’s Gotta Give

In the city of San Francisco, the median home value is more than $1 million. Assuming a 20 percent down payment and the current prevailing interest rate of 3.77 percent in Q1, a mortgage payment right now amounts to about $3,714 a month. If rates rose 100 basis points, that payment would rise to $4,183 (or 12.6 percent). A rise of 200 basis would bring the monthly payment to $4,679, almost $1,000 more per month than it is currently.

This also ignores any gains in home values, which would make buying a home even more expensive.

If home prices and rents continue to rise in the already unaffordable markets, and income growth fails to keep pace, at some point buyers will be unable to qualify for mortgages, or unwilling to pay the steep costs necessary to obtain one. If and when this happens, we would expect home value growth to slow further in many areas, or potentially fall outright.

But while affordability is a real issue in certain high-priced and already unaffordable markets (by historic standards), the affordability picture looks drastically different across the country. Even if mortgage rates rose to 7 percent next year, the share of income needed for a mortgage payment would remain below historical averages in many large metro areas, including Chicago, Dallas, Philadelphia, Atlanta and Minneapolis.

Use the interactive tool below to change the interest rate and see which metros move from being affordable to less affordable, noted by a change in the shaded color.

What About Renters?

While the picture for buyers may turn bleak in the future, it’s fairly positive now and for the foreseeable future (rates aren’t expected to reach 7 percent until2018 at the earliest, according to most forecasts). But for renters, monthly rents are largely unaffordable today, making it harder for would-be buyers to save for a suitable down payment. Nationwide, renters need to spend a hair less than 30 percent of their income to afford to rent the median home, compared to a historic average of roughly 24 percent. Furthermore, growth in rents has now outpaced growth in home values, a trend we expect to continue for some time.

In other words, the rental affordability problem likely won’t get better any time soon, at least not without significant income growth to help balance out higher rents.

Methodology

To calculate mortgage affordability, we first calculate the mortgage payment for the median-valued home in a metropolitan area by using the metro-levelZillow Home Value Index for a given quarter and the 30-year fixed mortgage interest rate during that time period, provided by the Freddie Mac Primary Mortgage Market Survey (based on a 20 percent down payment). Then, we consider what portion of the monthly median household income (U.S. Census) goes toward this monthly mortgage payment. Median household income is available with a lag. For quarters where median income is not available from the U.S. Census Bureau, we calculate future quarters of median household income by estimating it using the Bureau of Labor Statistics’ Employment Cost Index.

The affordability forecast is calculated similarly to the current affordability index but uses the one year Zillow Home Value Forecast instead of the current Zillow Home Value Index and a specified interest rate in lieu of PMMS. It also assumes a 20 percent down payment.

We calculate rent affordability similarly to mortgage affordability; however we use the Zillow Rent Index, which tracks the monthly median rent in particular geographical regions, to capture rental prices.

About the Author

Meredith Miller is a Research Analyst at Zillow. To learn more about Meredith, click here.

Source

http://www.zillow.com/research/q1-2015-rent-mortgage-affordability-10067/