by Zillow

Generally, the black homeownership rate is considerably lower than the white homeownership rate. But why? The full answer is difficult to determine based purely on economics.

Black and white households differ in many ways, including income, age and education, all of which might help explain some of their differences in homeownership. But some of the gap in homeownership rates might not be explained by demographic and economic factors and might be due to more pernicious causes like racism in the mortgage process, or cultural differences.

To untangle this thorny issue, we examined statistically how much of the difference in homeownership rates can be explained by differences in economic characteristics, and how much remains unaccounted for by economics and demographics and might instead be attributable to those more insidious causes.

To do this, we created a model to estimate the probability of owning a home given the race of the household’s head, along with a variety of socioeconomic and demographic characteristics, including:

- Year

- Age of head of household

- Income

- Number of children

- Number of adults

- Education of head of household

- Education of spouse

- Marital stats

- Inheritance

- Number of vehicles

There are some important variables missing from the equation. For example, we don’t know the credit score of mortgage applicants, a key factor in determining whether they can or will buy a home. That being said, over time, one would expect two different groups would generally have similar credit and purchase homes at a similar rate when controlling for differences in incomes.

This model allows us to answer the following question: Statistically, how high would we expect the black homeownership rate to rise if the average income, education and all the other variables above were at the same level as they are for white households? That is – how much of the difference in homeownership rates can be explained purely as a result of demographic and socioeconomic differences between the groups? The results are summarized below.

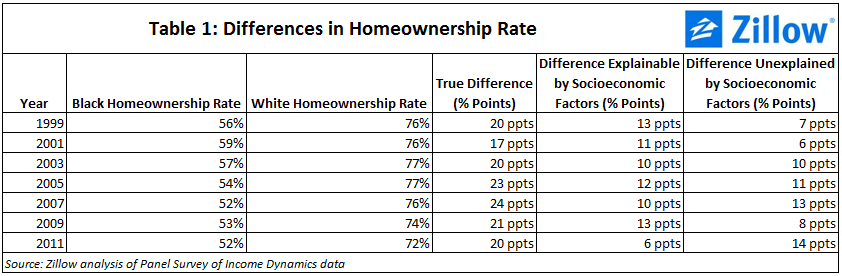

In every year modeled, those demographic and socioeconomic differences can explain some of the difference in homeownership rates, but most of it remains unaccounted for. For example, in 2011, the gap between the black and white homeownership rate in the U.S. was 20 percentage points. But only 6 percentage points of that gap can be explained as a result of demographic and socioeconomic differences between the black and white households – the remainder of the gap remains unexplained by observable data.

Interestingly, while the overall gap between black and white homeownership has remained fairly stable at roughly 20 percentage point over the years, the portion of that gap which can be explained by socioeconomic factors has declined from 13 percentage points in 1999 to 6 percentage points in 2011.

Where this gap originates is difficult to quantify. This gap could come from a variety of sources, including discrimination in the mortgage market and differences in preferences for owning homes. Unfortunately, these factors are hard to observe directly, making distinguishing between them difficult. But clearly understanding what drives this gap will be critical if we are ever going to close racial disparities in homeownership.

Methodology

Using the Panel Survey of Income Dynamics to build a penalized logistic model, we trained on a random sample of 80 percent of the sample and tested the accuracy on the remaining 20 percent of the data. People having no or negative income or wealth were excluded, as were those in the top 1 percent of income and wealth.

About the Author

Cody Fuller is an Economic Analyst at Zillow. To read more about Cody, click here.