by Zillow

The decision to buy a home or rent is very personal, and depends heavily on your distinct social circumstances and financial situation. But we have found that a rough idea for when buying a home may become better than renting it can help inform the choice, especially when so much emotion and so many moving pieces are involved.

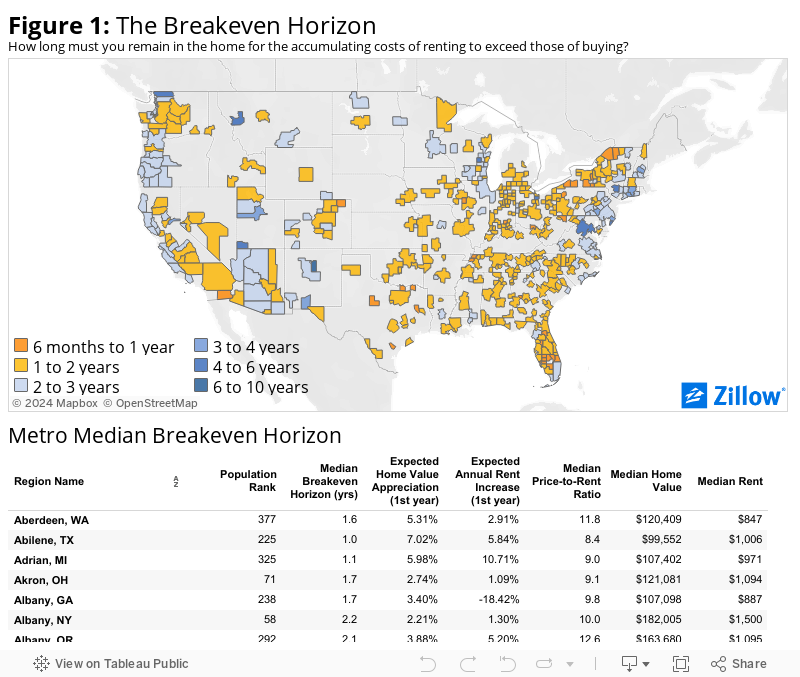

Zillow’s Breakeven Horizon estimates the number of years you would have to live in a home before buying it would become more financially advantageous than renting it. We make some basic assumptions[i] and bake in common costs associated with renting and buying, including down payments, security deposits, taxes and fees. The result is a comprehensive look at how long you’ll need to stay in a home in a given area before the total costs of renting, offset by investments in stocks or bonds, surpass the costs of owning as equity builds (figure 1).

For example potential buyers looking to buy a home in the Washington, D.C., area, should expect to stay in that home for 4.5 years before buying it will become more financially advantageous than renting it. Potential buyers in the Dallas-Fort Worth area will only need to live in a home for 1.1 years before the costs associated with renting overtake the costs associated with owning that home. Nationwide, the breakeven horizon (on a median-valued U.S. home) is currently 1.9 years.

General rules of thumb say that if you’ll only live in a home for a short time, it’s cheaper to rent. And in many cases – but not all – those rules hold true (depending on your definition of a “short” time frame). Buying a home often requires very large upfront costs in a down payment and closing costs, and significant investments over time in taxes and maintenance.

In a healthy market, you’ll get your down payment back in the form of home equity over time. Yes, transaction costs, property taxes and mortgage interest payments (among other costs) are gone forever. But as time goes by, your home’s value will typically grow, and a larger and larger share of your monthly mortgage payments pay down the principal on your loan. Growing home equity, over time, offsets many costs.

Rent, like some of the costs of homeownership, is also paid and gone for good. But as a renter, there is opportunity to invest the savings you otherwise would have used to purchase a home in a different asset, like stocks or bonds. The gains realized from these assets can often offset monthly rent payments.

But remember – everyone’s circumstances are different, and there is no universal right or wrong answer that will work for all of us.