by Congressional Budget Office

The long-term outlook for the federal budget has changed little since last year, according to CBO’s projections. If current laws remained generally unchanged in the future, federal debt held by the public would decline slightly relative to the economy’s annual output, or gross domestic product (GDP), over the next few years, CBO projects.

After that, however, growing budget deficits – caused mainly by the aging of the population and rising health care costs – would push debt back to, and then above, its current high level. The deficit would grow from less than 3 percent of GDP this year to more than 6 percent in 2040. At that point, 25 years from now, federal debt held by the public would exceed 100 percent of GDP. (Federal debt is now equivalent to about 74 percent of GDP, a higher percentage than at any point in U.S. history except a seven-year period around World War II.)

Moreover, in 2040, debt would still be on an upward path relative to the size of the economy. The rising debt could not be sustained indefinitely; the government’s creditors would eventually begin to doubt its ability to cut spending or raise revenues by enough to pay its debt obligations, forcing the government to pay much higher interest rates to borrow money.

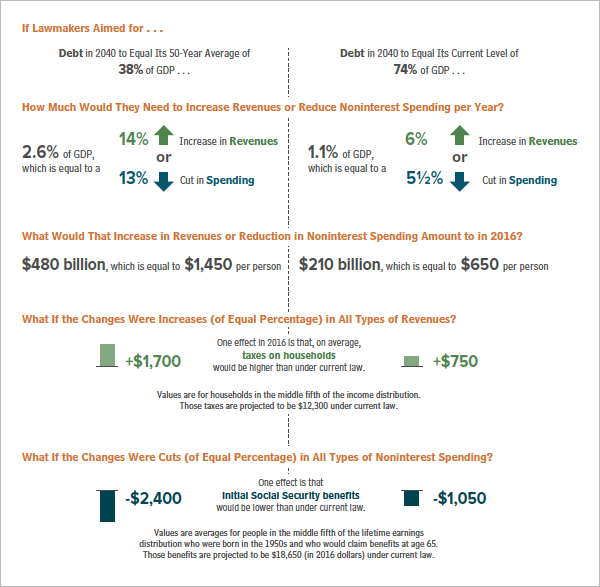

One way to measure the long-term fiscal imbalance is to assess the changes in revenues or noninterest spending that would be needed to achieve a chosen goal for federal debt. For example, if lawmakers wanted debt in 2040 to equal its current level of 74 percent of GDP, they could increase revenues or cut noninterest spending, relative to outcomes under current law, by a total of 1.1 percent of GDP each year starting in 2016 – an amount equal to $210 billion in that year (see figure below). If they chose only to cut noninterest spending, that spending would have to be 5½ percent lower than CBO currently projects in each of the next 25 years. Alternatively, if they chose only to increase revenues, those revenues would have to be 6 percent higher each year than projected. Reducing debt to the average percentage of GDP seen over the past 50 years (38 percent) would require changes in spending or revenues more than twice as large.

Budgetary outcomes are uncertain, however. They would undoubtedly differ from CBO’s projections – even if future tax and spending policies matched what is specified in current law – because of unexpected changes in the economy, demographics, and other factors. Nonetheless, CBO’s analysis shows that the main implication of this testimony applies under a wide range of possible values for some of those factors. That is, if current laws remained generally unchanged, federal debt, which is already high by historical standards, would probably be at least as high as it is today and would most likely be much higher.