Written by Yichao Wang, GEI Associate

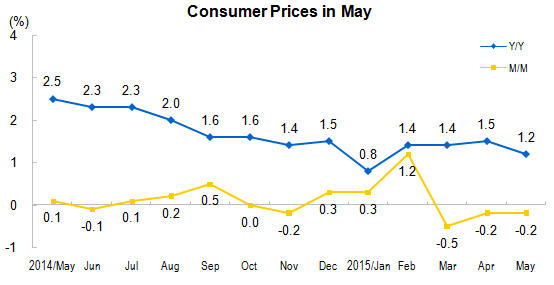

According to China’s National Bureau of Statistics, China’s consumer-price index (CPI) rose 1.2% in May from a year earlier, slower than the 1.5% increase in April. The producer-price index (PPI) dropped 4.6% in May from a year earlier, extending declines of 39 consecutive months.

Both CPI and PPI are worse than market expectations. Subdued CPI inflation and sinking factory prices reflect the still weak domestic demand and rising risks from deflation. The data also raised concerns that China might be following in the footsteps of Japan, where a decade-long fall in consumer prices has dragged on economic growth. As many analysts believe, the latest data will likely keep the pressure on Beijing for further policy easing to avert a sharper economic slowdown and deflation.

However, there are several reasons showing that China is near the end of the rate-cutting cycle.

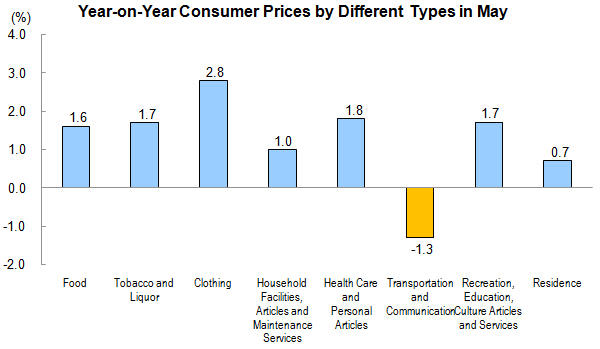

First of all, CPI is likely to rebound over the coming quarters. Because premier Li Keqiang urged lower internet-related fees last month, transport and telecommunication prices declined 1.3% year-on-year, dragging down the CPI in May. On the other hand, food prices in May actually rose 1.6%. Due to a sharp drop in pig numbers in recent months, pork prices are expected to rise. As one of the key swing factors in China inflations, pork price would help consumer price to strengthen in the following months. Moreover, the sharp fall in global commodity prices starting over a year ago also provide a much weaker base for comparison, assuaging the concerns over deflation.

Secondly, there are expectations that the U.S. Federal Reserve will begin to raise interest rates as the U.S. economy regains its footing. China’s capital outflows have been continuing for more than a year. The expectations of higher U.S. rates would lead more capital outflows as investors seek better returns in U.S. dollar assets. Therefore, this could lower Beijing’s willingness to cut interest rates.

Thirdly, in order to boost lending and stimulate the economic growth, China has already cut interest rates three times and lowered the reserve requirement ratio twice. Nevertheless, the measurable impact of the easings can only be found in the stock market, which has more than doubled since China began cutting interest rates in November. Although the wealth effect of the stock market can boost the overall economy, it is less likely for China to cut the interest rate too much due to the growing concerns about a market bubble.

Furthermore, a series of readings suggest that China’s economy appears to be stabilizing. According to the National Bureau of Statistics, value-added industrial output in China ticked up to 6.1% year-over-year in May. Banks issued 900.8 billion yuan ($145.3 billion) of new loans in May, compared with 707.9 billion yuan in April. China’s housing sales in the first five months of the year rose 5.1% over year-earlier levels, reversing the 2.2% decline seen in the first four months. Industrial profits rose year-over-year in April, reversing a six-month decline.

Therefore, although there could be one more rate cut, as some analysts predict, the central bank might call a halt to its rate-cutting efforts later this year.