Written by Yichao Wang, GEI Associate

The People’s Bank of China (PBOC) lowered the reserve requirement ratio (RRR) by 1% to 18.5% on April 20. This reduction injects over 1.2 trillion Chinese yuan (US$194 billion) of new liquidity which could boost lending. It is already the second industry-wide cut in less than three months, following the 0.5% cut in late January.

It is also the biggest RRR-cut for China since the global crisis of 2008. The amplitude of the reduction is unusually large. The weak growth in industrial output, capital outflows as well as disinflation has certainly caused concerns.

Limited effect

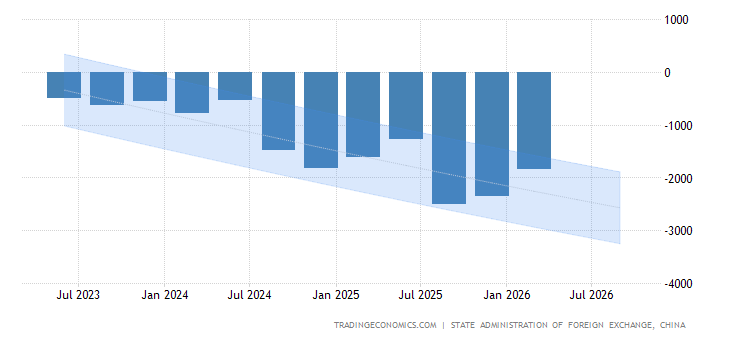

As China’s economy cools, there is more capital fleeing china. Data released by the State Administration of Foreign Exchange (SAFE) shows that the foreign exchange settlement deficit was $91.4 billion in the first quarter. Moreover, the central bank and commercial banks had sold a net 156.5 billion yuan ($25.3 billion) worth of foreign exchange in March, the most in at least a year. These data suggests that Capital is leaving China. In response, the reduction increases the money multiplier and offsets increasing capital outflows that created a contraction in the monetary base.

However, it would have a limited effect in China’s economic growth. With regard to companies, borrowing costs is still high, while demand and producer pricing power remain weak. Therefore, the reduction could cause people to respond in the short term; but in the long term, people could remain negative about embarking on fresh investments.

As for banks, they are cautious about making loans to small and medium enterprises, which are considered as higher credit risks. Even though Beijing urges banks to boost lending to real economy, banks could remain wary due to the growing downward pressure on the economy.

Although RRR cut would increase the amount of money that Chinese banks can lend out, it won’t boost economic activity effectively because China is facing problems of demand rather than supply. Without further regulatory reform or enforcement, the money released by the reserve requirement ratio cut could only lead to a speculative asset bubble, like the current parabolic move of the stock market in the stock market.

Expectation for further RRR cut

According to Economic Daily (a Chinese newspaper), Lian Ping, the chief economist at Bank of Communications, said that in order to achieve 12.5% M2 growth in 2015, more than 1 trillion yuan is needed. Therefore, PBOC needs to cut 1% RRR again this year. Related to this, China’s central bank Governor Zhou Xiaochuan also said in a brief interview that China still has room in the reserve ratio.

Although the reduction just made was surprisingly aggressive, the reserve requirement ratio is still relatively high compared with international standards. Moreover, China is facing several economic challenges that create a drain on the money supply: Capital outflows, bank deposit growth rate declines, while internet finance and stock market are attracting more and more active deposits. Therefore, monetary easing is necessary to contain disinflation, to maintain adequate interbank liquidity and to provide stable base money growth. Meanwhile, China does not want to relax credit too aggressively, which would worsen the debt problem. As a result, POBC is more likely to further cut RRR.