from Voxeu.org

— this post authored by George Alogoskoufis

Greece experienced a deep recession in 2020, and pandemic relief measures have led to further increases in its exorbitantly high public debt. This column outlines three potential methods for dealing with increasing debt after the crisis: (1) increases in taxation/reductions of government spending, (3) debt restructuring and (partial) debt write-offs, or (3) a policy of ‘gradual adjustment’ in which economic growth helps the debt burden shrink relative to GDP over time. The precise policy mix will involve significant coordination among euro area countries, but Greece must also implement domestic reforms to facilitate a dynamic and sustainable recovery.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Like the rest of the world, the Greek economy has entered into another deep economic recession in 2020. While the economy appeared to be on a modest recovery from its ‘great depression’ of 2010-2016, it was hit by a new major international economic shock due to the Covid-19 pandemic.

Greece appears to have experienced a very deep recession in 2020 and even under optimistic assumptions, a full recovery will take some time beyond 2021. In addition, the recession and the cost of the measures to mitigate it have already led to a further sharp rise of Greece’s already exorbitantly high public debt.

As for every other country, the immediate problem is how to deal with the health and short-term economic effects of the pandemic. This will become a little easier, due to the inflow of additional funding through the new Recovery and Resilience Facility of the EU, but there is little doubt that Greece’s high debt-to-GDP ratio will increase further.

Increasing public borrowing in order to support the economy in the short term is certainly the right solution, both globally and for Greece. However, the increase in borrowing shifts many of the problems to the future. As in the aftermath of wars, in the aftermath of a major economic downturn such as the current recession, every country must tackle the problem of debt repayment, or at least the reduction of its public debt-to-GDP ratio.1

So how does Greece pay for the cost of the pandemic? By analogy, the question is similar to the question in Keynes’ famous 1940 essay on ‘How to Pay for the War’.

There are three alternative methods of dealing with a large increase in public debt such as the one that is taking place during this crisis. First, is the significant increase in taxation and reduction of primary government spending immediately after the end of the crisis, through a policy of ‘austerity’. The second is the restructuring or even the partial write-off of the debt. The third is ‘gradual adjustment’, which is effectively the continuous postponement of significant debt reduction, with the hope that the debt will gradually shrink in relation to GDP through economic growth and inflation.

Greece experienced austerity mainly in the period between 2010 and 2018. The global crisis of 2007-2009 led to an increase in Greece’s public and external debt ratios. The austerity of the period 2010-2018 led to a Greek ‘great depression’. Due to the ‘great depression’, the debt-to-GDP ratio shot up instead of falling, despite the significant and front-loaded fiscal adjustment. From 103% of GDP in 2007, at the beginning of the 2007-2009 crisis, and 127% of GDP in 2009, in 2018, with the end of the adjustment and austerity programs, public debt had skyrocketed to 186% of GDP. Despite the huge costs paid by workers, the self-employed, retirees, and the unemployed, the effects of austerity on public debt have been disappointing.

Figure 1 shows how Greece’s debt usually rises in periods of recession and stagnation and is only stabilised in periods of recovery and growth. The debt-to-GDP ratio rose along with unemployment during the recessions of the early 1980s and the long period of stagnation until 1993, and then rose again significantly during the global crisis of 2007-2009 and the Greek ‘great depression’ of 2010-2016.2

Figure 1 Public debt and unemployment during periods of growth, stagnation, and recession in Greece

Greece also experienced the second method of dealing with debt, the restructuring and partial write-off of its debt, in 2012. Despite the concomitant problems, the results were somewhat better. There was a temporary halt to the rising debt and the cost of servicing it was reduced, resulting in more benign debt dynamics. In addition, the cost was paid by holders of Greek government bonds and the shareholders of Greek banks, presumably wealthier than the low-paid, the pensioners, and the unemployed.3

However, it is doubtful whether this can be repeated in the current context. First, a large part of Greece’s debt is now official debt held by other sovereigns through the ESM. Second, the debt problem created by the current crisis is global and does not only affect Greece or the peripheral economies of the euro area, as during 2010-2011. It is highly unlikely that the core euro area economies will risk losing their credibility to current and future investors through debt restructuring or write-offs, or whether, given the rise in their own public debt, they will accept to shoulder part of the cost of debt restructuring of economies of the periphery such as Greece.

This leaves us with the third method, that of ‘gradual adjustment’. This is how the public debt of the US, Britain, and other European economies fell relative to GDP after WWII. This is also the way in which Greece had stabilised its debt-to-GDP ratio during the 1994-2007 period of recovery and growth. However, this solution has an important pre-condition: The nominal yield of government bonds must remain lower than the sum of GDP growth and inflation for a relatively long period.

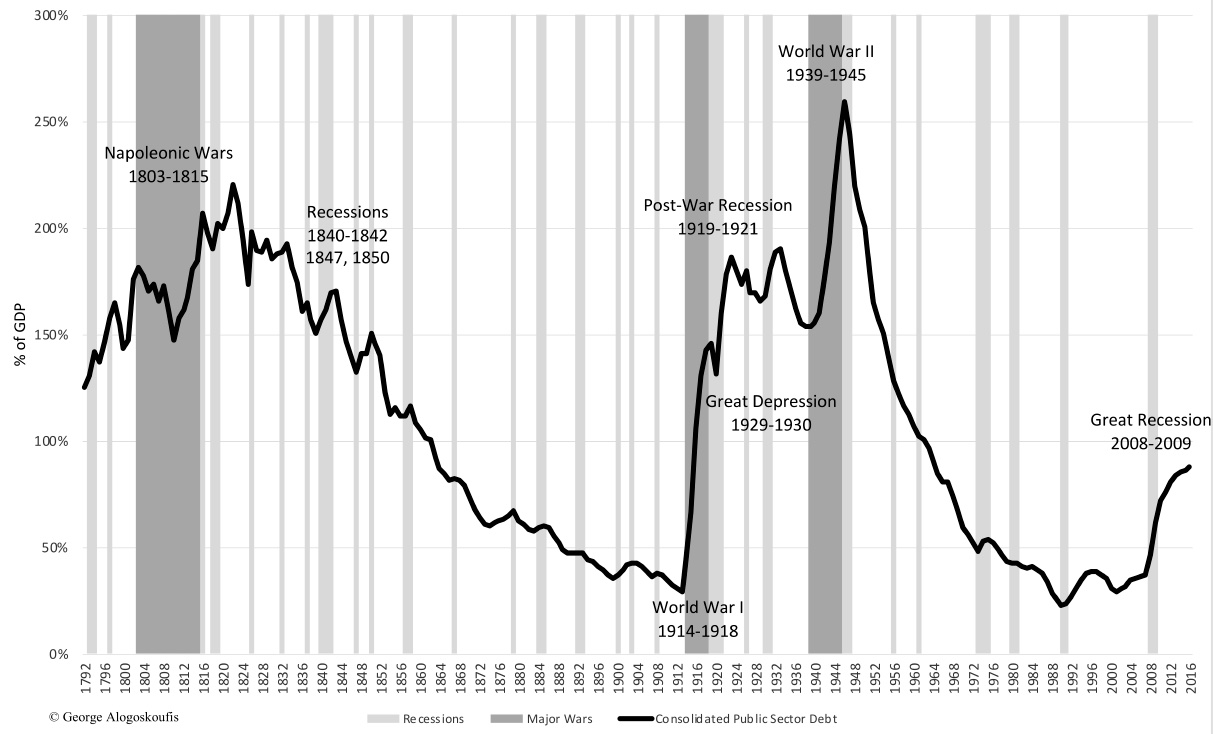

Figure 2 Public debt, wars, and recessions in Britain, 1792-2016

In the first thirty years of the post-war period this was achieved internationally through rapid economic growth and ‘financial repression’. The latter required significant state intervention in financial markets and capital controls in order to keep interest rates low.

In the case of Greece during 1994-2007, this was achieved through the reduction of interest rates and the economic recovery caused by the so called ‘convergence play’, i.e. the prospect of joining the euro area and then through euro area participation itself. Interest rates fell rapidly and remained low because of the significant reduction of the risk and devaluation premium and inflationary expectations. This caused an increase in both consumption and investment and acceleration of economic growth. Unfortunately, it also caused a persistent widening of the current account deficit, which was the root cause of the debt crisis of 2010 (Baldwin and Giavazzi 2015, Gourinchas et al. 2016, Alogoskoufis 2012, 2021).

The ‘gradual adjustment’ method has proven to be very effective in tackling large increases in public debt for the major industrial economies, usually after wars or deep recessions. Britain’s experience after the Napoleonic Wars and WWII, as shown in Figure 2, is a prime example. On the contrary, the austerity after WWI or after the Great Recession of 2008-2009 led to further increases in the debt-to-GDP ratio of Britain.

Can a policy of ‘gradual adjustment’ after the current crisis be successful in an age of liberalised financial markets and capital movements? If it could, a significant part of the cost of the adjustment would be passed on to the presumably richer investors in government bonds, as well as to future generations, who would have had the benefits of higher economic growth. The problem is whether interest rates can remain low for the long period of time required for ‘gradual adjustment’ to succeed. This may require a policy of interventions in financial markets, in addition to the accommodating monetary policy of central banks. In addition, this solution carries the risk that economies will remain vulnerable for a long time to the risk of a new financial crisis. Obviously, Greece would not be able to implement such a policy on its own. This would require the adoption of a common ‘gradual adjustment’ policy for the whole of the euro area.4

In conclusion, these are the three options for Greece to deal with the increase in its debt after the current crisis. None of the three is painless and each has different redistributive effects, involves different risks, and has different external prerequisites. What is certain is that when the pandemic subsides, all economies will have to tackle the debt problem with a combination of the above three methods. Greece will have to adapt its response to that of the rest of the euro area.

In any case, it is important that the Greek government does not abandon the reformist growth agenda on the basis of which it was elected in June 2019 because of the pandemic. Domestic reforms that will facilitate a dynamic and sustainable recovery after the current crisis will greatly help Greece tackle its debt problem, regardless of what is decided at the euro area level.

References

- Alogoskoufis, G (2012), “Greece’s Sovereign Debt Crisis: Retrospect and Prospect”, GreeSE Paper no. 54, Hellenic Observatory, London School of Economics, London.

- Alogoskoufis, G (2021), “The Greek Economy before and After the Euro”, Working Paper no 2-2021, Athens University of Economics and Business, Athens (forthcoming in Alogoskoufis, G and K Featherstone (2021), Greece and the Euro: From Crisis to Recovery, Hellenic Observatory, London School of Economics, London).

- Alogoskoufis, G (2019), Dynamic Macroeconomics, Cambridge, MA: MIT Press.

- Baldwin, R and F Giavazzi (2015), The Eurozone Crisis: A Consensus View of the Causes and a Few Possible Remedies, CEPR Press, 7 September.

- Bartsch, E, A Bénassy-Quéré, G Corsetti and X Debrun (2020), “Stronger together? The policy mix strikes back“, VoxEU.org, 15 December.

- Blanchard, O J (2019), “Public Debt and Low Interest Rates”, American Economic Review 109(4): 1197-1229.

- Gourinchas, P-O, T Philippon and D Vayanos (2016), “The Greek crisis: An autopsy“, VoxEU.org, 5 August.

- Micossi, S (2020), “Managing post-Covid sovereign debts in the euro area“, VoxEU.org, 20 October.

- Xafa, M (2014), “Lessons from the 2012 Greek debt restructuring”, VoxEU.org, 25 June.

Endnotes

- See Micossi (2020) on the impact of the pandemic on euro area debts and on managing the higher debt after the pandemic. Obviously, dealing with higher debt is not a problem only for Greece.

- For the euro area crisis and its aftermath see Baldwin and Giavazzi (2015). For Greece before and after the euro see Alogoskoufis (2021), on which this article is based.

- See Xafa (2014) for an analysis of the details of Greek debt restructuring.

- Blanchard (2019) discusses theoretical issues of public debt management under low interest rates. Bartsch et al. (2020) discuss the global fiscal-monetary policy mix following the pandemic.

About The Author

Georgios Alogoskoufis is a Professor of Economics at the Athens University of Economics and Business. He was a member of the Hellenic Parliament from September 1996 till October 2009 and served as Greece’s Minister of Economy and Finance from March 2004 till January 2009

Georgios Alogoskoufis is a Professor of Economics at the Athens University of Economics and Business. He was a member of the Hellenic Parliament from September 1996 till October 2009 and served as Greece’s Minister of Economy and Finance from March 2004 till January 2009

This article appeared on Voxeu.org 23 February 2021.

.