by Philip Pilkington

Article of the Week from Fixing the Economists

Back in 2013 a friend of mine, Rohan Grey (founder of the excellent Modern Money Network), directed me to the work of Columbia law professor Katherina Pistor. Pistor’s work seems to be getting a lot of attention, having won the Max Planck research award. Having looked into it a bit I can safely say that Pistor “gets it” to a far greater extent than most economists.

Please share this article – Go to very top of page, right hand side, for social media buttons.

To get an idea of what her work is all about I suggest watching this relatively short INET presentation (Pistor’s presentation starts around the 5 minute mark);

Pistor thinks that the manner in which we are regulating financial markets – with its emphasis on reducing transaction costs and information disclosure – is entirely wrong. I totally agree and what I find so interesting about Pistor’s work is that she recognises at a very fundamental level why regulators and economists are inclined to think otherwise.

At the start of her talk Pistor presents a basic supply and demand graph and says that this is how regulators and economists think of financial markets. She is absolutely correct. Even those theories that allow for disequilibria in markets – like the noise trader theory that I discussed in this post – take as their underlying structural principle the idea that markets are basically or even “naturally” efficient and will tend toward market equilibrium.

As I argued in the above post, this bias that is inherently built into the theory blinds economists, regulators and policymakers to the actual nature of such markets which is that they are, as Pistor says, inherently crisis-prone and hierarchical. Thus having regulations that basically focus on trying to allow markets to reach their supposedly “natural” equilibrium position will likely fail spectacularly.

What economic theory needs to do is to exorcise this specter of market equilibrium altogether. I have discussed how this might be done on this blog before, but let me elaborate a little further taking as a starting point Pistor’s presentation.

There are, as alluded to above, two components to Pistor’s criticism: (i) markets are inherently crisis-prone and (ii) markets are inherently hierarchical. Let’s deal with each aspect in turn.

If we concede that markets are inherently crisis-prone we must admit that they do not tend toward efficient market equilibrium positions. Think about that for a moment. Yes, theories like the noise trader theory – and there are other lesser known but similar theories which I will not discuss here – can account for bubbles and fluctuations in markets, but they tend to conceive of these as small ripples on an otherwise calm ocean.

This is because, in contrast to Pistor, they conceive of markets as being inherently stableand any crises that arise are anomalies (likely caused by some sort of anti-market process that can be regulated away). If we take as our basic precept, however, that markets are inherently unstable then we have to drop the assumption that they tend toward an efficient equilibrium.

The problem is that economists have internalised the efficient equilibrium bias to such an extent that they tend to view it simply as a methodological tool and not an a prioriassumption about the nature of markets which is what it actually is. There were a few economists who recognised how the underlying idea of efficient equilibrium is far more than simply a methodological tool, but they are few and far between. In her excellent The Accumulation of Capital Joan Robinson, for example, wrote:

[We cannot] apply the metaphor of a balance which is seeking or tending towards a position of equilibrium though prevented from actually reaching it by constant disturbances. In economic affairs the fact that disturbances are known to be liable to occur makes expectations about the future uncertain and has an important influence upon any conduct (which is, in fact, all economic conduct) directed toward future results. For instance, [financial asset] owners (and their professional advisers) are always on the look-out to buy what will rise in value. A belief that a particular share is going to rise causes people to offer to buy it and so raises the price … This element of ‘thinking makes it so’ creates the situation in which a cunning guesser who can guess what the other guessers are going to guess is able to make a fortune. There are no solid weights to give us an analogy of a pair of scales in balance. (p59).

The first step that needs to be taken if we are to reform the theory of financial markets is that we must throw out the idea of efficient market equilibrium. If we do not, it will continuously come back to haunt us. The problem is that very few economists seem to be able to understand that this idea is not merely a methodological tool but rather a normative bias about the supposed “nature” of markets that deeply affects how we conceive of them.

The second aspect of Pistor’s criticism is tied to this. What she means when she says that markets are inherently hierarchical is that there exist a network of institutions that affect the capacity of various players in financial markets. She takes as her example the Federal Reserve and claims, rightly, that we can understand the hierarchy of the financial markets by looking at its balance sheet since the 2008 crisis. Here is the balance sheet (click to enlarge):

As Pistor says in her talk, an underwater homeowner cannot hand their mortgage over to the Fed in order to ensure their solvency, but if you’re a big bank about to go under you have all sorts of options at hand.

Although at first glance this has little to do with the idea of equilibrium, I would argue that it does. What the Fed does in times of crisis is that it chooses certain asset classes and then uses its money creation abilities to pump the value of these assets up to what it considers to be an appropriate price. There is an equilibrium process underlying this process, but not a market equilibrium one.

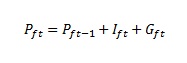

What is happening is that private sector investment is falling for some assets and central bank investment is piling in to stabilise the price. We can represent this algebraically in a very similar manner as we might the Keynesian income-determination process. Consider that price is set by investment either by the private sector, If, or by the central bank, which we will here call the government sector, Gf. Then:

To be crystal clear, that says that price, Pft, is determined by the price in the previous time period, Pft-1, private sector investment, Ift, and government investment, Gft.

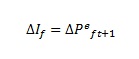

Now, let’s further say that the change in private investment is determined by expectations of future price changes. Then:

Again, what that equation says is that the change in private investment is determined by the expected future change in the price. I.e. if the future price is expected to fall, private sector investment will fall and if the future price is expected to rise, private investment will rise.

I have to say that I am oversimplifying here massively. The process is actually much more complicated than this, but I’m really just interested in bringing out the basic structure of what is going on here.

Okay, that said, let’s lay out what determines the equilibrium price, Pft*.

As we can see – and again, we are massively oversimplifying here – the equilibrium price is determined (a) based on the expectations among investors of future price increases/decreases and (b) government, in this case central bank, action. Here is the key point: the equilibrium outcome is not a market equilibrium outcome; rather it is a stock-flow equilibrium outcome. The equilibrium price is purely determined by investment flows into the asset; just like income is determined in the Keynesian system by investment and consumption flows.

This is what I’m working on (in a far more complex way) for my dissertation. What I think is key to expanding our understanding of financial markets is to overthrow the bias inherent in the market equilibrium view. By introducing a stock-flow equilibrium framework we can see that these markets (1) are inherently unstable and dependent on expectations and (2) determined by investment flows that have an irreducible institutional element. This, I think, is how economists can begin to integrate and talk about work like Pistor’s.

.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>