Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

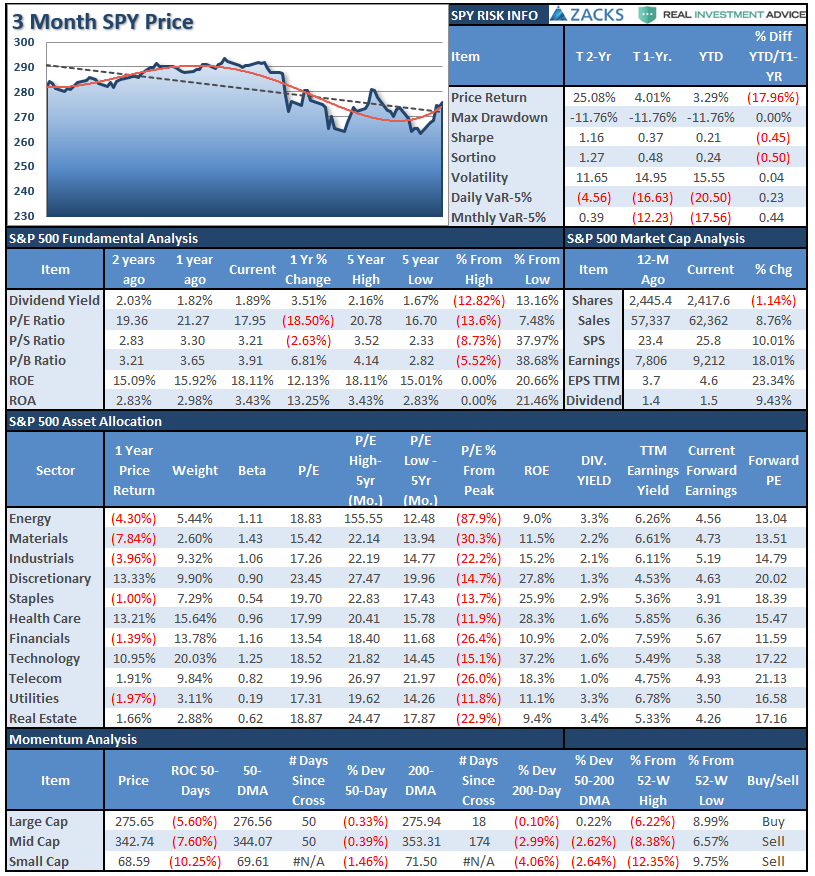

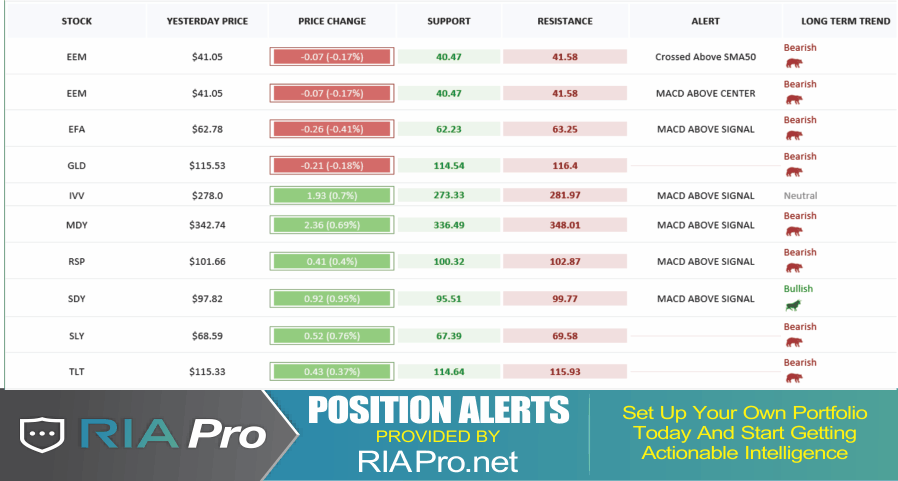

S&P 500 Tear Sheet

Performance Analysis

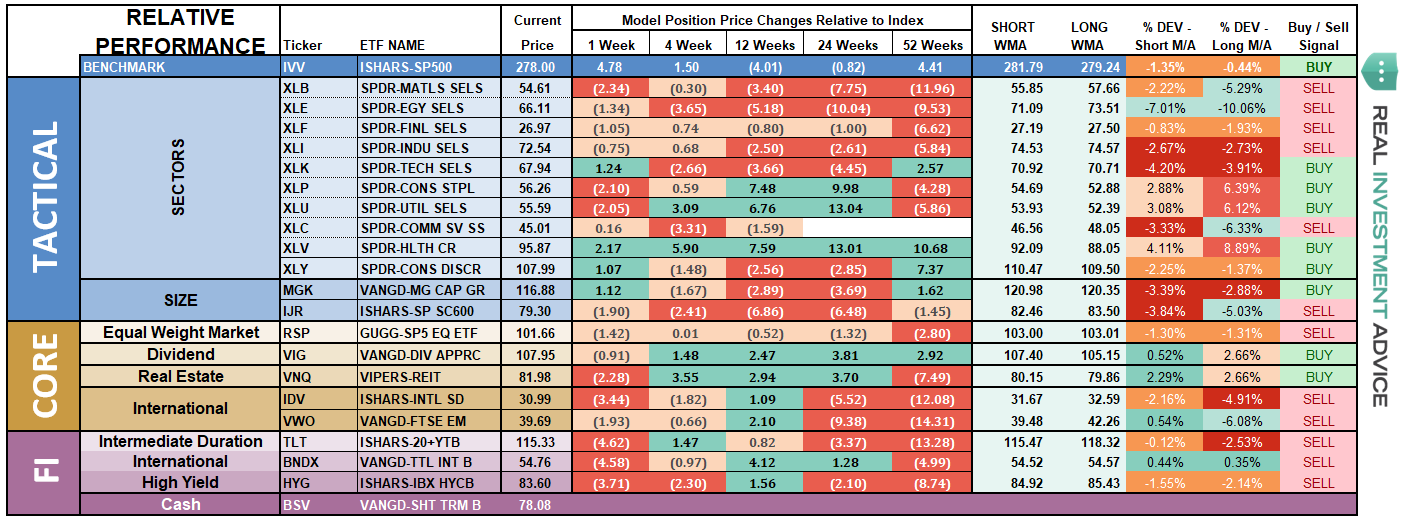

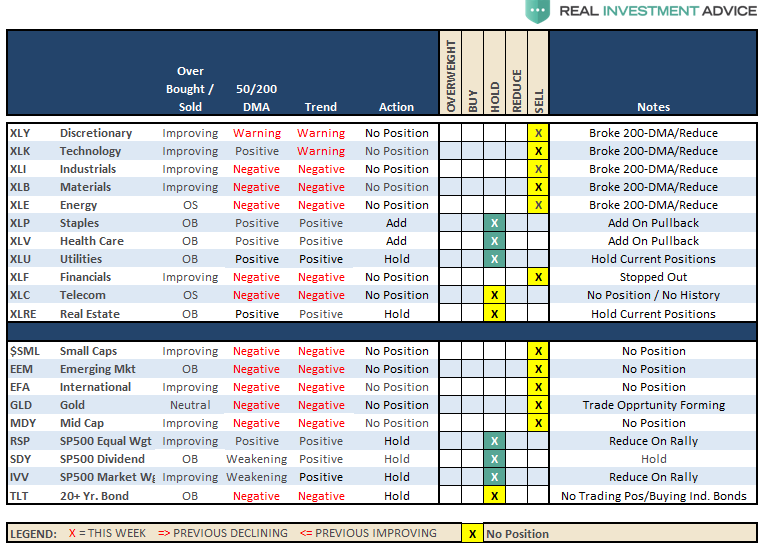

ETF Model Relative Performance Analysis

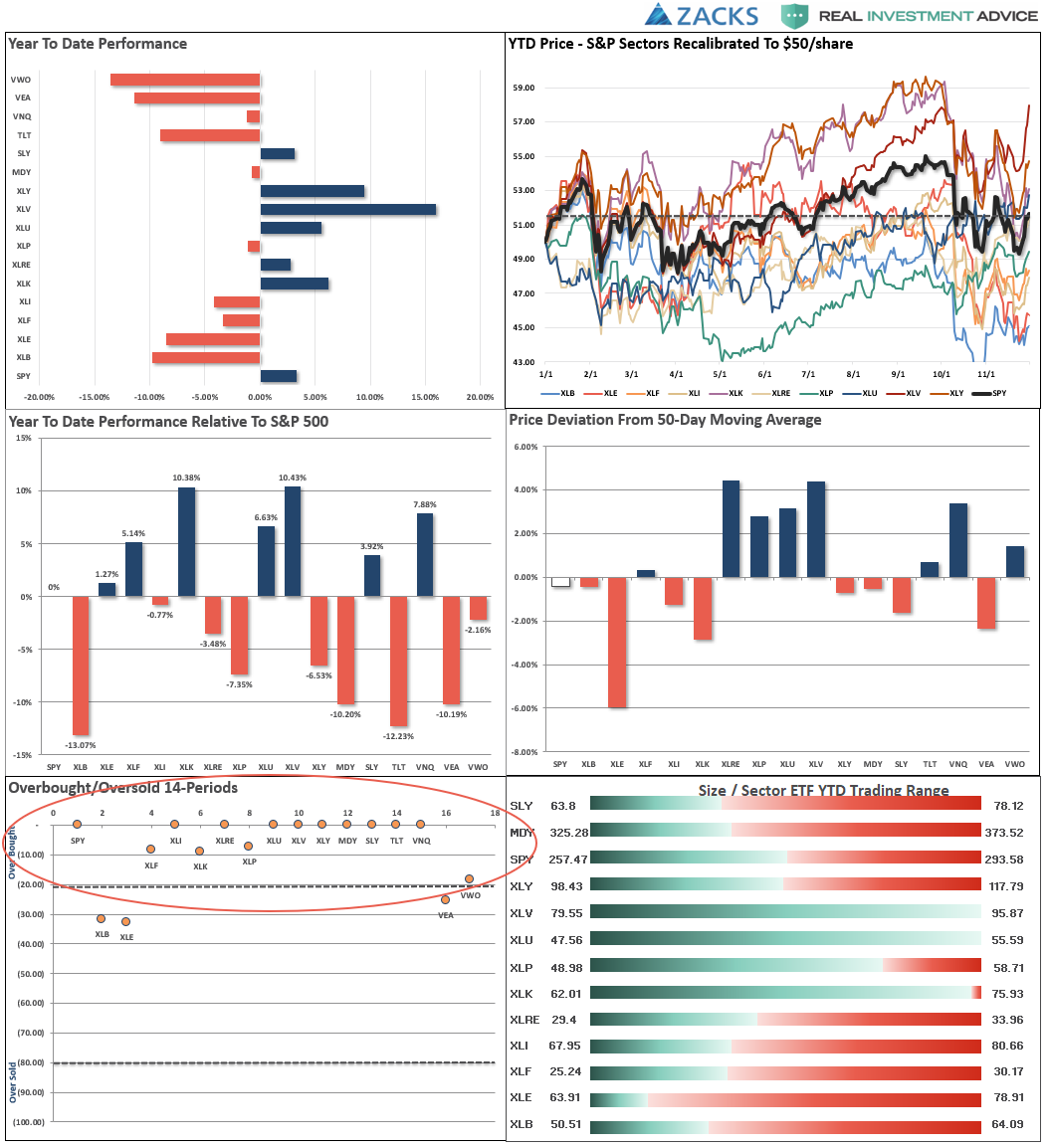

Sector & Market Analysis:

Sector-by-Sector

Discretionary and Technology After having violated the 200-dma, the sectors finally put together a rally last week. Discretionary, like the broader market, is running into resistance at the 200-dma with the 50-dma just above and heading lower. The same goes for Technology, but tech remains a decent distance below the 200-dma with a crossover of the 50-dma approaching rapidly. Given Tech is a huge weighting of the overall market, the bearish backdrop for the sector should not be dismissed.

Industrials, Materials, Energy, Financials, Communications – we are currently out of all of these sectors as the technical backdrop is much more bearish. With all of these sectors wrestling with the 50-dma which is running below the 200-dma the downside pressure remains on for these sectors as a whole. If you choose to be long these sectors it is advisable to remain underweight for now. Industrials, Materials, and Energy are representative of the broader economic activity in the U.S. and currently suggests we are seeing weakness on the horizon.

Real Estate, Staples, Healthcare, and Utilities continue to be bright spots. We continue to remain long staples and healthcare specifically. Despite a seemingly more bullish backdrop for the markets over the last few days, money is still primarily gravitating to traditionally more defensive sectors of the market.

Small-Cap and Mid Cap – both of these markets are currently on macro-sell signals and the recent rally in both markets failed to get above technical resistance. More importantly, the previous oversold condition is now gone and suggests lower prices are coming. Like Industrials and Materials above, Small and Mid-cap stocks are very economically sensitive and suggests a much weaker backdrop going into 2019. We remain out of these sectors for now.

Emerging and International Markets – Emerging markets broke above its downward trending 50-dma last week and showed some signs of life. We have seen this before which ultimately led to lower lows. However, a recent series of higher bottoms suggests a bottom might be forming. We will look for a tradeable opportunity but need some more confirmation first. International markets still look terrible and no improvement is being made there just yet. With major sell signals in place currently, there is still no compelling reason to add these markets to portfolios at this time.

Dividends, Market, and Equal Weight – Not surprisingly, given the rotation to “defensive” positioning in the market, dividend based S&P Index is leading the charge and is approaching all-time highs. Given the drag from Technology and Finance as of late S&P equal weight index is the lagging the S&P market-cap weighted index by a small amount. The overall market dynamic remains negative for now.

Gold – Gold remains in a downtrend, but the good news is the price continues to hug along the 50-dma which has turned up. We are still looking for a “sign” there is a committed trade to the metal before getting back in after having been out of the trade since 2013. Move stops up to $114 if you are still long the metal.

Bonds – continued to perform better last week and after a successful retest of the 50-dma have turned higher. Currently, bonds are very overbought which likely suggests a pullback is coming which would coincide with a further rally in the stock market through the end of year. However, such a pullback will likely provide a good buying opportunity as evidence of broader economic weakness continues to mount. We remain long our core bond holdings for capital preservation purposes but all trading positions are currently closed.

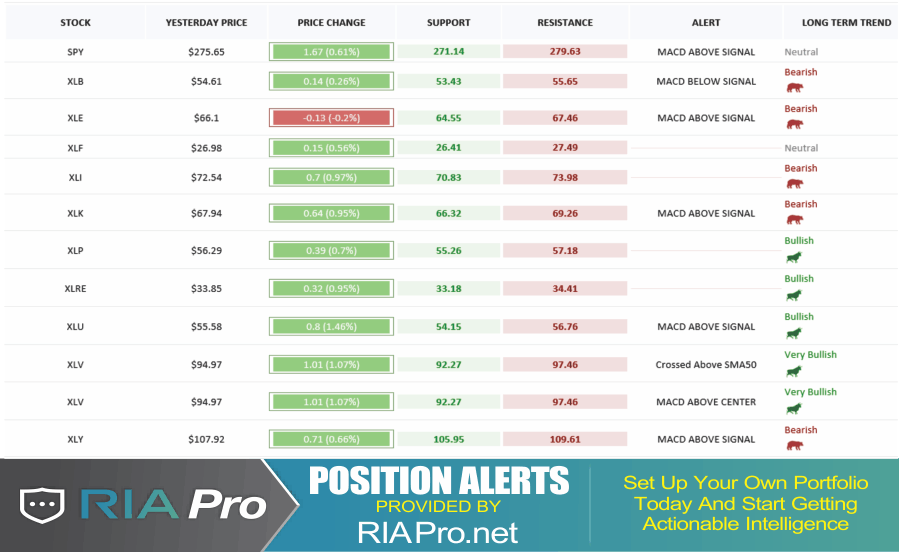

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

As noted last week, the market action remains troubling, to say the least. The bullish trend longer-term remains intact but more bearish dynamics are rising. However, after having got stopped out of many of our positions over the last several weeks were are currently more underweight equity than we should be.

We are looking to add some selective exposure over the next week particularly if progress is made on the “trade” front between the U.S. and China.

- New clients: We will continue to hold existing positions and add new positions selectively.

- Equity Model: On Friday, we added 1/2 weights to AEP, AXP, CMCSA, MDLZ, MDT, MMM, CHCT, & CDW. We will look to bring existing 1/2 weight positions to full model weights. Stops have been dramatically tightened up.

- Equity/ETF blended – Same as with the equity model.

- ETF Model: We will look to add further exposure this coming week if a positive outcome from the G-20 presents itself.

Again, we are moving cautiously. There is mounting evidence of short to intermediate-term risk of which we are very aware. However, with the market moving into the seasonally strong period of the year, we realize that short-term performance is just as important as the long-term. It is always a challenge to marry both.

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these actions either by reducing, selling, or hedging, if the market environment changes for the worse.

.