Money Morning Article of the Week

by Keith Fitz-Gerald, Money Morning

Wal-Mart Stores Inc. (NYSE: WMT) had its market value wiped out by $18 billion a week ago Wednesday after senior management revealed the company may suffer a 6% to 12% earnings drop in 2017.

The actual story here, however, has nothing to do with the company itself.

Conventional wisdom would have you believe that Wal-Mart is a unique situation and the lowered expectations are about everything from compressed margins to the fact that Amazon.com Inc. (Nasdaq: AMZN) is eating Wal-Mart’s lunch.

All of those things are true.

Analysts like Morningstar’s Ken Perkins noted that the sell-off is an “overreaction and a buying opportunity.”

That may also be true, but again, the story isn’t about Wal-Mart.

Instead, it’s about a change in market tenor – both for Wal-Mart and for the stock market.

You see, this has everything to do with a fundamental shift in market conditions that’s going to catch millions of investors by surprise this earnings season.

My job is to make sure you and your money come out on the right side of the equation – so let’s get cracking! Here’s what you need to know about today’s markets…

Wal-Mart’s Double-Digit Dive Reflects a New Era in Markets

There’s been a meme since the financial crisis began: what’s bad is good and what’s good is bad.

The basic drift is that any bit of bad news is actually good because it implies further Fed involvement in the markets and lower interest rates. That’s why the markets have moved higher since 2009 on bad jobs data, terrible consumer confidence, and falling economic numbers. That’s also why the markets have tanked on even the smallest bits of good news – a signal that traders believed would hasten the Fed’s exit.

But now that the Fed has taken a “damn the torpedoes” approach to raising rates, the markets have begun to recognize that bad news is actually bad news – not the good news it was a few months ago.

And that, in turn, brings the focus squarely back to earnings, or in this case, earnings potential at a time when earnings are being revised lower faster than Tom Brady (allegedly) deflated his footballs.

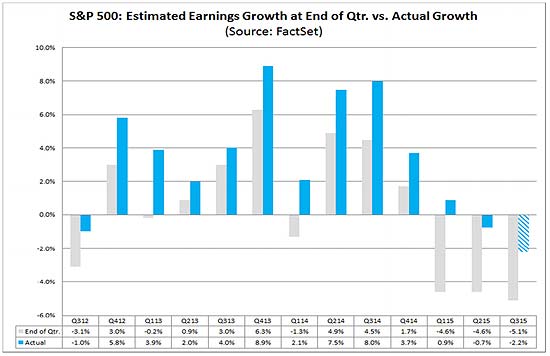

This season, for example, the S&P 500 is expected to report an average year-over-year earnings decline of 5.5% for Q3, according to FactSet.

That’s what makes this so dangerous.

When S&P 500 companies report earnings that are above earnings estimate, the overall growth rate goes up because actual earnings numbers replaced lower estimated numbers. But the converse is true, too. Reported declines negatively impact actual growth rates which, as you can see below, are already decelerating sharply.

I honestly don’t know why this is such a surprise to most investors.

Earnings – above all else – are the single strongest predictor of stock prices over time. If there’s a decline in the works as I think there is, it will be the first back-to-back series of earnings declines since 2009.

The fact that Wal-Mart is talking about 2017 implies another four to six quarters of negative growth. Only two quarters are required for a recession.

And that is really what unhinged traders.