by Pebblewriter, Pebblewriter.com

Ever wonder why the S&P 500 keeps rising, even though there’s so much crummy stuff going on in the US economy and the world in general? Ever wonder how the market can shrug off crappy retail sales, lousy earnings, or a plunging NASDAQ? It’s as though those things don’t even matter, right? The truth is, they don’t. I’ll explain.

Leading up to and since USDJPY topped out on Jan 2, I’ve written extensively about the impact the reversal should have on stocks. In short, every time the pair has backed off of the trend line that connects latest top to the 1998, 2002 and 2007 ones, stocks have dropped anywhere from 22 – 57%.

Click to enlarge

This time, it hasn’t — at least not yet. The moving averages are bearish. The channels are mostly bearish. The harmonics are bearish. But, the yen is still being aggressively trashed by the Bank of Japan in an effort to increase Japanese exports (a cheaper yen makes Accords more affordable in the US.)

Without devolving into a lengthy discussion of whether or not Abenomics will ultimately work (it won’t), suffice it to say that it’s doing a great job of maintaining the bull market for US equities. Meet the yen carry trade.

In the good old days, a carry trade involved borrowing at a low interest rate and re-investing at a higher rate. It could be done in different currencies, as long as the currency in which one borrows depreciates or at least doesn’t appreciate relative to the one in which one invests.

So, one could borrow in yen at 0% and reinvest in US dollar denominated paper at 0.25% (or Brazil, Iceland, etc. at much higher rates) and have no risk as long as the yen doesn’t appreciate against the dollar. Done in enough volume, this is essentially a risk-free way to print a lot of money. And, thanks to the BOJ trashing the value of the yen, there was no risk for a long time.

But, why reinvest the proceeds in overnight paper at .25% when stocks are gaining over 50% per annum as did the Nikkei? Money flowed into the Japanese stock market — as well as those in Singapore, Hong Kong, Philippine, Indonesia, Korea, etc. The BOJ even buys ETF’s of Japanese stocks directly, just in case the market isn’t stimulated enough by $80 billion per month of quantitative easing.

Click to enlarge

Only problem… it stopped working. The Nikkei stalled out when the USDJPY did and fell by over 15% — hardly a risk-free proposition. If only there were a stock market whose prices were guaranteed by a central bank to never decline…. oh, wait! How about these guys!?

“I pledge to never allow the market to decline!”

It’s a marriage made in heaven. Between the BOJ and the Fed, there’s plenty of 0% money for the asking — especially if you’re a TBTF bank with Janet Yellen on speed dial.

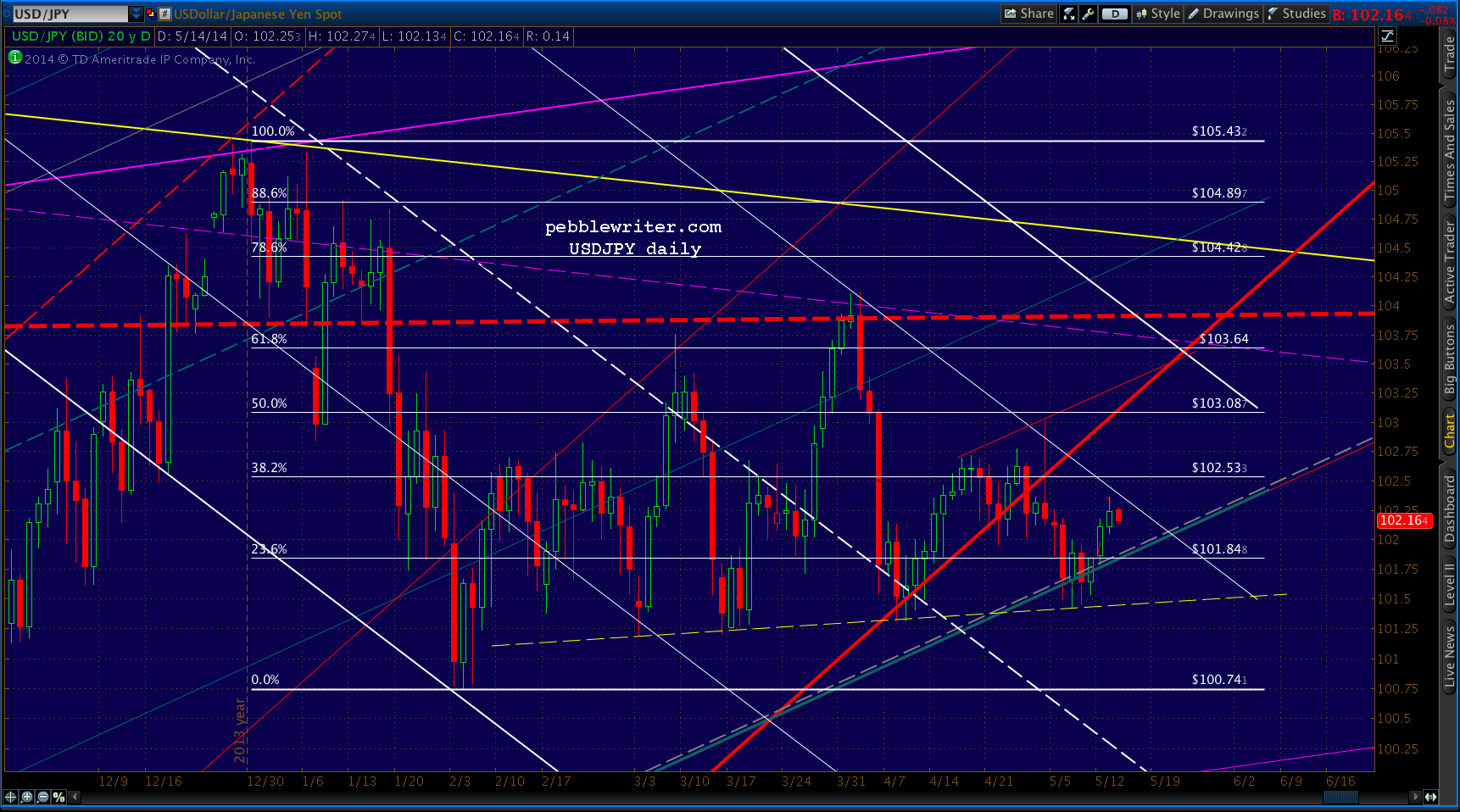

The process is pretty simple. When the yen declines (meaning the USDJPY rises), it’s stock-buying time. In other words, a rising USDJPY means a rising ES/SPX. Of course, USDJPY can’t go up all the time. In fact, it fell from 105.43 to 100.74 between Jan 2 and Feb 3. It bounced there, and has since chewed up a lot of real estate, see-sawing back and forth for 3 1/2 months just like NKD (same neckline and unfulfilled H&S Patterns.)

Click to enlarge

Remember, they’re both being propped up by the BOJ — and, not that namby pamby wink-and-a-nod propping up like the Fed. We’re talking outright manipulation whenever and wherever they feel like it. Gazing at that dashed yellow neckline (just like NKD’s), it’s pretty easy to tell when they felt like it. And, if they’re ever asleep on the job, the bankers benefiting from the trade are only too happy to jump in and “stabilize” things.

I know what you’re thinking… if USDJPY see-saws back and forth, why doesn’t it unwind all the benefits of its rallies every time it declines? I’m glad you asked.

The trick is to allow the USDJPY to reset at a time when stocks aren’t affected, i.e. the after-hours market. After a full day of follow the leader where stocks chase USDJPY higher, the cash markets close. SPX, having pocketed its 10-15 points, can sleep peacefully even while USDJPY and the Nikkei drop like a bad transmission. Why?

At night, the volume in the futures is so low that the same guys playing this game during the day can easily prop up them up. We’re talking $50mm or less most nights. All they have to do is put in a big bid at a critical support level; 500-1,000 contracts on the e-minis usually does the trick (I know, I’ve pulled all-nighters trying to get the 3-4 points a pattern promised.)

Anyone trying to short ES had better have deep pockets, because that bid won’t budge until the big banks feel like it — usually in the dead of night when US investors are sound asleep. Then, after USDJPY (and, often NKD) have been brought back into alignment with whatever patterns they’re completing, TPTB are free to start pumping ES. Generally speaking, it’ll be in the early morning — an hour or so before the cash market opens.

If timed properly, investors will wake up and see the futures up 5-10 points, and race to the office conditioned to Buy-Buy-Buy! It happens over and over again, resulting in new highs even when there’s little to justify them. I’ll finish with a few charts for illustration purposes. These are from the past few days — nothing special about them. I could just as easily have picked a few days from last week or last month — same results.

This is the e-minis since yesterday morning. Note the huge plunge in USDJPY that was arrested right before the market opened. Two higher lows in a row established enough of a trend that ES rallied strongly on the opening, even after the crappy retail sales figures. USDJPY kept climbing, so ES did as well — at least until SPX bagged 1900 (the objective.)

The lighter shaded area represents the overnight session.

Click to enlarge

After that, USDJPY’s job was to keep ES’s decline manageable until the close. And, it worked like a charm. Despite two lower lows, there was no follow-through. After the close, USDJPY plunged while ES barely budged. As I write this, ES has actually risen — and, much more than USDJPY has.

Here’s another chart going back to last week that shows more of the same.

Click to enlarge

And, another from the perspective of USDJPY (ES in purple):

Click to enlarge

And, last, here’s one showing NKD over the same time period:

Click to enlarge

It’s hard to say how long this can go on. The target is clearly the S&P 500, as COMP, RUT and NDX can attest. There are probably trillions of dollars at play, though I’ve been unable to find any statistics. The BIS might touch on it in their June report, but who knows?

A significant enough event will probably bring it all crashing down one of these days. It will require a big drop in stock prices and/or sustained strength in the yen (the object of a flight to safety for Asian investors). A fighting war in Ukraine directly involving the US and Russia would do it. An announcement from the BOJ that they were going to stop manipulating the yen would work. And, the termination of the Fed’s QE will no doubt help.

And, here’s a wild card for you: the de-dollarization of global finance. Zerohedge just posted a thought-provoking article about meetings going on between China, Russia, et al designed to unseat the dollar as the medium for global trade (including the petrodollar). It needn’t be a clean sweep in order for the dollar to weaken relative to the yen (USDJPY falls).

Bottom line, it’ll keep on working until it doesn’t. Chart patterns, harmonics, technical analysis, support and resistance — all this stuff is pretty meaningless as long as the yen carry trade game goes on. It’s a very frustrating situation for those of us who rely on these normally reliable tools to anticipate market moves.

But, there will come a day. And, the force of all that leverage unwinding and bubbles popping will probably make 2007-2009 seem mild by comparison. Remember the $1.5 quadrillion in derivatives that are still out there — carried at book value (under the illusion that they will all somehow net out) at over twenty times the Gross World Product and hundreds of times the Tier 1 capital of the banks that gave them birth.

Those who are now mindlessly buying all the dips will experience some long, dark days during which they can reminisce about the good times — when central bankers ruled the world and nothing bad ever, ever happened.

Epilogue:

After yesterday’s lackluster performance, ES needed to tag downside support in order to get a boost for higher prices. The best candidate (meaningful, and not too far down) is the neckline of the recently completed IH&S pattern. Only problem, ES was in a decent uptrend most of the night. The neckline was getting further and further away.

USDJPY to the rescue. The pair took a timely dive starting around 3am EDT and didn’t let up until ES had reached the IH&S neckline. They were careful to leave a higher low in order to establish a rising trend in USDJPY — a cue for investors looking for some direction.

Click to enlarge

If ES can break out of the falling red channel and get a nice bounce off the rising white channel, USDJPY will have done its job. ES will be in a position to take a run at new highs, ideally reaching its IH&S target of 1917ish.

Will it get there? Who knows. If you’re a big bank managing $500 billion and have mutual funds to sell, you need it to. If you’re a market maker, you’d like traders to think it will, betting heavily before you pull the rug out from under them — preferably on a weekend or overnight.

USDJPY needs to get back above the key support represented by the grey channel bottom. But, if that’s the plan, you can bet that USDJPY will lead the way.

Click to enlarge

One obstacle, this morning’s PPI figures did a number on the 10-year. A reversal off the .886 down at 25.35 (125’225ish) would be helpful in providing a floor for stocks. Maybe corresponding with a backtest of the former highs for SPX/ES (1891.33/1886.00), 14275 on NKD, and the red .786 or .886 for USDJPY (101.64 or 101.55)?

Click to enlarge