Why Top Tier Data But No Breakouts, What’s Missing?

by Cliff Wachtel, FX Empire

FX Traders’ weekly EURUSD fundamental & technical picture, this week’s market drivers that could change it- the bullish, the bearish and likely EURUSD direction.

The following is a partial summary of the conclusions from the fxempire.com weekly analysts‘ meeting in which we cover outlooks for the major pairs for the coming week and beyond.

Summary

- Technical Picture For This Week: Neutral-Standoff Between Weakening Momentum, Resistance Continues

- Fundamental Outlook: Neutral Near Term, Bearish Longer Term

- Trader Positioning: Shorts Grow As EURUSD Edges Back To Top Of Trading Range

- Conclusions: Why no breakouts despite top tier data, likely trading range this week, what could bring a breakout

TECHNICAL OUTLOOK

First we look at overall risk appetite as portrayed by our sample of global indexes, because the EURUSD has been tracking these fairly well recently.

Overall Risk Appetite Per Weekly Charts Of Leading Global Stock Indexes

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA [DATES] In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

Sample Global Index Weekly Charts’ Key Take-Aways: Continued Risk Appetite Is EURUSD Bullish

Overall risk appetite per US and European sample indexes show a 3 week uptrend, a 12 week flat trading range, and long term uptrend since at least mid-2012. In other words, short term and long term trends favor more EURUSD upside.

This bullishness is confirmed by the S&P 500 and DJ EUR50 weekly charts both closing within their double Bollinger® band buy zones. That suggests that their medium-long term momentum is strong enough for the odds to favor more upside.

EURUSD Weekly Technical Outlook

EURUSD Weekly Chart March18 2012 – Present

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

EURUSD Weekly Chart Key Take-Aways: Inconclusive Standoff Between Momentum, Resistance.

We’ve a continued standoff between upward momentum and resistance.

Once again the pair tracks the S&P 500 well, also closing higher on the week but remaining within its 12 week trading range.

Medium-Long Term Upward Momentum Continues:

-For the first time in 4 weeks the pair closes firmly within its double Bollinger ®Band buy zone

-All weekly EMAs continue to move higher

However resistance around 1.39 has not yet broken.

In sum, the weekly charts’ picture of medium and long term price action both upward momentum and resistance holding, YET both showing signs of weakening.

-Resistance weakening: the pair DID close above both the long term downtrend line (green) from July 2008, and the 61.8% Fibonacci retracement of the downtrend from mid-2011 to mid-2012.

-Momentum weakening: the 12 week trading range is taking its toll on upward momentum as the EMAs’ upward slopes are rising at a slower pace.

EURUSD Daily Technical Outlook: Note The Dojis

EURUSD Daily Chart December 23 2013 -Present

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

Key Take-Aways Daily Chart:

The daily chart shows the short term outlook for the pair is the same as for the weekly chart, a standoff between bullish upward momentum and bearish resistance, with both momentum and resistance showing signs of weakness.

Bullish upward momentum: the pair closed in its double Bollinger ® band buy zone, and the EMAs continue to move higher, but at a slowing pace as they weaken and flatten out.

Bearish Resistance: 1.39-1.40 holds as the pair traded within 1.380-1.387.

Note also that the once again the week ended with two ‘doji’ type daily candles that reflect indecision.

Second Opinion: Daily Charts Per BoFA- Merrill Lynch: Medium/Long Term EURUSD Topping Out

For those seeking second opinion, the bank sees the current 1.39-1.40 as a top for the coming months or longer, with tests of support at 1.31 and eventually 1.28-1.27.

EURUSD Daily Chart Showing Evidence of Topping Out ~1.39-1.40

Source: BofA- Merrill Lynch (via efxnews.com here)

Technical Picture Conclusion For This Week: Neutral-Standoff Between Weakening Momentum, Resistance Continues

We therefore look to fundamentals for guidance.

FUNDAMENTAL OUTLOOK: THE BALANCE OF BULLISH VS. BEARISH

Below we cover bullish and bearish fundamentals that are specific to Europe and the US. Of course the pair is heavily influenced by overall risk appetite, which we cover in depth in out weekly previews here.

As the minimal movement in the above EURUSD weekly chart suggests, despite the abundance of top tier data, the results were so mixed that the aggregate effect was minimal. There’s been no significant change in the relative fundamentals, they remain in equilibrium. In particular, the long expected Fed tightening remains in the distant future, and the expected ECB easing in June is probably mostly priced in already, as Nomura notes here.

Thus it’s no surprise that the EURUSD remains within its 12 week range, awaiting a material change in either risk appetite or a change in relative rate expectations that should eventually favor the USD and send the pair lower. Eventually.

That said, here’s how the bullish and bearish forces align for the pair as we look to the coming week.

BULLISH

US, EU Data Both Mixed

Neither currency saw a material advantage from the past week’s economic reports. Each bullish report seemed to be met with a bearish counterpart. The climactic event of the week, the US monthly jobs reports encapsulated this theme perfectly, as it proved to be a study in conflicting details that had little effect on both stocks and the EURUSD. More on that below.

European Data Not Bad Enough To Undermine EUR Short Term Demand

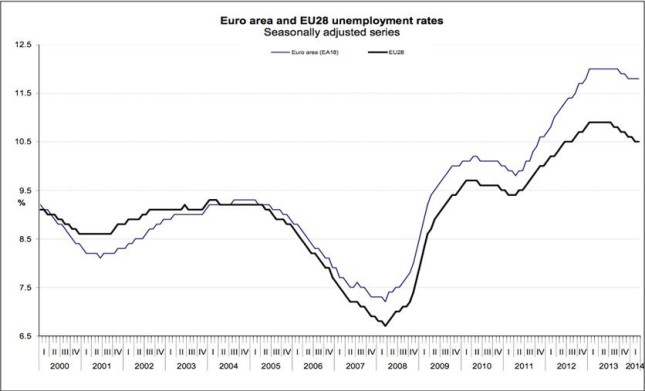

Economic data from Europe this week was good enough to sustain demand for EUR denominated assets, and thus support demand for the Euros needed to buy them.

On Monday German preliminary CPI missed forecasts, coming in lower than expected, but it was still higher than in March. Spanish unemployment was not only weaker, it was also worse than the already disastrous expected 25.6%. Yet, on Friday yields on Spanish notes fell below 3% for the first time since 2005. That poor Spain jobs data was a harbinger of the EZ unemployment data that came out Friday. It was a relatively less dismal 11.8%, which was actually a bit better than the expected 11.9%.

Via Eurostat

The good news is that it is starting to trend lower. The bad news is that that this month’s “improvement” is still near all-time highs, and thus virtually assuring continued weakness in spending, growth and deflation data, and rising pressure on the ECB and EU to attempt to a variety of possible remedies, all of which are bearish for the EUR. These include a variety of easing measures like lowering rates or some QE variant, increase spending, etc.

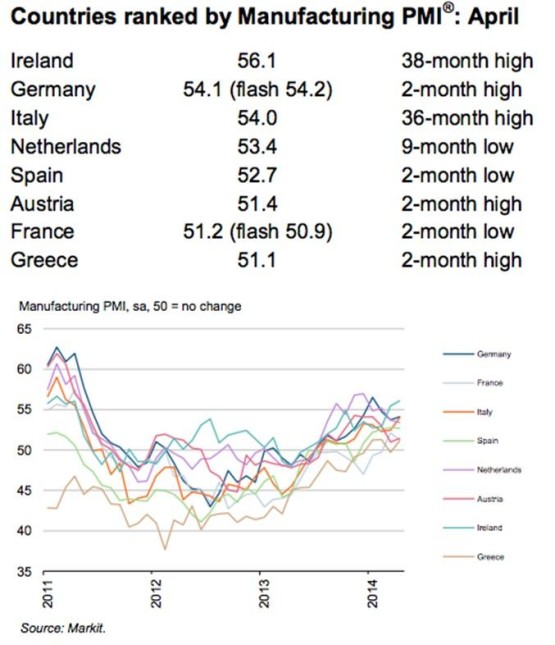

Similarly, EZ manufacturing PMIs from Friday were also a mixed bag.

Markit (Via Business Insider )

The good news is that all were over 50, indicating varying degrees of optimism. Overall, they continue with the theme of slow recovery.

The bad news is that they also suggest a recovery that is too slow to bring a enough improvement in the area’s economy to prevent further EUR dilutive measures in the coming months.

Other data continued along these lines. Spanish flash GDP q/q was in-line at 0.4%, the fastest in four years though weak by normal standards. The key is that didn’t disappoint, remained positive, and so it did not provide a reason for EU optimists to halt the rally in Spanish and GIIPS assets. German retail sales came in a bit below forecasts, German unemployment beat expectations.

Thus as the weekly charts for European indexes show, EU stocks (and bonds) continue to hold steady or rise, supporting EUR demand, at least in the near term.

US Data Also Mixed Also Mixed

US top tier data has also been mixed, but continues to show overall slow improvement.

US preliminary GDP came in way below expectations (-0.1% vs +1.2% forecasted) and the prior quarter was revised lower.

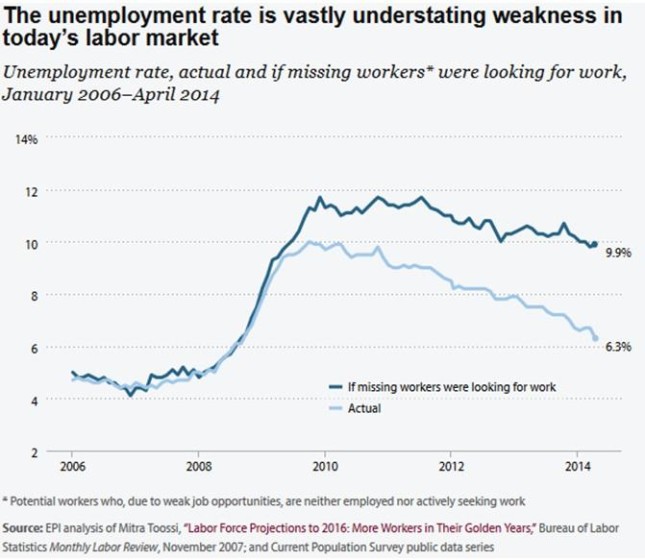

US monthly non-farms payrolls smashed expectations (288k vs. ~218k expected), and the unemployment rate plunged from 6.7% in March to 6.3% in April, seemingly countering the GDP disappointment. Yet even these gaudy figures belie the more ambivalent details.

-The labor participation rate (LFPR) fell to its lowest level since 1978, suggesting that the drop in the unemployment rate was due mostly to longer term unemployed no longer looking and thus no longer counted in the unemployment rate calculation.

–Per Dan Crawford of the Economic Policy Institute , the headline unemployment rate heavily understates true unemployment, saying if the LFPR were more stable, the unemployment rate would be much higher, closer to 9.9%. Still, the U-6 rate (more inclusive of those discouraged dropouts) also fell along with all other alternative measures of labor underutilization.

Source: Dan Crawford (via Business Insider)

-Wages remain stagnant.

Other data on jobs, housing, consumer confidence, etc., was mixed.

Most importantly, the tepid US data prevents any USD supportive speculation about a faster Fed tightening.

US Jobs Report’s Conflicting Data Points Neutralize Each Other

Despite the glowing headline figures, the jobs had little influence on the pair Friday, as the above daily chart shows. Here’s why.

- Labor Force Participation Lower, Wage Growth Stagnant: Despite the great headline figures that smashed expectations for both NFP growth and the unemployment rate, the employment picture still equivocal. In particular, Labor Force Participation Rate Fell to 62.8% from 63.2%. Thus the employment rate improvement was attributed to the loss of ~800k active full time job seekers. This is the key undermining factor that kept the report from being clearly positive and very USD supportive, as tightening expectations could have been revised forward significantly.

- USD Not Getting Any Rate Advantage Needed For Sustained Rally, Yield Curve Flattens After Jobs Reports

- Rate Hike Expectations Essentially Unchanged, From July to June of 2015

The conflicting data in the US jobs reports means Yellin’s speech next week now takes on added importance as markets will be looking clues on any possible changes in Fed policy. See our below conclusions for more on that, and stay tuned for our coming post on the lessons for the coming week too.

European Stocks Attract Buyers Despite Continued Weak Earnings, Downward Revisions

Despite the mixed data out of the EU, European stocks continue to attract buyers, despite continued weak earnings performance and Europe’s weak growth outlook. The demand drivers include M&A activity, continued weak USD interest rates, as well as optimism about the EU’s recovery, fed by what we believe is excessive complacency about risks due to:

- Potential for further damage from the Ukraine crisis, given Europe’s vulnerability to higher energy costs, and European business and banking exposure to Russian default and currency risks.

- The failed banking union deal leaves EU banking inadequately protected.

- European shares suffer from continued weak earnings performance and Europe’s weak growth outlook doesn’t help their longer term prospects.

See our weekly preview for details.

BEARISH

France To Push For Lower EUR

French PM Manuel Valls, declared on Tuesday that France will pressure the EU to lower the value of the euro after European parliamentary elections next month. As part of his effort to gather French parliamentary support for his commitment to meet EU-designated fiscal targets, Mr. Valls said European growth initiatives must be matched by a more dovish monetary policy “because the level of the euro is too high”. Germany remains opposed such moves.

EU Flash CPI Below Forecasts, Keeps Deflation Threat Pressure On ECB Over Longer term

Although the CPI results printed a bit lower than forecast, they were still higher than the previous month’s figures so that the rate of change in price levels was positive. The higher CPI readings raise the odds that the ECB will wait another month before announcing new dovish policy initiatives.

Many have pointed out that the ECB must choose between the lesser of evils when it comes to further easing actions. Imposing negative rates would likely anger retail savers who would now start seeing a monthly drop in the absolute value of their bank deposits, a penalty for retaining cash. A QE program to purchase asset backed securities would likely be too small to matter given the market’s current size. Yet any attempt to buy more liquid, easily available US Treasury bonds is simply seen as politically untenable given the unpopularity of supporting US debt when so many EU nations’ need demand for their bonds to keep their borrowing costs down. Thus far the ECB has tried to delay these choices for as long as possible, hoping that prices rise on their own as the GIIPS slowly recover.

Fed Continues Taper Despite Mixed Data, Remains Upbeat On US Outlook

Despite the poor GDP showing, FOMC minutes last week confirmed the Fed will continue its taper and remains on course for higher rates sometime in mid-2015.

Key points of the FOMC meeting minutes included:

- Taper Continues by Another $10bln -$5bln MBS, $5bln Treasuries

- Decision was Unanimous – No Dissenters this time

- Fed Optimistic, notes:

- “Economy Picked Up, after having slowed sharply during the winter”

- “Consumer Demand Rising More Quickly”

- “Labor Market Indicators Mixed but on Balance Show Further Improvement”

The overall positive tone of US data, particularly the stellar headline NFP and unemployment rate figures add weight to this outlook.

EU Stress Test Not To Be So Rigorous After All

As we’ve repeatedly noted in past posts on the inadequate banking union deal, the lack of a real EU backstop for failing banks means the ECB must choose between

- Fulfilling its promise to actually run rigorous banks stress tests and risk scaring markets if /when many banks fail, because there is NO safety net in place.

- Lowering the standards of the stress tests, in keeping with traditional ECB standards that saw passing banks need bailouts shortly afterwards.

We are shocked (shocked!) to learn yet again (after already lowering reporting requirements in recent months) that the ECB has chosen once again to keep standards low enough to keep the failure rate and needed emergency bailouts manageable, and to pray for continued calm.

In the short run a high pass rate may actually be bullish for the pair if it maintains the illusion that EU banking has really been reformed. In the longer term it raises the odds of another crisis.

It also vastly lowers the odds that the EU will back meaningful sanctions against Russia and risk defaults on EU bank loans to Russia and EU businesses dependent on Russian cash. Stay tuned for our coming special report (Fools Russian Part 2) for details here.

Top EURUSD Calendar Events

Here are the events most likely to move the EURUSD.

Monday

China: HSBC final mfg PMI – could be relevant as top tier China data can move overall risk appetite.

US ISM non-manufacturing PMI: Consensus is 54.3 versus March’s 53.1 read, but 4 out the past 5 readings have come in below forecasts.

Tuesday

EU: Spain employment change, services PMI, Italian services PMI, EU retail sales. None are top tier by themselves, but collectively these could be market moving if they all surprise in the same direction.

US: trade balance

Wednesday: Has Potential To Be Big, Probably Won’t

US: Fed Chain Yellin testifies before the Joint Economic Committee of Congress. As noted above, we don’t expect her to say anything that changes market perceptions of Fed policy, given that recent data has not provided a reason to do so, as noted above.

Thursday

China: trade balance

EU: ECB meeting and press conference – more likely than Yellin’s testimony to produce market moving comments, but still expected to be a non-event without surprises. Draghi whining about how the EUR is too high is not news, so we’d be surprised if markets move on his warnings about weakening the EUR unless he actually announces significant new policy moves to do that NOW. Markets don’t expect these until the June statement at earliest.

Friday

China: CPI, PPI (both y/y) – Consensus is for a drop to 2.1% from 2.4% in March. A lower reading would be bearish, suggesting more slowdown than expected.

US: JOLTS jobs openings – has assumed new importance because Yellin believes it’s a key US jobs metric, and after Friday’s confusing report the Fed will be seeking added clarity on US employment and thus whether any policy changes are warranted.

Sample Retail Traders Positioning

Source: Forexfactory.com

As the pair edges closer to a test of the resistance around 1.39, our sample has shifted a bit further to the short side.

CONCLUSIONS

The technical picture is neutral for the coming week.

Fundamentals remain in equilibrium.

-Both Europe and US data is mixed

-The EURUSD remains stuck as continued low US benchmark rates and threatened new ECB easing don’t give either pair a perceived rate advantage. Meanwhile demand for GIIPS stocks and bonds continues to support EUR demand despite the EU’s less appealing economic outlook versus that of the US.

-The conflicting data in the US jobs reports means Fed Chair Janet Yellin’s speech next week takes on added importance as markets will be looking clues on any possible changes in Fed policy. We doubt it. The overall results are positive, however the Fed’s primary “spin control” concern will be to prevent speculators from driving up US benchmark bond rates. Therefore if any FOMC members have thoughts of advancing the pace or timing of tightening, they will likely keep these private lest rising rates dampen the recovery. Thus this top tier event is most likely to leave markets unmoved.

Both the technical and fundamental picture remains inconclusive for the coming week, suggesting more range bound trade within the bounds of the past 12 weeks. That means the pair likely stays within the 1.3934 – 1.376 area.

What could bring a breakout? A surprise from either Yellin’s testimony or the ECB rate statement that shifts market expectations on their comparative policies and rates.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts. For information on a free intro to currencies video course based on my award winning book, see here.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.