EURUSD Weekly Outlook 07 April 2014

by Cliff Wachtel, FX Empire

FX Traders’ weekly EURUSD fundamental & technical picture, this week’s market drivers that could change it- the bullish, the bearish and likely EURUSD direction short, medium, long term

The following is a partial summary of the conclusions from the fxempire.com weekly analysts‘ meeting in which we cover outlooks for the major pairs for the coming week and beyond.

Summary

- Technical Outlook: Weekly Neutral, Daily Bearish, At Clear Technical Crossroads

- Fundamental Outlook: Short Term Neutral, Longer Term Bearish

- Trader Positioning: Our real time sample shows growing long positions as EURUSD falls-bearish on a weekly basis

- Conclusions: Currently at crossroads as strong support of the 1.37 level has held. If it breaks a test of the 1.36 level is likely. If support holds, upside for the coming week limited to around 1.3750 – 80.

- Monthly Chart Shows EURUSD at long term crossroads, though likely longer term USD rate advantage suggests the long term downtrend ultimately prevails

TECHNICAL OUTLOOK

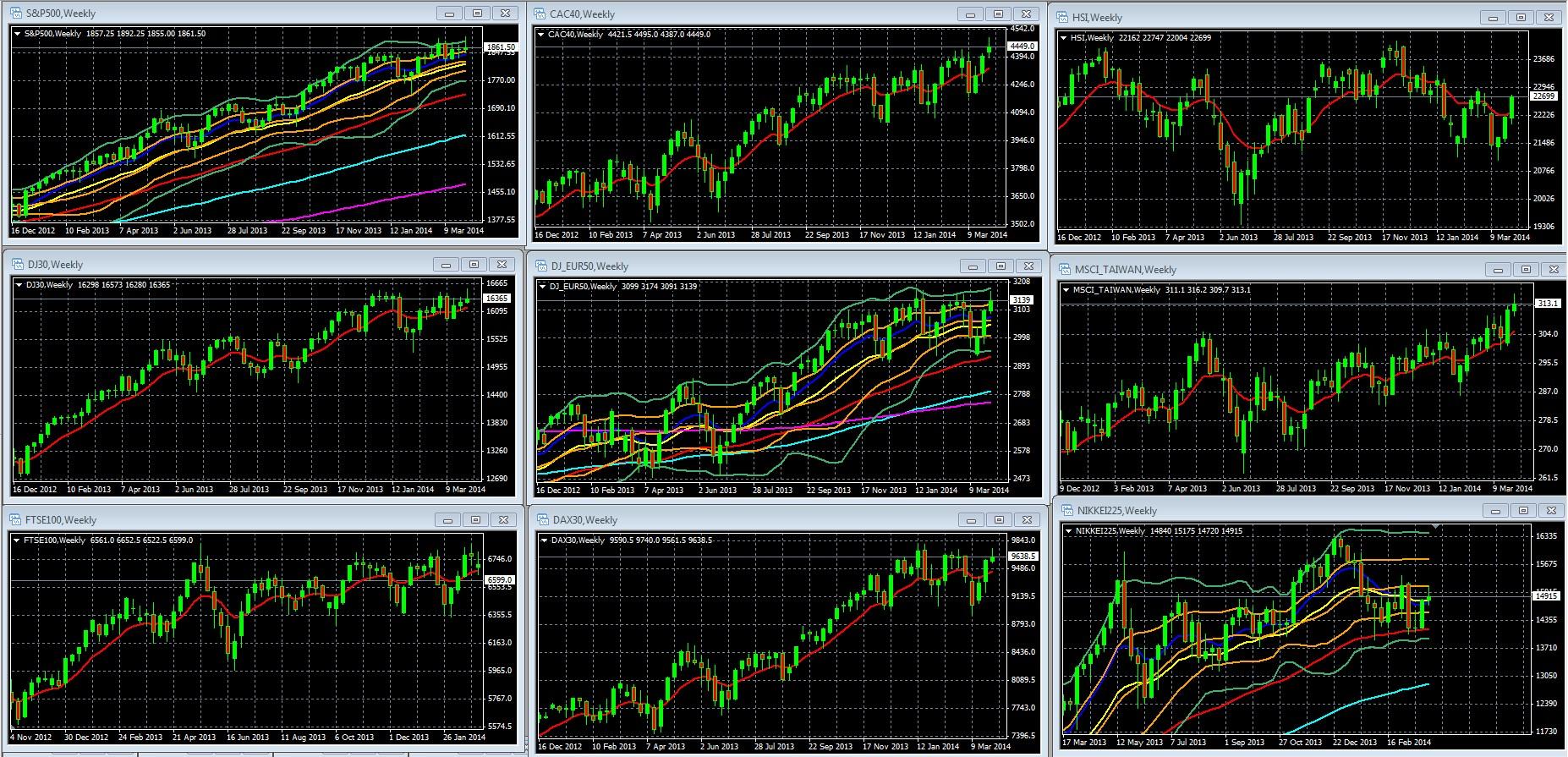

First we look at overall risk appetite as portrayed by our sample of global indexes, because the EURUSD has been tracking these fairly well recently.

Overall Risk Appetite Per Leading Global Stock Indexes Weekly Charts: Bullish

Our sample of weekly charts for leading global stock indexes suggests continued steady-higher indexes, risk appetite.

Weekly Charts Of Large Cap Global Indexes With 10 Week/200 Day EMA [DATES] In Red: LEFT COLUMN TOP TO BOTTOM: S&P 500, DJ 30, FTSE 100, MIDDLE: CAC 40, DJ EUR 50, DAX 30, RIGHT: HANG SENG, MSCI TAIWAN, NIKKEI 225

Key For S&P 500, DJ EUR 50, Nikkei 225 Weekly Chart: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER® BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange.

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

Key Take-Aways Weekly Chart: Bullish

US and European indexes were not only up last week, but also the European indexes overall moved back into (or at least closer to) the double Bollinger band buy zones, so long term risk appetite momentum is strong enough for the odds to favor further gains. Barring any potent EUR or USD news, the EURUSD tends to track overall risk appetite, particularly the S&P 500.

EURUSD Weekly & Daily Technical Outlook: Weekly Neutral, Daily Bearish, At Clear Technical Crossroads

Summary: Neutral longer term (weekly chart), bearish near term (daily chart). Currently at crossroads as strong support of the 1.37 level has held. If it breaks this week, a test of the 1.36 level is likely. If support holds, upside for the coming week per technical data is likely limited to around 1.3750 – 80, the upper end of the new descending channel formed by the past 3 weekly candles.

EURUSD Weekly Chart March 31- April 4 2014 Highlighted With Red Arrow

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

Key Take-Aways Weekly Chart: Neutral But At Major Technical Crossroads

- The pair suffered its third straight down week, creating a steep downtrend

- It remains within the double Bollinger band neutral zone, so momentum is neutral, so we don’t have a reliable trend on the weekly charts.

However strong support of the 1.3700 level held. Note that this level has multiple levels of support, including:

- The 1.3700 price level itself, which has served as significant support or resistance since December 2013.

- The 61.8% Fibonacci retracement of the prior downtrend of the first 5 weeks of 2014.

- The 20 week EMA

Longer Term Conclusions For Weekly Charts: Neutral But At Major Crossroad Of The 1.37 Zone

- Weekly momentum is neutral – no strong weekly trend yet

- Note how a break above or below this 1.3700 level has been a reliable signal of further moves in the same direction. Therefore a confirmed break below this level suggests more downside ahead. If this support holds again, it’s a bullish sign, especially in the context of continued bullishness in US and European risk assets as noted above.

- Note also that the uptrend that began in June 2013 (green up trend line) remains very much intact with its continued series of higher highs and higher lows. Therefore the weekly EURUSD uptrend is firmly intact, even if the 1.3700 support level is broken briefly. This uptrend would be broken by a move below the 1.36 area, where we’ve layered support of:

- The 2 most recent uptrend lines

- The 38.2% Fibonacci retracement level

- The next support after the 1.3600 area is around 1.3485

EURUSD Daily Technical Outlook: Bearish

EURUSD Daily Chart March 31- April 4 2014 Highlighted Area

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER® BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

Key Take-Aways Daily Chart: Near Term Bearish Trend, Momentum, But Major Support Zone Has Held

- Clear Downward Momentum: The pair closed firmly in the double Bollinger band sell zone, so we’ve strong downward momentum that suggests at test of the next big support at least.

- Clear Downtrend

- The pair closed around 1.37, a major support area on the daily as well as weekly chart. In addition to the price level itself, the zone has support from the 100 day EMA and the 61.8% Fibonacci retracement level.

- If support around 1.37 breaks, that opens the way for a test of the 1.36 area, comprised of not only the price level itself, but also both of the most recent weekly uptrend lines and the 38.2% Fibonacci retracement level of the prior downtrend from January 2014

EURUSD Monthly Technical Outlook: Still Bearish But Also At Crossroads

This is a weekly outlook, so we tend to ignore the very long term picture of the monthly EURUSD chart.

Occasionally, when we appear to be at a very long term crossroad, it’s worth presenting the monthly EURUSD chart.

EURUSD Monthly Chart February 2007 – Present, Highlighted Area March 31- April 4 2014

KEY: 10 Week EMA Dark Blue, 20 WEEK EMA Yellow, 50 WEEK EMA Red, 100 WEEK EMA Light Blue, 200 WEEK EMA Violet, DOUBLE BOLLINGER® BANDS: Normal 2 Standard Deviations Green, 1 Standard Deviation Orange

Source: MetaQuotes Software Corp, www.fxempire.com, www.thesensibleguidetoforex.com

Key Points

The monthly downtrend line dating back to February 2007 remains intact

The uptrend since June 2012 (Draghi’s untested OMT program calms markets about Spanish banks) is converging with the longer term downtrend

See our conclusions in the fundamentals section for how we see this being resolved.

FUNDAMENTAL OUTLOOK: Short Term Neutral, Longer Term Bearish

Bullish: Fed, ECB Comments Suggest Neither Central Bank Ready For Policy Shift

That means yield differences between the two currencies aren’t likely to change much, so the pair is likely to move with overall risk appetite. Our sample of global stock index weekly charts suggests risk appetite continues steady to higher. The EURUSD tends to track the indexes, so we must regard the current 3 week pullback as just a normal short term retracement within a (weakening) longer term uptrend.

ECB appears to accept EUR strength while the EURUSD remains under 1.4000

Yellin’s recent comments sounding almost as dovish as Draghi’s, despite better US fundamentals and data.

In sum, although it’s clear markets anticipate an eventual return to the EURUSD’s long term downtrend, that’s not likely to happen until higher USD rates appear imminent. Thus as we note above, the EURUSD weekly uptrend isn’t dead yet.

China Stimulus: Last week China announced a mini-stimulus program, confirming that they despite bearish reforms including tightening credit, they want to keep the slowdown gradual.

Bearish: Long Term Fundamentals Continue To Suggest Eventual USD Rate Advantage & Thus EURUSD Downtrend

The combination of dovish ECB comments and improving US data

ECB Talking Down EUR, Edging Towards New EUR Dilutive Easing

After leaving interest rates unchanged Thursday, the ECB continued to talk down the EUR at the press conference that followed, sparking the biggest single day EURUSD selloff of the week.

Mario Draghi spent most of his press conference on the possibility of additional easing and outlining the ways they could increase stimulus. He was unusually clear on how Quantitative Easing, another rate cut, negative deposit rates and a narrower rate corridor were all under consideration.

For the first time this year, Draghi noted his biggest fear is stagnation.

Clearly the ECB is signaling its increasingly dovish bias, however we don’t see any imminent moves, because the ECB did not see an intensification of deflation, indeed it expects some degree of rising prices in April.

Longer term, markets continue to anticipate an eventual widening rate advantage for the USD, although the gradual pullback in the EURUSD suggests that no one thinks that’s coming soon. As noted above, the technical picture thus far suggests only a normal short term pullback within a longer term (albeit weakening) uptrend.

In sum, the long term story of the Fed tightening and ECB easing remains a long term story that is at least 6-12 months away if the current April 2015 first rate hike consensus is true.

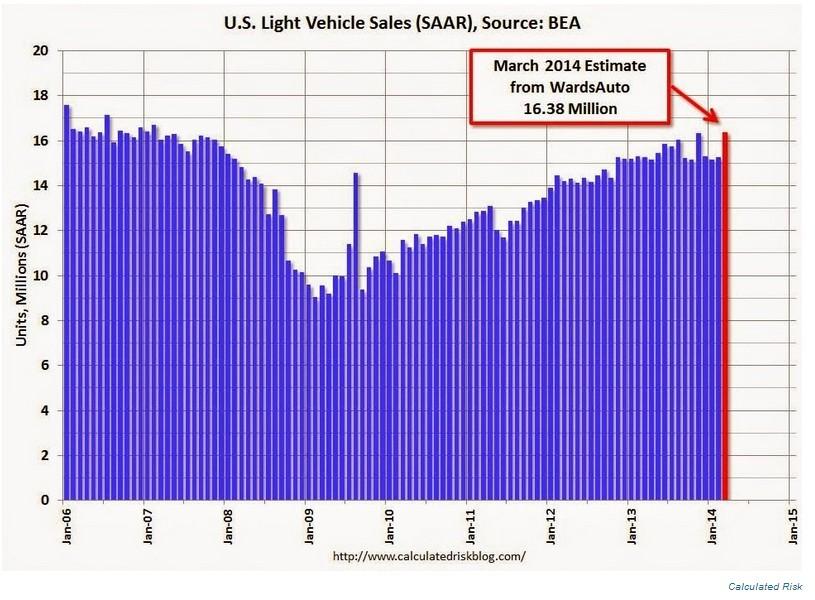

US Car Sales

Hit strongest monthly level since March 2007. Car sales generally correlate well with other economic indicators like jobs and retail sales. If the latest figures are indicative, then the snapback from recent lower winter months suggests recent weakness in US data was indeed heavily influenced by temporary bad weather.

In other words, this suggests the US recovery remains on course, and so does the taper, as well as an eventual USD interest rate advantage from a Fed rate increase in the coming year.

March US Jobs Report & February Revision Higher

This too confirmed the “slow but steady” US recovery theme. Overall, the jobs data was respectable.

Total nonfarm private payrolls rose by 192,000 jobs in March, up from 188,000 in February. The consensus was for about 200,000. However the upward revision of the February NFP from 175k to 197k (+22k) more than compensated for the 8k miss in March. Overall the past 2 months have beaten expectations by that 22k.

The jobs data refuted winter weather excuse for recent US data weakness. Construction employment rose by 19,000 in March, only a minor improvement over the 18,000 added in February. Had winter weather conditions really hit the economy, construction payrolls would have spiked in March just like we saw with car sales above.

The weather did influence the number of hours worked in February. The average workweek fell to 34.3 in February as weather conditions prevented employees from working their normal hours. As temperatures and conditions normalized, the average workweek rose to 34.5 hours in March.

Average hourly earnings were essentially flat in March after increasing 0.4% in February. Thus the increase in hours should help overall earnings going forward due to more hours worked.

The unemployment rate remained at 6.7% in March while the consensus expected the rate to tick down to 6.6%.

Fundamentals Conclusion: Neutral Short Term, Bearish Long Term

Neither the Fed nor ECB is planning any near term policy changes.

In the long term the pair should drop as Fed policy becomes more hawkish and USD supportive relative to that of the ECB.

That leaves the pair to move with overall risk appetite, which, per our sample of global indexes, continues to drift higher. It will take a major risk aversion event to change that trend, or an enduring change in top tier US, European, and global economic growth data (which drives overall risk appetite). There are no such shifts or risk aversion events on the horizon, although there’s no shortage of potential sources, for example:

- Escalation of Russia – West sanctions: Unlikely as Russia sees Ukraine and other weak neighbors as vital strategic assets worth some economic pain, unlike the West. It doesn’t help that Obama may not be capable of even recognizing, never mind confronting, genuinely evil enemies. He looks in the mirror and projects himself onto everyone, assumes they’re all gentleman of good intentions.This explains much of his endless willingness to appease enemies at a cost of forsaking friends. Ok, so would simple “Jimmy Carter caliber” naiveté or inability to confront enemies.

- EU sovereign debt/banking crisis relapse

- China Hard Landing

- China-Japan Escalation on South China Sea Rocks Islands

- Escalation of Russia – West sanctions

- EU sovereign debt/banking crisis relapse

- China Hard Landing

- China-Japan Escalation on South China Sea Rocks Islands

Real Time Sample Retail Traders Positioning

Our real time sample shows retail traders have increased long EURUSD positions over the prior week, as shown in the chart below.

Source: forexfactory.com

On a week-to-week basis they’ve tended to be a good counter indicator.

Per the more reliable sample from the US commitment of traders data, as of the week ending April 1, speculators have cut long positions slightly and increased shorts slightly, the opposite of our sample traders’ behavior.

TOP CALENDAR EVENTS FOR BOTH OVERALL RISK APPETITE AND SPECIFIC TO THE EURUSD

It’s a quiet week per the standard economic calendar events. That gives the big name earnings announcements this week, start of the official q1 2014 earnings season, added market moving potential:

As usual, there are only a few top names in this first of the 3 weeks when earnings season is really influential, but they include leaders in global materials and banking.

- Tuesday: Alcoa (AA) Global materials sector

- Wednesday: Bed, Bath & Beyond BBBY (Retail-consumer discretionary) Ruby Tuesday (RT) (same)

- Friday: JPMorgan Chase & Co. (JPM), Wells Fargo & Co. (WFC)

Tuesday: US JOLTS job openings, 2 Fed governors speak

Wednesday

- China: New loans

- EU: German Trade Balance

- US: FOMC Meeting Minutes

Thursday

- All: G-20 meetings

- US: Weekly new jobless claims

Friday

- China: inflation data – CPI, PPI

- US: Inflation Data – CPI, PPI, preliminary UoM Consumer Confidence.

To be added to Cliff’s email distribution list, just click here, and leave your name, email address, and request to be on the mailing list for alerts of future posts.

DISCLOSURE /DISCLAIMER: THE ABOVE IS FOR INFORMATIONAL PURPOSES ONLY, RESPONSIBILITY FOR ALL TRADING OR INVESTING DECISIONS LIES SOLELY WITH THE READER.