by Poly, Zentrader

Click to enlarge

It just gets worse by the day over in Europe as German PMI manufacturing declined to 48.9 in March, from a 50.3 reading in February. Euro-area services and manufacturing output also fell to 46.5 from 47.9 in February. Europe remains locked in a recessionary spiral that their leaders are dismissing as a normal business Cycle. The estimates out of Europe have been complacent for a few years now as every one of them has the Eurozone quickly recovering and back into growth stages by the middle of this year.

Clearly they have not looked at the Greek example (5 years of recessions) and the impact that an “austerity at all costs” policy has on these structurally weak economies. The problem is that besides Germany (for the most part), the European economies are just not resilient or structurally reformed enough to cushion the drag that deep austerity imposes. They have been so dependent upon government spending for so long that their private sectors are just not capable of quickly filling the large void left by extreme austerity. But at this time the near record high DAX index and the 18 month highs on the French CAC are naively and dangerously pricing in a sharp rebound expected over the coming few quarters.

Click to enlarge

In the U.S, the economy has been much more resilient. But even in the US, we’ve come to accept a new normal where slightly beating expectations or not falling into negative growth is somehow a good thing. We’ve come nowhere near the 4% and 5%+ growth levels associated with a normal recovery and we’re now loudly cheering growth that is in the high 2% range. The same could be said for unemployment, 4 years after the great recession and we’re barely capable of generating 200k jobs, a level that hardly fulfills the demands presented by recent college graduates and new immigrant workers.

To think that all is fine primarily because we’re not dropping into a recession highlights how deep the denial runs. It exposes the fragility of this market as the spread between underlying macro-economic fundamentals and equity valuations are probably at their widest ever. To compound the matter, investors are discounting the artificial support this market is enjoying, instead choosing to view the FED’s involvement in positive light. They are ignorantly viewing the FED’s involvement as accommodating when they fail to realize that the assets they are invested in are on “life support“. The FED has interest rates at zero for 4 straight years and is engaged in buying over $1 trillion of debt each year just to support this economy. Although it’s obviously a massive liquidity boost, how this could be viewed as the foundation of a new bull market is beyond my comprehension.

So the talking heads are feeding us a message that a new secular bull market is underway. But the reality is that the underlying world economy is sick and debt ridden. Secular bull markets are born out of the ruins of deep bear markets, but unfortunately that natural business Cycle has not been allowed to unfold. Instead what we have here is a Ponzi like propping up of asset markets that end up divorcing assets from their true value, and the reality of the world economy. The FED’s stated intention is to raise asset prices through liquidity, and for now this is working. But that objective is to stimulate demand and spending to prematurely induce a self-sustaining growth trajectory. What investors fail to understand is that the market has already priced in both a significant rebound in the world economy and a massive acceleration in earnings. Call me a skeptic, but even the very best case scenario of strong economic growth only serves to satisfy current valuations.

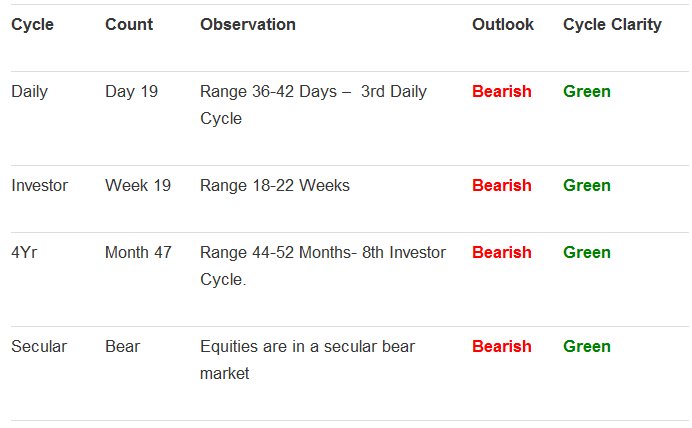

With regards to the currently equity markets, most indices are already at all-time highs or very close to them. 5 weeks ago when the market hit 1,525, there was broad support. We had 92% of stocks trading above their 50dma and 1,000 net new highs. Today, that number is down to 300 net new highs and only 72% of the S&P trading above its 50dma. These are classic diverging warnings that show the market is being supported by fewer stocks. Waning breadth bolsters the case for a coming Investor Cycle Top.

This as is an excerpt from Weekend’s premium update published on Wednesday (3.23) focusing on the Europe’s Equities from the The Financial Tap, which is dedicated to helping people learn to grow into successful investors by providing cycle research on multiple markets delivered twice weekly, as well as real time trade alerts to profit from market inefficiencies.

They offer a FREE 15-day trial where you’ll receive complete access to the entire site. Coupon code (ZEN) saves you 15%.