The Coming Week: Setting The Tone For The Rest Of 2012

by Cliff Wachtel, Global Markets and The Sensible Guide to Forex

Arguably it’s the busiest event risk calendar for the rest of the year, and the one most likely to influence markets for months to come. Here are the top market drivers, both fundamental and technical, that you need to watch for the coming week.

US

The most market moving events are likely to come from the US.

ELECTIONS: All About The Economy, Particularly The Fiscal Cliff

The presidential election is the big event for the week. Tons have been written on this, so let’s just cut to the key points that actually matter.

Market response will likely be based on whether investors see the result as good or bad for resolving the US’s fiscal cliff. The biggest risk is that we get an extended period of uncertainty about that, from both:

The actual results: Close races take longer to resolve due to recounts, mail-in ballot issues, etc. Weather related delays from Hurricane Sandy and additional storms may also be a factor.

Market Interpretation of the results: neither side earns a decisive victory, and major uncertainty remains about when and how Washington resolves the fiscal cliff.

The concern is very real, given that if all the planned spending cuts and tax increases go into effect, they could shrink GDP by up to 4 percent, according to Goldman Sachs analysts. See here for a detailed guide to the fiscal cliff and related perils.

Of course, no one expects Washington to allow the full range of tax cuts and spending increases to expire, given its decided preference for small short term gains, even at a cost of bigger problems in the long term that it risks from not making meaningful progress in reducing the US deficit. A compromise is expected, the only question is whether:

The final result is achieved in a timely manner that convinces markets that the US is not paralyzed by political deadlock (as suggested by the failure to resolve the debt ceiling mess in summer 2011 which convinced S&P to strip the US of its AAA rating) and can resolve its deficit issues while it still has time to avoid the kind of debt driven death spiral experienced in much of the Euro-zone.

Who pays the price: what goodies remain, which ones go, and whether that result is overall market friendly or not.

As we noted last week, a Republican victory is generally seen as more pro-markets, but in an era when markets rise or fall with the prospects of more stimulus, might they favor the more pro-stimulus/deficit spending Democrats this time?

The key point is that any kind of result that raises hopes for any kind of timely and responsible resolution of fiscal cliff will be good for risk assets. Continued uncertainty about the fiscal cliff would likely have the opposite effect, and favor safe havens like the USD and JPY in the near term.

However, the biggest effect of the US elections may simply come from the fact that once they’re done, so is Washington’s request for quiet in the EU. More on that below.

ONGOING HURRICANE SANDY EFFECTS

Market perceptions of Sandy’s effects are still evolving, and that could matter this week and beyond in a number of ways.

The thing to consider is that the US has no recent experience with a weather related disaster hitting such a densely populated, economically significant region.

The Election

The most immediate concern is if weather related problems effect Tuesday’s elections, both via delays or turnout. As noted above, in the near term, delays alone could keep markets cautious. In the longer term, if either side believes the election was unfairly ‘stolen’ by weather related issues, that resentment might complicate fiscal cliff negotiations.

Note that there’s a chance the US Northeast could get hit by more bad weather on Election Day. Given the current damage, new storms could compound the damage to infrastructure and property that hasn’t been repaired, and delay or prevent voters from voting.

Whether or not you believe that the hurricane was a direct result of climate change, New York Mayor Bloomberg thinks so, and apparently that caused him to publicly endorse Obama.

The Economy

Gluskin Sheff’s David Rosenberg wrote last week that markets have seriously underestimated the effects of Sandy on GDP. Essentially, he argues that we’ve no experience with a disaster that hits 60 million of America’s higher spending consumers. He writes:

We are talking about 60 million people being affected, not three, or four, or five million spread across corn and cotton fields in the south. There has not been such devastation affecting so many participants in the U.S. economy before. We’re talking about New York, New Jersey, Connecticut and Philadelphia here – not Waco. When such masses do not go to the office, then they don’t do what they usually do, which is buy their coffee at Starbucks. They don’t like up for pizza and sushi. That spending is not coming back.

….We are talking about the storm hitting the most free-spending consumers in America. And that is also because these are the states with the highest per capita incomes – the major states of the Northeast have on average household spending power that is 40% higher than in the deep south where storms and floods have historically been prevalent (again rendering comparisons with the past nearly totally useless when it comes to estimating near term GDP impact).

In addition, he notes that the hurricane hit this economically sensitive area just before the start of the most important time of the year for the retail sector, retailers are likely to get hit hard as these consumers divert spending to hurricane related damage.

That damage to consumer spending (70% of US GDP, most of which is spent during the holiday season) will radiate beyond the US to all those export economies that also depend on robust US consumer spending.

DELAYED REACTION TO US JOBS REPORT?

Of course, Asian markets don’t have the chance to respond to US monthly jobs reports, issued on the first Friday of each month, until the following Monday. The seemingly bullish reports failed to have any lasting effect on US markets, so we suspect Asia might not react strongly either.

Still, markets at times show a delayed reaction to these reports after having had a weekend to digest them and pick out important details that were drowned out by the headline numbers. For example, David Rosenberg pointed out that the drop in weekly wages undermines the bullish headline figures, because falling earnings shouldn’t be happening if the jobs market was materially improving.

If market opinion of Friday’s jobs reports sours, even just to the point where they’re seen as indicating no meaningful change rather than an improvement, that could weigh not only on the Obama campaign, but on markets as well.

EU

As noted above, arguably the most important effect of the US elections is that once they’re over, Washington’s request for quiet on the EU crisis is over, and public discussion on what to do about Greece and Spain can resume.

GREECE

Concerning Greece, that means deciding how to handle an eventual default and its timing.

There are some (like my esteemed colleague at forexcrunch.com) who dismiss my belief in the Reuters report on Washington’s request for EU quiet saying that

“the Greek crisis is mostly a European issue – two thirds of the troika are actually EU bodies.”

Child please! This is about contagion risk, not borders. Greece is no less an American issue than the US subprime mess and ultimate collapse of Lehman Brothers proved to be very much a European and global issue. Greece presents a contagion threat, a global contagion threat which Washington has repeatedly demonstrated that it recognizes all too well and obviously would do whatever it could to prevent in the weeks prior to the election. Global financial crises do not inspire confidence in the incumbent.

No doubt the EU remembers that its own debt and banking crisis was born in December 2009, not in the EU, but in remote Dubai, when its sovereign wealth fund announced it would defer bond payments. Focus then turned to other possible default risks. Within 6 months the EU went from denial of any major problems to a full Greek bailout, soon followed by bailouts for others.

Anyway, Greece says it will be out of cash in a few weeks. This week, Greece’s parliament must once again approve austerity measures it can’t keep in order to get another tranche of loans it can’t repay. So, we should anticipate it will generate some drama and market volatility in the coming weeks as markets anticipate whether it will or won’t default again and who gets stuck taking the losses.

Oh, and for those who will argue that the size of a Greek default is within EU means, remember that the primary danger from a Greek default isn’t the financial loss. Rather, the danger is the loss of confidence in GIIPS debt. That could send bond yields soaring for…..

SPAIN

Spanish bond yields have stabilized in the three months since the ECB announced its OMT program to buy sovereign bonds, because now all assume the ECB will prop up Spanish bonds when the need arises. That calm is the only thing keeping Spain’s bond yields from rising, and from Spain needing to ask for a bailout, which would make markets more nervous and perhaps even focus attention on (gulp) Italy.

Even if we somehow have continued quiet on Greece, there’s plenty of potential for trouble from Spain.

Its economy and banking system continue to deteriorate, and its list of regions and banks seeking bailouts keeps growing. That means the time for Spain’s needing a bailout (fast) is approaching, even though Spain insists it has enough cash for the rest of the year (i.e. nine weeks). Meanwhile coming Catalan elections (scheduled for November 25) may prevent Spain from accepting conditions demanded from its EU creditors in exchange for the assumed bailout.

Do you see how easily markets could start getting worried about Spain?

OTHER EU EVENTS

On Wednesday there are Euro-group meetings, which might be a venue for renewed public discussion on Greece and Spain, now that US elections are over and the EU’s unpleasant realities can again be publicly discussed.

On Thursday, there’s the ECB’s monthly rate statement and press conference, another potential venue for these topics. With the GIIPS in deep recession and even France and Germany struggling, the pressure is on for the ECB to do more. Both a rate cut and even some direct debt purchases via the old SMP program are possible. See here for details. Usually such potentially dilutive moves would hurt the EUR, but markets are more concerned about its survival than loss of purchasing power, so any downside might not be significant.

Remember, purchases via the OMT can’t happen until a nation requests them and accepts conditions designed to preserve the chance that the bonds might be repaid.

CHINA LEADERSHIP TRANSITION

A changing of the guard at China’s 18 Communist Party Congress is noteworthy though unlikely to have short term market influence unless it brings further corruption scandals to light in the wake of the leadership transition.

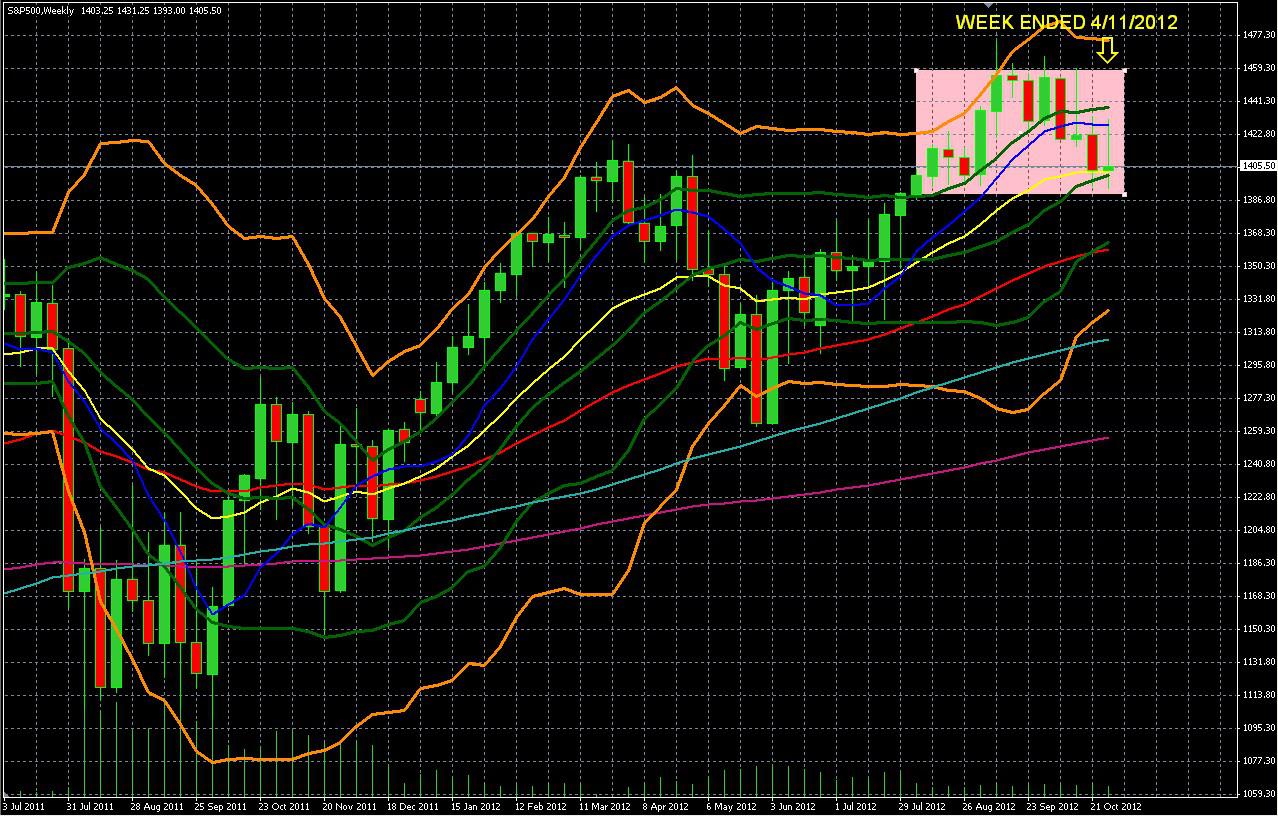

TECHNICAL PICTURE

Looking at the bellwether S&P 500 chart below, what do we see?

(click to enlarge)

WEEKLY S&P 500 CHART

Source: MetaQuotes Software Corp, thesensibleguidetoforex.com globalmarkets.anyoption.com, 04 NOV 04 02 58

The main messages from the Weekly S&P 500 are:

1. We remain within a 13 week trading range that’s near decade highs

2. Both of the long term up trends that were fueled by speculation of coming new QE programs (that began in the summers of 2011 and 2012) have lost their upward momentum. This loss of momentum is confirmed by:

-The index has completed its 4th straight week below its upper Double Bollinger band buy zone (bounded by the upper orange and green Bollinger bands). When price is within this upper zone, that’s our confirmation that even after a prolonged move higher, the momentum is still strong enough to trust for those seeking to open new long positions. To quickly understand how to use and interpret double Bollinger bands, see: 4 Rules For Using The Most Useful Technical Indicator, Double Bollinger Bands.

-The 10 (blue) and 20 (yellow) week EMAs flattening out

-The weekly candles for the past 4 weeks show a repeating pattern of downward movement (red -lower close-bodies) followed by weak, minimal attempts to move higher shown by the “gravestone” dojis candles. The long upper wicks and minimal higher closes of these gravestone dojis suggest a market trying to push higher, failing, and then giving up most of its gains.

In view of the bearish fundamental picture detailed above (and summarized below), the technical picture can be viewed as either:

Positive: A market showing remarkable resilience in the face of discouraging fundamentals.

Negative: A market that is bending under the weight of those fundamentals, has not yet broken, but is in the process of doing so.

Which is it?

CONCLUSIONS

After rallying since June on hopes for a Spain rescue and more Fed stimulus, most risk asset markets remain near decade highs. What do they have going for them to fuel them higher?

-More stimulus? It’s already unlimited. The only question is when it will stop, so we’re not likely to see a lot of upside from that

-Financial repression: anyone needing income will find it hard to get enough yield from investment quality bonds, and so is pushed into stocks despite the risks of these bearish fundamentals.

-Less uncertainty when the US elections and fiscal cliff are resolved: At best these are likely to bring minor relief because the results aren’t as bad as feared. They aren’t likely to generate enough excitement to justify a decisive break above 2007 highs.

In sum, we’ve a bearish fundamental picture characterized by:

-Slowing global growth that’s starting to show up in earnings that are steadily being revised lower

-A simmering EU crisis that threatens to boil over yet again

-A looming US fiscal cliff that once resolved will likely reduce US GDP by 1-4%

Indeed, the rally in risk assets since the summer of 2011 has been fueled primarily by anticipated stimulus and low rates rather than actual signs of growth. To move higher, it needs new bullish fundamentals but can’t look forward to much more government intervention than what it already has gotten.

Combine these fundamental threats with an overall technical picture of a market that has stalled, and we conclude that the odds favor more pullback. Whether it’s a minor or major one depends whether the EU or fiscal cliff issues turn ugly. We suspect at least one of them will do so.

We reiterate our weekly warning that all of the most likely scenarios we see coming involve a vast expansion of the supply of dollars, euros, yen, and also of other currencies as nations seek to protect their exports’ competitiveness with cheaper currency.

We reiterate our weekly warning that all of the most likely scenarios we see coming involve a vast expansion of the supply of dollars, euros, yen, and also of other currencies as nations seek to protect their exports’ competitiveness with cheaper currency.

That means we all need to start diversifying into the more responsibly managed currencies or into assets denominated in them. For details on the best collection of the safer, simpler, less demanding ways to do this than generally found in guides to forex markets or to investing in foreign assets, just click “The Sensible Guide To Forex“.

Related Articles

About the Author

Cliff Wachtel, CPA, is currently the Chief Analyst of anyoption.com, a leading binary options broker, and Director of Market Research, New Media and Training for Caesartrade.com, a fast growing forex and CFD broker.

Cliff Wachtel, CPA, is currently the Chief Analyst of anyoption.com, a leading binary options broker, and Director of Market Research, New Media and Training for Caesartrade.com, a fast growing forex and CFD broker.

He is also the author of The Sensible Guide To Forex, and publisher of thesensibleguidetoforex.com. Both the book and website are uniquely dedicated to providing safer, simpler ways for active traders and passive long term income investors to use forex markets to diversify out of currencies like the USD, EUR, JPY, and others that are being debased by excessive money printing. Since the Great Financial Crisis began in 2007, Cliff was among the first financial writers to focus on stocks that provide steady, high yields currency diversification for insurance against currencies being steadily devalued. Articles focus on both top income stocks for exposure to multiple quality currencies, and safer, simpler less demanding types of longer term forex trades than commonly covered on other forex sites.

Cliff can also be found at leading financial websites such as Seeking Alpha, Business Insider and forex sites like Forex Factory. He has appeared in a variety of offline publications including Forex Journal, and John Nyaradi’s book, Super Sectors, in which he was interviewed along with other market experts like Jim Rodgers, Dr.Marc Faber, John Mauldin, Robert Prechter, and Tom Lydon.