by Carla Fried, Editor, Y-Charts

Spitting out 4% dividend payouts makes utility stocks undeniable catnip for yield-prowling investors. But that’s some expensive catnip. Historically, the utility sector trades at a lower price/earnings multiple than the rest of the market given its defensive slow-growth profile. Right now, though, it’s trading at a near 20% premium.

Spitting out 4% dividend payouts makes utility stocks undeniable catnip for yield-prowling investors. But that’s some expensive catnip. Historically, the utility sector trades at a lower price/earnings multiple than the rest of the market given its defensive slow-growth profile. Right now, though, it’s trading at a near 20% premium.

If you happen to care about valuation, the healthcare sector is well worth some vetting. According to FactSet, the health care stocks in the S&P 500 currently trade at a forward p/e that is in line with the overall index. And that’s for a segment of the economy with far better growth prospects.

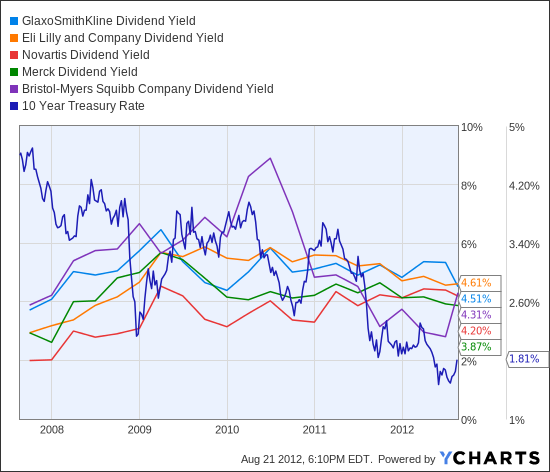

Moreover, big pharma stocks — including GlaxoSmithKline (GSK) — also happen to be spinning out utility-level yields that offer plenty more income than the 10-year Treasury note.

GSK Dividend Yield data by YCharts

Now of course there’s got to be a reason those stocks are paying yields that far outpace the 2% payout for the overall S&P 500. On the macro level, there was some collective sidelining going on as everyone waited for the Supreme Court to decide the fate of the Affordable Care Act (ACA). And on the company-level there’s been apprehension over how firms would compensate for the loss of lucrative exclusive patents on blockbuster drugs. In just the past year Pfizer (PFE) has bid adios to its exclusive on Lipitor, Eli Lilly (LLY) has seen its blockbuster Zyprexa antipsychotic drug open to the generic market, and Bristol-Myers Squibb (BMY) is dealing with life after its Plavix exclusivity ran out.

The ACA uncertainty is over, but there’s still plenty of wait-and-see to deal with regarding the development (and FDA approval) of next-generation drugs. For example, Pfizer recently reported that the FDA needs more time to review a new rheumatoid arthritis treatment the drug firm-and the Street-has high hopes for.

But if you’ve got a long-term outlook, big pharma’s big yields are paying you a lot to be patient, without sticking you with abnormally high valuations (see: utilities.) Bristol-Myer Squibb’s 4.3% yield comes with a PE ratio that is still trading below its 10-year low.

BMY PE Ratio data by YCharts

Same sort of situation with the 4.6% dividend yield on Eli Lilly shares.

LLY PE Ratio data by YCharts

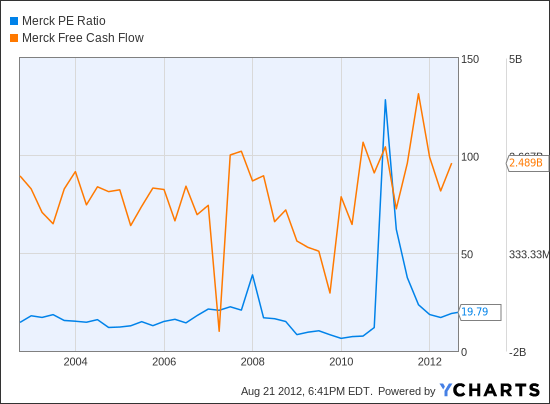

Merck’s (MRK) near 20 PE ratio doesn’t scream bargain relative to the broad market, but it’s right in line with its long-term average.

MRK PE Ratio data by YCharts

Then there’s Johnson & Johnson (JNJ) It’s had enough headaches the past few years that even Warren Buffett has seemingly lost patience, recently selling off a large chunk of Berkshire Hathaway’s long-time stake. It’s not a screaming bargain relative to the market either, but it offers the allure of one of the best dividend growth histories in the sector.

JNJ Dividend data by YCharts

And despite its lousy performance the past few years, Johnson & Johnson isn’t having to dig deep into its cash to make the dividend payouts; its 43% cash dividend payout ratio is in line with other U.S. based big pharma.

JNJ Cash Div. Payout Ratio TTM data by YCharts

For income-seeking investors there is clearly some utility in checking out the health care sector. High current dividend yields and the cash to keep the payments coming is often available at a below-market valuation.

About the Author: Carla Fried is an editor for the YCharts Pro Investor Service which includes professional stock charts, stock ratings and portfolio strategies.

Ratings notes:

Bristol-Myers Squibb Company is rated Neutral.

GlaxoSmithKline is rated Neutral.

Johnson & Johnson is rated Neutral.

Eli Lilly and Company is rated Neutral.

Merck & Co Inc. is rated Neutral.

Pfizer Inc. is rated Neutral.

Find out why with YCharts Pro: Click here to start your 14-day trial.

Related Articles